Europe Igg4 Related Disease Market

Market Size in USD Million

CAGR :

%

USD

855.72 Million

USD

1,144.35 Million

2025

2033

USD

855.72 Million

USD

1,144.35 Million

2025

2033

| 2026 –2033 | |

| USD 855.72 Million | |

| USD 1,144.35 Million | |

| % | |

|

Europe IgG4-Related Disease Market Size

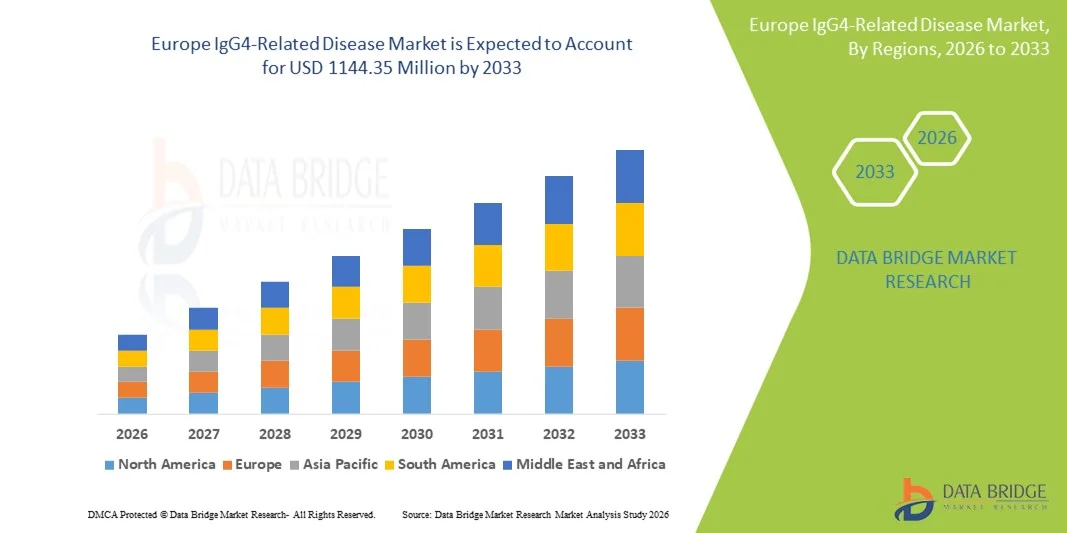

- The Europe IgG4-Related Disease market size was valued at USD 855.72 Million in 2025 and is expected to reach USD 1144.35Million by 2033, at a CAGR of 3.70% during the forecast period

- The market growth is largely fueled by the increasing prevalence and improved diagnosis of autoimmune and inflammatory disorders, along with rising awareness among healthcare professionals regarding IgG4-related disease (IgG4-RD), leading to higher detection rates and expanding treatment adoption across hospitals and specialty clinics

- Furthermore, growing research activities focused on immunosuppressive therapies, biologics, and targeted treatment approaches are improving clinical outcomes and strengthening therapeutic pipelines. These converging factors are accelerating the uptake of IgG4-related disease treatment solutions, thereby significantly boosting the industry's growth

Europe IgG4-Related Disease Market Analysis

- IgG4-related disease, a chronic immune-mediated fibro-inflammatory condition affecting multiple organs, is gaining increasing clinical attention due to improved diagnostic criteria, growing physician awareness, and expanding availability of advanced imaging and histopathological testing across tertiary healthcare settings

- The rising demand for IgG4-related disease treatment is primarily driven by increasing prevalence of autoimmune disorders, growing adoption of corticosteroids and immunosuppressive therapies, and ongoing research into targeted biologics aimed at reducing relapse rates and long-term organ damage

- The U.K. dominated the IgG4-related disease market with the largest revenue share of approximately 34.7% in 2025, supported by strong government investment in healthcare infrastructure, expansion of specialty and tertiary hospitals, improved access to advanced diagnostic services, and increasing focus on rare and immune-mediated disease management under national healthcare initiatives

- Germany is expected to be the fastest-growing country in the IgG4-related disease market during the forecast period, driven by rapid growth in private healthcare facilities, rising medical tourism, increasing adoption of advanced immunology diagnostics, and growing availability of specialized treatments for rare autoimmune conditions

- The Parenteral segment dominated, holding the largest revenue share of 62.1% in 2025, due to the widespread use of intravenous corticosteroids, immunoglobulins, and biologic therapies in treating severe or multi-organ IgG4-RD

Report Scope and IgG4-Related Disease Market Segmentation

|

Attributes |

IgG4-Related Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe IgG4-Related Disease Market Trends

Enhanced Focus on Early Diagnosis and Targeted Treatment

- There is a growing emphasis on early detection and precise management of IgG4-Related Disease, as delayed diagnosis can lead to permanent organ damage in affected patients. Early recognition is critical for preventing complications in organs such as the pancreas, kidneys, salivary glands, and lungs

- For instance, In 2024, a tertiary care hospital in Japan implemented a combined imaging and serological screening program, which resulted in a 35% increase in early-stage detection of IgG4-Related Disease, enabling timely treatment initiation and improved patient outcomes

- Advanced diagnostic techniques—including high-resolution imaging, serum IgG4 testing, and tissue biopsies—are increasingly being adopted worldwide, particularly in specialized healthcare center

- The market is also witnessing a shift toward targeted therapies, such as corticosteroid-sparing immunosuppressants and monoclonal antibodies like rituximab, which allow precise disease control while minimizing long-term steroid exposure

- Multidisciplinary approaches, involving rheumatologists, gastroenterologists, nephrologists, and pathologists, are becoming more common, ensuring comprehensive patient management and reducing relapse risks

Europe IgG4-Related Disease Market Dynamics

Driver

Rising Prevalence and Growing Awareness

- The market is being driven by the increasing prevalence of IgG4-Related Disease globally, coupled with heightened awareness among healthcare professionals and patients about its manifestations and complications

- For Instance, In 2023, the Mayo Clinic in the U.S. launched a physician awareness campaign for IgG4-Related Disease, which led to a 28% increase in referrals to specialized treatment centers, demonstrating the direct impact of education and awareness on diagnosis and market growth

- Investment in healthcare infrastructure, including specialized immunology clinics, advanced imaging, and pathology laboratories, is improving access to proper diagnosis and ongoing monitoring

- Growing prevalence of autoimmune and inflammatory disorders, along with an aging global population, is increasing the need for effective management strategies

- Continuous clinician training programs and professional workshops are helping to reduce misdiagnosis, shorten the time to treatment, and promote standardized therapeutic approaches

Restraint/Challenge

High Treatment Costs and Limited Access

- High costs of advanced therapies and biologic treatments remain a key restraint for the market, limiting access to effective management options in both developing and some developed countries

- For Instance A 2022 study in India revealed that less than 40% of patients diagnosed with IgG4-Related Disease could access biologic therapy due to high costs and limited availability of specialized treatment centers

- Long-term therapy is often required because of the relapsing nature of the disease, adding to the financial and logistical burden on patients

- Limited clinician expertise in certain regions contributes to delayed diagnosis and suboptimal treatment outcomes, further restraining market growth

- Complex therapy regimens and side effects of immunosuppressive drugs can affect patient adherence, while travel to specialized centers may be challenging for patients in rural or semi-urban areas

- Efforts to reduce cost, expand insurance coverage, and increase the availability of advanced therapies will be critical for sustained growth in emerging markets

Europe IgG4-Related Disease Market Scope

The market is segmented on the basis of disease type, type, route of administration, end-user, and distribution channel.

- By Disease Type

On the basis of disease type, the IgG4-Related Disease market is segmented into Type 1 (IgG4-Related) Autoimmune Pancreatitis (AIP), Retroperitoneal Fibrosis, IgG4-Related Tubulointerstitial Nephritis (TIN), IgG4-Related Sclerosing Cholangitis, IgG4-Related Dacryoadenitis and Sialadenitis, IgG4-Related Pachymeningitis, IgG4-Related Thyroid Disease, Serum IgG4 Concentration, and Others. The Type 1 Autoimmune Pancreatitis (AIP) segment dominated the market, accounting for the largest revenue share of approximately 39.5% in 2025, due to its high prevalence among IgG4-RD patients and well-established clinical recognition. The segment benefits from widespread physician awareness, routine diagnostic screening, and established treatment protocols. AIP cases often require advanced imaging, serological testing, and corticosteroid therapy, which drive procedure volume and treatment adoption. Hospitals and specialty clinics frequently manage these patients, further supporting revenue dominance. Early diagnosis and increasing disease awareness contribute to sustained growth. Clinical guidelines and evidence-based therapies increase confidence in management. The segment’s robust presence in North America, Europe, and parts of Asia enhances market share. Ongoing research in biomarkers and imaging methods maintains its leading position.

The IgG4-Related Tubulointerstitial Nephritis (TIN) segment is projected to witness the fastest CAGR of 9.2% from 2026 to 2033, driven by rising awareness of renal involvement in IgG4-RD and increasing diagnostic advancements. The segment benefits from improved serological testing, biopsy techniques, and growing recognition of renal manifestations in systemic disease. Adoption is being accelerated by expanding nephrology centers and increased referral patterns from general practitioners. Early detection and effective treatment improve patient outcomes, further motivating adoption. Technological advancements in imaging and laboratory testing enhance diagnosis. Emerging markets with growing healthcare infrastructure are increasingly diagnosing and managing TIN cases. Training programs for nephrologists and immunologists are also contributing. Collectively, these factors make TIN the fastest-growing disease type segment.

- By Type

On the basis of type, the market is segmented into Diagnostic and Treatment. The Treatment segment dominated the market, holding a revenue share of around 58.3% in 2025, due to the high reliance on corticosteroids, immunosuppressive agents, and biologic therapies for disease management. Hospitals and specialty clinics widely adopt treatment regimens, particularly in severe or multi-organ involvement cases. Established clinical guidelines recommend prompt therapy to prevent organ damage, supporting consistent revenue generation. The segment benefits from ongoing innovations in biologics and targeted therapies. Adoption in developed regions with high healthcare expenditure, particularly North America and Europe, reinforces dominance. Strong physician familiarity and robust reimbursement frameworks support continued growth. Growing prevalence of multi-organ IgG4-RD cases contributes to sustained demand. Treatment effectiveness and patient outcome improvements further maintain segment leadership.

The Diagnostic segment is expected to witness the fastest CAGR of 8.6% from 2026 to 2033, driven by the increasing use of serum IgG4 testing, imaging modalities, and biopsy-based diagnosis. Rising awareness among clinicians and improved availability of advanced diagnostic tools are accelerating uptake. Early diagnosis enables timely treatment, reducing complications and hospitalization costs. Expansion of specialty clinics and tertiary care centers also boosts adoption. Technological improvements, including more sensitive assays, further enhance growth. Emerging markets investing in diagnostic infrastructure are likely to witness rapid growth. Government initiatives promoting early disease detection support adoption. Collectively, these factors position diagnostics as the fastest-growing type segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into Parenteral, Oral, and Others. The Parenteral segment dominated, holding the largest revenue share of 62.1% in 2025, due to the widespread use of intravenous corticosteroids, immunoglobulins, and biologic therapies in treating severe or multi-organ IgG4-RD. Hospitals and specialty clinics favor parenteral administration for rapid efficacy and controlled dosing. Established treatment guidelines recommend IV therapy for acute exacerbations, supporting revenue generation. Physician familiarity, predictable pharmacokinetics, and reliable patient response maintain dominance. Adoption is strongest in North America and Europe, where hospital infrastructure supports infusion therapy. Parenteral administration is preferred in cases requiring immediate intervention, multi-organ involvement, or refractory disease. Accessibility, safety monitoring, and standardized protocols reinforce market leadership. Strong pipeline of advanced IV therapies supports ongoing growth.

The Oral segment is projected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by convenience, patient compliance, and long-term management needs. Oral corticosteroids and immunosuppressive drugs are increasingly used for maintenance therapy. Growth is supported by rising outpatient care adoption and increasing disease awareness. Advances in oral formulations enhancing bioavailability and reducing side effects contribute to adoption. Expansion of specialty clinics and telemedicine follow-ups further accelerate growth. Emerging markets are witnessing faster oral therapy uptake due to cost-effectiveness and accessibility. Combined, these factors make oral administration the fastest-growing segment.

- By End-User

On the basis of end-user, the market is segmented into Hospitals, Specialty Clinics, and Others. The Hospitals segment dominated, accounting for a revenue share of approximately 54.7% in 2025, due to high patient volumes, availability of multidisciplinary care, and specialized units for autoimmune and systemic disorders. Hospitals manage complex multi-organ IgG4-RD cases requiring advanced diagnostics and treatment. Well-equipped facilities, access to specialists, and reimbursement support reinforce dominance. Hospitals also facilitate clinical trials, research initiatives, and advanced therapy adoption. North America and Europe remain the largest markets due to strong healthcare infrastructure and awareness. Hospitals act as referral centers, further enhancing procedure volume. Rising investments in specialized care units sustain segment leadership.

The Specialty Clinics segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by increasing awareness of IgG4-RD among immunologists, gastroenterologists, and nephrologists. Specialty clinics are expanding advanced diagnostic and treatment offerings. Rising patient preference for focused care, outpatient management, and personalized treatment supports adoption. Increasing investments in clinical infrastructure, coupled with rising private healthcare penetration in emerging markets, further accelerate growth. Specialty clinics’ focus on early detection and disease monitoring contributes to faster adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment dominated, holding the largest revenue share of 56.2% in 2025, as hospitals dispense corticosteroids, biologics, and immunosuppressive agents directly to patients undergoing treatment. Strong hospital procurement frameworks, reliable supply chains, and established relationships with pharmaceutical manufacturers contribute to dominance. Hospital pharmacies support specialized dosing, IV administration, and inpatient care. Adoption is strongest in North America and Europe due to healthcare infrastructure and reimbursement systems. Availability of advanced biologics and combination therapy protocols reinforces leadership.

The Online Pharmacy segment is expected to witness the fastest CAGR of 10.1% from 2026 to 2033, driven by increasing e-commerce penetration, patient preference for home delivery, and the growing trend of telemedicine consultations. Online pharmacies facilitate convenient access to oral medications and maintenance therapy for chronic IgG4-RD patients. Expansion of digital healthcare platforms, improved logistics, and patient awareness further support adoption. Cost-effectiveness, accessibility in remote regions, and home delivery services contribute to growth. Emerging markets with rising internet penetration are expected to adopt online pharmacy channels rapidly.

Europe IgG4-Related Disease Market Regional Analysis

- The Europe IgG4-related disease market is growing steadily, driven by rising healthcare expenditure, increased awareness of rare autoimmune diseases, and expansion of advanced healthcare infrastructure across the region

- Hospitals and specialty clinics are increasingly adopting state-of-the-art diagnostics, biologics, and immunosuppressive therapies to enable accurate disease detection and effective management. Government initiatives, public-private partnerships, medical research investments, and growing medical tourism further support market growth

- The adoption of advanced immunology labs, multidisciplinary treatment centers, and improved reimbursement coverage enhances patient access to innovative therapies, fueling demand

U.K. IgG4-Related Disease Market Insight

The U.K. IgG4-related disease market dominated the Europe market, holding the largest revenue share of approximately 34.7% in 2025. Market leadership is supported by strong government investment in healthcare infrastructure, expansion of specialty and tertiary hospitals, improved access to advanced diagnostic services, and increasing focus on rare and immune-mediated disease management under national healthcare initiatives. Hospitals and specialty clinics are adopting advanced immunology labs, biologics, and targeted therapies to manage complex IgG4-RD cases. Rising patient awareness, high-quality healthcare professionals, and investments in multidisciplinary care teams reinforce the U.K.’s dominant position.

Germany IgG4-Related Disease Market Insight

The Germany IgG4-related disease market is expected to be the fastest-growing country in the Europe market during the forecast period, driven by rapid expansion of private healthcare facilities, rising medical tourism, adoption of advanced immunology diagnostics, and growing availability of specialized treatments for rare autoimmune conditions. Private hospitals and specialty clinics are investing in cutting-edge diagnostic tools, biologics, and immunosuppressive therapies, enabling early detection and effective disease management. Government initiatives to modernize healthcare and increasing patient awareness accelerate market adoption, while robust infrastructure and high-income population segments support rapid uptake of new therapies.

Europe IgG4-Related Disease Market Share

The IgG4-Related Disease industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical Company (Japan)

- GSK. (U.K.)

- Roche (Switzerland)

- Pfizer (U.S.)

- Bristol-Myers Squibb (U.S.)

- Sanofi (France)

- AstraZeneca (U.K.)

- Eli Lilly and Company (U.S.)

- Novartis (Switzerland)

- Johnson & Johnson (U.S.)

- AbbVie (U.S.)

- Boehringer Ingelheim (Germany)

- Celgene (BMS subsidiary) (U.S.)

- Amgen (U.S.)

- Regeneron Pharmaceuticals (U.S.)

- Mallinckrodt Pharmaceuticals (Ireland/U.S.)

- Horizon Therapeutics (U.S.)

- Sobi (Sweden)

- Mitsubishi Tanabe Pharma (Japan)

- Ipsen (France)

Latest Developments in Europe IgG4-Related Disease Market

- In June 2024, Amgen announced positive topline results from its Phase 3 MITIGATE trial evaluating UPLIZNA (inebilizumab‑cdon) for the treatment of Immunoglobulin G4‑related disease (IgG4‑RD), showing an 87 % reduction in disease flares versus placebo and meeting all primary and key secondary endpoints — a significant clinical milestone toward establishing the first targeted therapy for the condition

- In February 2025, the U.S. Food and Drug Administration accepted Amgen’s regulatory submission for UPLIZNA (inebilizumab‑cdon) under priority review for IgG4‑related disease, advancing toward a potentially historic approval for a disease with limited treatment options beyond steroids

- In April 2025, the U.S. FDA approved UPLIZNA (inebilizumab‑cdon) as the first and only FDA‑approved treatment specifically for adults living with Immunoglobulin G4‑related disease (IgG4‑RD), recognizing it with Breakthrough Therapy Designation and offering a steroid‑sparing, flare‑reducing therapeutic option that directly targets underlying disease mechanisms

- In August 2025, the European Medicines Agency granted orphan designation to Sanofi’s investigational BTK inhibitor rilzabrutinib for the treatment of IgG4‑related disease, acknowledging the rare nature of the condition and supporting accelerated development pathways for novel therapeutic approaches

- In March 2025, Hansoh Pharmaceutical announced that the second Biologics License Application (BLA) of XINYUE (inebilizumab) was accepted by China’s National Medical Products Administration (NMPA) for IgG4‑related disease, indicating active regulatory progress toward approval in China and expanded global access

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.