Global Arthroscopy Devices Market

Market Size in USD Billion

CAGR :

%

USD

7.26 Billion

USD

14.80 Billion

2024

2032

USD

7.26 Billion

USD

14.80 Billion

2024

2032

| 2025 –2032 | |

| USD 7.26 Billion | |

| USD 14.80 Billion | |

| % | |

|

Arthroscopy Devices Market Size

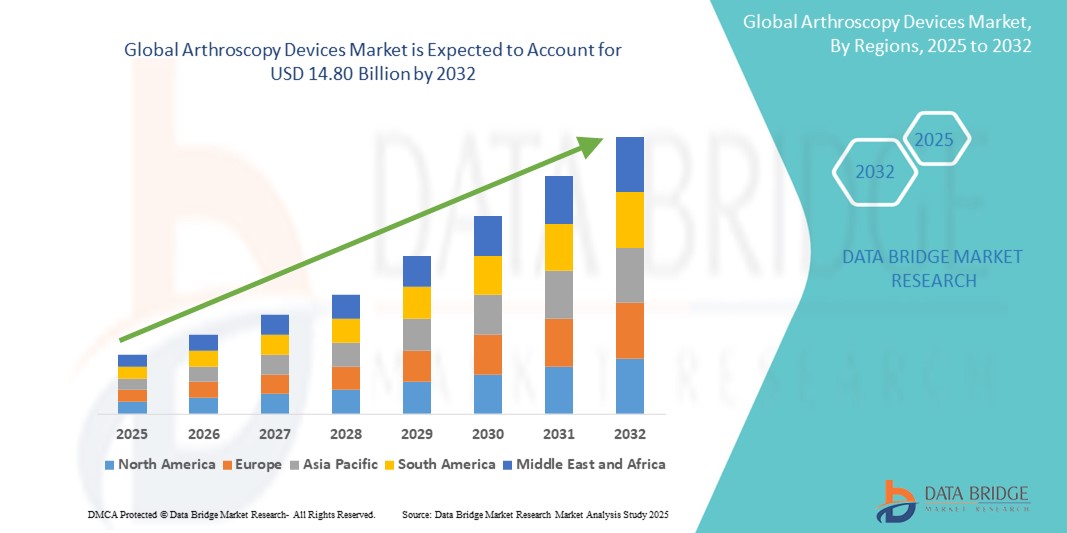

- The global arthroscopy devices market size was valued at USD 7.26 billion in 2024 and is expected to reach USD 14.80 billion by 2032, at a CAGR of 9.30% during the forecast period

- This growth is driven by factors such as the increasing prevalence of joint-related disorders, rising demand for minimally invasive surgical procedures, and advancements in arthroscopic technologies

Arthroscopy Devices Market Analysis

- Arthroscopy devices are minimally invasive surgical instruments used to diagnose and treat joint conditions, particularly in the knee, shoulder, hip, and wrist, offering quicker recovery and reduced surgical risks

- The demand for arthroscopy devices is driven by the rising incidence of sports injuries, osteoarthritis, and technological advancements in imaging and surgical tools

- North America is expected to dominate the arthroscopy devices market with a market share of 46.4%, due to advanced healthcare infrastructure, high adoption of minimally invasive surgical procedures, and a strong presence of leading market players

- Asia-Pacific is expected to be the fastest growing region in the arthroscopy devices market with a market share of 25.5%, during the forecast period due to rapid improvements in healthcare infrastructure, increasing awareness about joint health, and rising surgical volumes

- Arthroscopic implants segment is expected to dominate the market with a market share of 48.1% due to its the high demand for joint stabilization and repair during arthroscopic procedures. These implants, such as screws, anchors, and grafts, are essential for treating ligament injuries, cartilage damage, and joint instabilities, which are common in knee, shoulder, and other joint surgeries

Report Scope and Arthroscopy Devices Market Segmentation

|

Attributes |

Arthroscopy Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Arthroscopy Devices Market Trends

“Technological Advancements in Arthroscopic Visualization and Instrumentation”

- One prominent trend in the arthroscopy devices market is the rapid development of high-definition camera systems and minimally invasive surgical instruments, significantly enhancing the accuracy and efficiency of joint surgeries

- These innovations are improving clinical outcomes by enabling clearer intra-articular visualization, better access to joint spaces, and more precise tissue manipulation during procedures

- For instance, 4K and 3D visualization systems are now being integrated into arthroscopic towers, allowing surgeons enhanced depth perception and image clarity, which is particularly beneficial for complex procedures such as shoulder and hip arthroscopy

- These advancements are reshaping arthroscopic surgeries, reducing patient recovery times, and fueling the demand for next-generation arthroscopy devices across both developed and emerging healthcare markets

Arthroscopy Devices Market Dynamics

Driver

“Increasing Prevalence of Joint Disorders and Sports Injuries”

- The rising prevalence of joint disorders such as osteoarthritis, along with the growing number of sports-related injuries, is significantly driving the demand for arthroscopy devices

- With the global population aging and increased participation in sports, conditions such as knee injuries, shoulder instability, and ligament tears are becoming more common, necessitating minimally invasive surgical interventions

- As more patients seek treatment for these conditions, the demand for advanced arthroscopic devices, including visualization systems and powered shaver systems, continues to rise, leading to enhanced surgical outcomes and faster recovery times

For instance,

- According to a 2022 report by the World Health Organization, osteoarthritis affects over 10% of the global population aged 60 and above, which increases the need for joint-related surgeries

- The growing incidence of these conditions, coupled with the benefits of minimally invasive procedures, is driving the demand for next-generation arthroscopic tools and technologies

Opportunity

“Integration of Artificial Intelligence in Arthroscopic Surgery”

- AI-powered arthroscopy devices are transforming joint surgeries by enhancing visualization, automating complex tasks, and improving diagnostic accuracy, which enables surgeons to make more precise decisions during procedures

- AI algorithms can analyze real-time joint images and offer feedback on surgical steps, helping surgeons identify potential issues such as ligament tears, joint instability, or cartilage damage, improving the overall outcome of the procedure

- In addition, AI-driven systems can assist in pre-surgical planning, postoperative monitoring, and rehabilitation, offering personalized treatment plans and enabling early detection of complications

For instance,

- In 2024, a study published in The Journal of Arthroplasty found that AI applications, particularly machine learning, could accurately predict post-surgical outcomes for knee and hip replacement surgeries, improving preoperative decision-making and reducing the rate of complications

- The integration of AI in arthroscopic devices is expected to drive more efficient surgeries, reduce recovery times, and enhance the overall surgical experience, leading to a rise in demand for these advanced technologies in the market

Restraint/Challenge

“High Equipment Costs Hindering Market Penetration”

- The high cost of arthroscopic devices remains a significant challenge for the market, particularly for healthcare facilities in developing regions where budget constraints are more pronounced

- Advanced arthroscopic equipment, including high-definition cameras, specialized shavers, and fluid management systems, can cost tens of thousands to even hundreds of thousands of dollars, making them unaffordable for smaller clinics and hospitals

- This financial burden can prevent healthcare providers from investing in the latest arthroscopic technologies, leading to reliance on older, less efficient equipment that may hinder the precision and outcomes of joint surgeries

For instance,

- According to a 2024 report by The Journal of Orthopedic Surgery & Research, the high cost of arthroscopic tools, combined with maintenance expenses, has led to equipment underutilization in smaller healthcare centers, limiting their ability to offer state-of-the-art services

- Consequently, such challenges create a gap in the accessibility of advanced arthroscopy devices, affecting market expansion, particularly in low- and middle-income countries, where healthcare affordability is a key concern.

Arthroscopy Devices Market Scope

The market is segmented on the basis of product, application, and end user.

|

Segmentation |

Sub-Segmentation |

|

By Product |

|

|

By Application |

|

|

By End User |

|

In 2025, arthroscopic implants is projected to dominate the market with a largest share in product segment

The arthroscopic implants segment is expected to dominate the arthroscopy devices market with the largest share of 48.1% in 2025 due to the high demand for joint stabilization and repair during arthroscopic procedures. These implants, such as screws, anchors, and grafts, are essential for treating ligament injuries, cartilage damage, and joint instabilities, which are common in knee, shoulder, and other joint surgeries. Their widespread use, coupled with ongoing advancements in implant materials and design, drives the growth of this segment

The knee arthroscopy is expected to account for the largest share during the forecast period in application market

In 2025, the knee arthroscopy segment is expected to dominate the market with the largest market share of 42.3% due to its the high prevalence of knee injuries, particularly among athletes and the aging population. Knee arthroscopy is a minimally invasive procedure used to treat various conditions such as ligament tears, meniscal damage, and osteoarthritis. The growing number of sports-related knee injuries, combined with the benefits of faster recovery and reduced surgical risks, drives the continued demand for knee arthroscopy procedures

Arthroscopy Devices Market Regional Analysis

“North America Holds the Largest Share in the Arthroscopy Devices Market”

- North America dominates the arthroscopy devices market with a market share of estimated 46.4%, driven by advanced healthcare infrastructure, high adoption of minimally invasive surgical procedures, and a strong presence of leading market players

- U.S. holds a market share of 35.5%, due to the increasing demand for arthroscopic surgeries, the rising prevalence of joint disorders such as osteoarthritis and sports injuries, and continuous advancements in arthroscopic technologies

- The availability of well-established reimbursement policies, along with significant investments in research and development by major medical device companies, further strengthens the market in the region

- In addition, the growing number of joint-related surgeries and an increasing focus on patient outcomes through advanced surgical techniques fuel the market growth across North America

“Asia-Pacific is Projected to Register the Highest CAGR in the Arthroscopy Devices Market”

- Asia-Pacific is expected to witness the highest growth rate in the arthroscopy devices market with a market share of 25.5%, driven by rapid improvements in healthcare infrastructure, increasing awareness about joint health, and rising surgical volumes

- Countries such as China, India, and Japan are emerging as key markets due to the growing aging population and the increasing prevalence of joint disorders, which create a higher demand for arthroscopic procedures

- Japan, with its advanced healthcare system and a high number of orthopedic surgeons, remains a critical market for arthroscopic devices, continuously adopting the latest surgical equipment to enhance precision and efficiency

- India is projected to register the highest CAGR of 5.4%, driven by expanding healthcare facilities, a rising prevalence of joint diseases, and the growing adoption of minimally invasive surgical technologies

Arthroscopy Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Arthrex, Inc. (U.S.)

- Smith+Nephew (U.K.)

- Johnson & Johnson Services, Inc. (U.S.)

- Stryker (U.S.)

- CONMED Corporation (U.S.)

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- B. Braun SE (Germany)

- Zimmer Biomet (U.S.)

- KARL STORZ SE & Co. KG (Germany)

- Olympus Corporation (Japan)

- Richard Wolf GmbH (Germany)

- Bioventus (U.S.)

- Medicon Health Care Private Limited (India)

- Sklar Instruments (U.S.)

- GPC Medical Ltd (India)

- Zimmer MedizinSysteme GmbH (Germany)

- Joimax GmbH (Germany)

Latest Developments in Global Arthroscopy Devices Market

- In March 2025, Smith+Nephew, a global medical technology company, announced the launch of its next-generation Werewolf Fastseal 6.0 Hemostasis Wand, designed for use in arthroscopic procedures. The new device enhances soft tissue management and bleeding control during surgery, improving visibility and efficiency for surgeons, particularly in shoulder and knee arthroscopy

- In January 2025, Arthrex, Inc. introduced the NanoNeedle Scope System, a miniaturized arthroscopy platform that allows for minimally invasive joint assessments and treatments using only a needle-sized incision. This innovation supports in-office diagnostic procedures, reducing the need for full operating room interventions and enhancing patient comfort

- In November 2024, Stryker Corporation showcased its advanced 1688 AIM 4K Platform with SPY fluorescence imaging at the American Academy of Orthopaedic Surgeons (AAOS) conference. The system improves intraoperative visualization and enables real-time tissue perfusion assessment, offering enhanced clarity and precision in joint surgeries

- In September 2024, CONMED Corporation launched the Argo Knotless Suture Anchor System, offering surgeons a reliable and efficient solution for soft tissue fixation. The system improves surgical workflow, reduces operative time, and enhances outcomes in shoulder and knee repair procedures. It was well received at the 2024 Orthopaedic Summit (OSET), further solidifying CONMED’s leadership in arthroscopic repair innovation

- In December 2021, Healthium Medtech had launched Arthroscopy product manufacturing facilities in Ahemdabad. The Arthroscopy products developed in the manufacturing facility are used to treat various knee and shoulder conditions, including anterior cruciate ligament reconstruction, posterior cruciate ligament injuries, and others.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.