Europe Electric Enclosure Market

Market Size in USD Billion

USD

2.50 Billion

USD

4.41 Billion

2025

2033

USD

2.50 Billion

USD

4.41 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.50 Billion | |

| USD 4.41 Billion | |

| % | |

|

What is the Europe Electric Enclosure Market Size and Growth Rate?

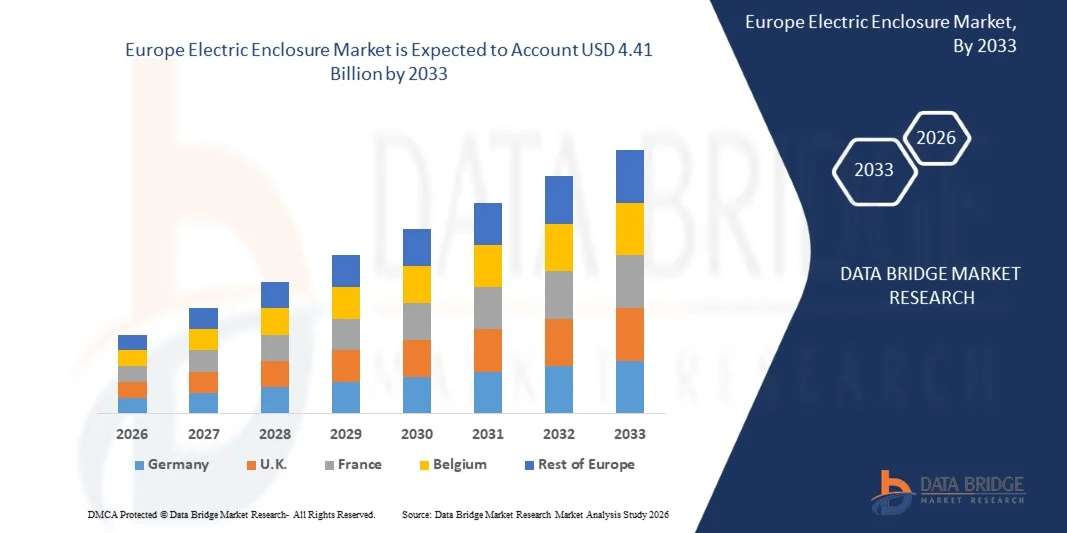

- As per Data Bridge Market Research Analysis the Europe Electric Enclosure Market size was valued at USD 2.50 Billion in 2025 and is expected to reach USD 4.41 Billion by 2033, at a CAGR of 7.4% during the forecast period

- Electric enclosure is a cabinet meant for electrical components where electrical or electronic equipment such as switches, knobs, and display are being mounted. It is used for securing content in harsh environment and also to protect people from electric shocks or explosion.

Market Size & Forecast

- Europe Market Value (2025): USD 2.50 Billion

- Expected Market Value (2033): USD 4.41 Billion

- Forecast CAGR (2026–2033): 7.4%

Europe Electric Enclosure Market Analysis

- The Europe Electric Enclosure Market is witnessing stable growth, driven by the increasing expansion of industrial automation, power distribution infrastructure, and renewable energy projects across the region.

- Rising investments in smart manufacturing, energy-efficient electrical systems, and industrial safety standards are significantly boosting the demand for electric enclosures used in protecting electrical and electronic components from environmental hazards, dust, moisture, and corrosion. Demand is particularly strong across industries such as power generation, oil & gas, automotive, transportation, food & beverage, and data centers, where reliable protection of electrical systems is essential for operational efficiency and workplace safety.

- The Germany is expected to dominate the market share 17.6% in 2025, Technological advancements and product innovation are playing a major role in shaping the market landscape, with manufacturers increasingly focusing on lightweight, corrosion-resistant, and modular enclosure solutions.

- U.K. is expected to witness the fastest growth during the forecast period CAGR 9.4%, driven by growing adoption of stainless steel, aluminum, and non-metallic enclosures is enhancing durability and performance across harsh industrial environments. In addition, the integration of smart monitoring systems, thermal management technologies, and IoT-enabled enclosure solutions is improving equipment protection and operational reliability.

- The Non Metallic segment is anticipated to hold the largest market share 63.5% in 2025 and anticipated to show the fastest growth during the forecast period CAGR, due to its superior corrosion resistance, lightweight properties, durability, and increasing suitability for harsh industrial and outdoor environments.

Report Scope and Europe Electric Enclosure Market Segmentation

|

Attributes |

Europe Electric Enclosure Market Key Market Insights |

|

Segments Covered |

· By Material/Product Type: Non Metallic, Metallic · By Mounting Type: Wall Mounted, Free Standing, Underground · By Usage: Indoor, Outdoor · By Application: Dust Tight, Hazardous Equipment, Drip Tight, Flame Explosion · By Design: Standard, Custom · By Form Factor: Compact Electric Enclosures, Free Size Electric Enclosures, Small Enclosures · By Vertical: Power Generation & Distribution, Oil & Gas, Medical, Food & Beverages, Metal & Mining, Transportation, Pulp & Paper |

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

What is the Key Trend in the Europe Electric Enclosure Market?

“Rapid Industrialization And Infrastructure Development In Emerging European Economies”

- Rapid industrialization and infrastructure development across emerging European economies is emerging as a key opportunity in the Europe Electric Enclosure Market. Countries across Eastern and Central Europe are increasingly investing in industrial expansion, transportation infrastructure, manufacturing facilities, utility modernization, and commercial construction projects to strengthen economic growth and industrial competitiveness.

- Electric enclosures are essential components used to protect electrical systems, control panels, automation equipment, and power distribution networks from environmental exposure, operational hazards, corrosion, moisture, and industrial contamination.

- In January 2026, the European Commission highlighted increasing infrastructure modernization and industrial development investments across emerging European economies to strengthen regional economic growth and industrial competitiveness.

- In September 2025, Eurostat reported continuous growth in manufacturing output and industrial construction activities across Eastern and Central European countries.

- In March 2025, the European Investment Bank announced financial support for infrastructure expansion, industrial modernization, and utility improvement projects across developing European regions.

Europe Electric Enclosure Market Dynamics

Driver

Increasing Expansion And Upgradation Of Power Transmission And Distribution Infrastructure Across Europe

- Increasing expansion and modernization of power transmission and distribution infrastructure across Europe is emerging as a major driver for the Europe Electric Enclosure Market. Governments, utility providers, and industrial operators across the region are significantly investing in upgrading aging electrical networks, strengthening cross-border electricity connectivity, and expanding high-voltage transmission systems to meet rising electricity demand and energy transition goals.

- In November 2025, the European Commission reported that substantial investments are being directed toward modernization and expansion of Europe’s electricity grids to support increasing electrification, industrial growth, and renewable energy integration across member states.

- In March 2025, the International Energy Agency stated that Europe continues to accelerate investments in transmission and distribution infrastructure modernization projects to improve grid reliability, operational efficiency, and long-term energy security, which is significantly increasing demand for electric enclosures used in substations, power control systems, and utility infrastructure protection applications across the European marke.

- In February 2026, Siemens Energy reported increasing investments in high-voltage transmission infrastructure and grid automation projects across Europe, supporting growth of electrical enclosure installations in utility applications and creating significant demand for advanced enclosure systems capable of protecting sensitive electrical and automation equipment under complex operating conditions.

- The increasing expansion and modernization of transmission and distribution infrastructure across Europe is significantly strengthening demand for advanced electric enclosure systems. Rising investments in smart grids, substations, industrial electrification, and cross-border electricity connectivity projects are accelerating deployment of protected electrical systems across utility and industrial applications.

Restraint/Challenge

High Technical Complexity Related To Enclosure Design, Customization, And System Integratio

- The Europe Electric Enclosure Market faces a significant challenge due to the high technical complexity associated with enclosure design, customization, and integration within modern electrical infrastructure systems. Electric enclosures used across industrial automation, renewable energy facilities, smart grids, transportation systems, and utility networks are required to meet highly specific operational, environmental, and safety requirements.

- Manufacturers must develop enclosure systems capable of protecting sensitive electrical and electronic equipment from moisture, corrosion, dust, vibration, electromagnetic interference, and temperature fluctuations while maintaining operational efficiency and regulatory compliance. Increasing deployment of digital substations, smart manufacturing systems, and intelligent power distribution technologies is further increasing demand for highly customized and technologically advanced enclosure solutions.

- In January 2026, the European Commission highlighted increasing technical requirements associated with modernization of electrical infrastructure and deployment of advanced digital energy systems across Europe, which is increasing complexity in design, customization, and integration of electric enclosure systems across utility and industrial applications.

- In September 2025, the International Energy Agency stated that integration of smart grid technologies and renewable energy systems is increasing engineering complexity within electricity infrastructure projects, thereby creating challenges for manufacturers developing advanced enclosure systems compatible with digitally integrated power networks.

- The high technical complexity associated with enclosure design, customization, and integration continues to remain a major challenge for the Europe Electric Enclosure Market. Increasing deployment of smart grids, industrial automation systems, renewable energy infrastructure, and digital power distribution technologies is significantly increasing demand for advanced enclosure systems capable of meeting strict operational and regulatory requirements.

Europe Electric Enclosure Market Scope

The Europe Electric Enclosure Market is categorized into seven notable segments which are based on the basis of material/product type, mounting type, usage, application, design, form factor and vertical.

- By Material/Product type

On the basis of Material/Product type, the Europe Electric Enclosure Market is segmented into metallic enclosures and non-metallic enclosures. In 2026, the non-metallic enclosures segment is expected to dominate the market share 63.7% due to its superior corrosion resistance, lightweight properties, durability, and increasing suitability for harsh industrial and outdoor environments.

The metallic enclosures segment is projected to grow with a 7.8% CAGR during the forecast period due to its high mechanical strength, enhanced protection capabilities, and extensive usage in heavy industrial and hazardous applications.

- By mounting type

On the basis of mounting type, the Europe Electric Enclosure Market is segmented into wall mounted enclosures, free standing enclosures, and underground electric enclosures. In 2026, the wall mounted enclosures segment is expected to dominate the market share 61.1% owing to its extensive utilization across industrial and commercial facilities, ease of installation, compact design, and suitability for both indoor and outdoor applications.

The underground electric enclosures segment is projected to grow with the 7.8% CAGR during the forecast period due to increasing investments in underground power distribution infrastructure and smart city development projects.

- By usage

On the basis of usage, the Europe Electric Enclosure Market is segmented into indoor and outdoor. In 2026, the indoor segment is expected to dominate the market share 67.9% due to the increasing installation of electrical control systems, switchgear equipment, and variable frequency drives within industrial manufacturing facilities and commercial infrastructure.

The outdoor segment is projected to grow with the 7.6% CAGR during the forecast period due to increasing investments in renewable energy projects, utility infrastructure, and outdoor telecommunications installations.

- By application

On the basis of application, the Europe Electric Enclosure Market is segmented into dust tight, hazardous equipment, drip tight, flame/explosion proof, and others. In 2026, the dust tight segment is expected to dominate the market share 42.5% due to the growing requirement for protection against dust, dirt, and airborne particles in industrial and manufacturing environments.

The flame/explosion proof segment is projected to grow with the 7.5% CAGR during the forecast period due to increasing safety regulations and rising adoption across oil & gas, chemical, and hazardous industrial facilities.

- By Design

On the basis of design, the Europe Electric Enclosure Market is segmented into standard and custom. In 2026, the standard segment is expected to dominate the market share 65.3% owing to its cost-effectiveness, wide availability, simplified installation process, and increasing preference across multiple industrial applications.

The custom segment is projected to grow with the 7.9% CAGR during the forecast period due to increasing demand for application-specific enclosure solutions tailored to complex industrial and automation requirements.

- By Form Factor

On the basis of form factor, the Europe Electric Enclosure Market is segmented into compact electric enclosures, free size electric enclosures, and small enclosures. In 2026, the compact electric enclosures segment is expected to dominate the market share 55.9% due to its high utilization across industrial automation, energy, and infrastructure applications requiring space-efficient enclosure solutions.

The custom segment is projected to grow with the 7.9% CAGR during the forecast period due to increasing demand for application-specific enclosure solutions tailored to complex industrial and automation requirements.

- By vertical

On the basis of vertical, the Europe Electric Enclosure Market is segmented into power generation and distribution, oil and gas, medical, food and beverage, metals and mining, transportation, pulp and paper, and others. In 2026, the power generation and distribution segment is expected to dominate the market share 34.2% due to the increasing demand for electrical safety systems, grid modernization projects, and expansion of renewable energy infrastructure across Europe.

The transportation segment is projected to grow with the 8.0% CAGR during the forecast period due to rising electrification initiatives, railway infrastructure expansion, and increasing deployment of smart transportation systems.

Europe Electric Enclosure Market Regional Analysis

Germany dominates the Electric Enclosure market with the largest revenue share of 17.7% in 2026, driven by the country’s strong industrial automation sector, advanced manufacturing infrastructure, and growing investments in renewable energy and smart grid projects. Increasing demand for reliable protection systems across automotive, machinery, power distribution, and industrial facilities continues to support market growth. In addition, the presence of leading enclosure manufacturers and rising adoption of Industry 4.0 technologies further accelerate demand for electric enclosures across the country.

France Electric Enclosure Market Insight

The France Electric Enclosure market captured a significant share of Europe electric enclosure revenue in 2026, supported by expanding investments in energy infrastructure, industrial modernization, and commercial construction activities. Growing deployment of electrical safety systems, rising automation across manufacturing industries, and increasing renewable energy installations are driving enclosure demand. Furthermore, stringent electrical safety regulations and the increasing adoption of compact and corrosion-resistant enclosure systems contribute to sustained market expansion in France.

U.K. Electric Enclosure Market Insight

The U.K. Electric Enclosure market is projected to grow steadily, driven by rising investments in data centers, transportation infrastructure, and industrial automation projects. Increasing focus on electrical safety, expansion of renewable energy facilities, and modernization of power distribution networks are significantly boosting demand for electric enclosures. Additionally, the growing need for weatherproof and durable enclosure systems in outdoor and harsh industrial environments continues to support market growth across the country.

Germany Electric Enclosure Market Insight

Germany’s electric enclosure market is driven by strong industrial automation, expanding renewable energy infrastructure, and rising investments in smart manufacturing. The country’s focus on Industry 4.0, electric vehicle production, and advanced power distribution systems is increasing demand for durable, high-protection enclosures across factories, utilities, and transportation applications.

France Electric Enclosure Market Insight

France’s electric enclosure market is supported by growing renewable energy deployment, modernization of electrical infrastructure, and increasing adoption of industrial automation systems. Rising investments in smart grids, rail transportation, and energy-efficient manufacturing facilities are boosting demand for corrosion-resistant and weatherproof enclosures in commercial, industrial, and utility sectors.

Electric Enclosure Market Share

The Electric Enclosure Market is primarily led by well-established companies, including:

- Rittal GmbH & Co. KG (Germany)

- ABB Ltd. (Switzerland)

- Eaton Corporation plc (Ireland)

- Legrand SA (France)

- Schneider Electric SE (France)

- nVent Electric plc (U.K.)

- Emerson Electric Co. (U.S.)

- Hubbell Incorporated (U.S.)

- Phoenix Mecano AG (Switzerland)

- Hager Group (Germany)

- GEWISS S.p.A. (Italy)

- Leviton Manufacturing Co., Inc. (U.S.)

- GE Vernova Inc. (U.S.)

- Omega Engineering, Inc. (U.S.)

- Fibox Oy Ab (Finland)

- Adalet (U.S.)

- Socomec Group (France)

- Deltron Enclosures (Australia)

- Eldon Holding AB (Sweden)

- Hammond Manufacturing Ltd. (Canada)

- Ensto Group (Finland)

- Adalet Global (U.S.)

- Fibox Group (Finland)

Latest Developments in Europe Electric Enclosure Market

- In August 2024, Schneider Electric highlighted that modernization of aging distribution networks and industrial electrical systems is accelerating installation of durable and weather-resistant enclosure solutions, thereby supporting market growth through increasing replacement demand for modern electrical protection infrastructure across Europe.

- In February 2026, Siemens Energy reported increasing investments in high-voltage transmission infrastructure and grid automation projects across Europe, supporting growth of electrical enclosure installations in utility applications and creating significant demand for advanced enclosure systems capable of protecting sensitive electrical and automation equipment under complex operating conditions.

- In May 2025, Hitachi Energy stated that rising deployment of smart substations and digital power infrastructure across Europe is increasing demand for advanced enclosure systems supporting electrical safety and operational reliability, which is accelerating adoption of technologically advanced and customized electric enclosure products across utility and industrial applications.

- In May 2025, ABB highlighted growing demand for weatherproof and corrosion-resistant electrical enclosures across renewable energy facilities including wind and solar installations, which is supporting market growth through increasing adoption of specialized enclosure systems designed for outdoor and utility-scale applications.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF EUROPE ELECTRIC ENCLOSURE MARKET

1.4 CURRENCY AND PRICING:

1.5 LIMITATION

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 DBMR VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELING

2.9 MATERIAL/PRODUCT TYPE TIMELINE CURVE

2.1 MARKET APPLICATION COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTER’S FIVE FORCES ANALYSIS

4.1.1 OVERVIEW

4.1.2 THREAT OF NEW ENTRANTS – MODERATE TO LOW

4.1.3 BARGAINING POWER OF SUPPLIERS – LOW TO MODERATE

4.1.4 BARGAINING POWER OF BUYERS – MODERATE TO HIGH

4.1.5 THREAT OF SUBSTITUTES – LOW

4.1.6 COMPETITIVE RIVALRY – HIGH

4.1.7 CONCLUSION

4.2 RAW MATERIAL/PRODUCT TYPE COVERAGE

4.2.1 METALLIC RAW MATERIAL/PRODUCT TYPES

4.2.2 CARBON STEEL

4.2.3 STAINLESS STEEL

4.2.4 ALUMINUM

4.2.5 NON-METALLIC RAW MATERIAL/PRODUCT TYPES

4.2.6 POLYCARBONATE

4.2.7 ABS (ACRYLONITRILE BUTADIENE STYRENE)

4.2.8 FIBERGLASS-REINFORCED POLYESTER (FRP/GRP)

4.2.9 KEY MARKET TRENDS: RAW MATERIAL/PRODUCT TYPES IN EUROPE ELECTRIC ENCLOSURE MARKET

4.2.10 RISING ADOPTION OF NON-METALLIC AND COMPOSITE MATERIAL/PRODUCT TYPES

4.2.11 INCREASING DEMAND FOR CORROSION-RESISTANT MATERIAL/PRODUCT TYPES

4.2.12 GROWING PREFERENCE FOR RECYCLABLE AND SUSTAINABLE MATERIAL/PRODUCT TYPES

4.2.13 VOLATILITY IN STEEL AND ALUMINUM PRICES

4.2.14 EXPANSION OF RENEWABLE ENERGY AND SMART INFRASTRUCTURE PROJECTS

4.2.15 SHIFT TOWARD LIGHTWEIGHT ENCLOSURE SOLUTIONS

4.2.16 TECHNOLOGICAL ADVANCEMENTS IN MATERIAL/PRODUCT TYPE ENGINEERING

4.2.17 CONCLUSION

4.3 CONSUMER BUYING BEHAVIOUR

4.3.1 INDUSTRIAL AUTOMATION BUYERS

4.3.2 UTILITY & POWER INFRASTRUCTURE OPERATORS

4.3.3 COMMERCIAL & CONSTRUCTION BUYERS

4.3.4 OEM & MACHINERY MANUFACTURERS

4.3.5 BUDGET-SENSITIVE SMALL ENTERPRISES

4.3.6 PREMIUM SMART INFRASTRUCTURE BUYERS

4.3.7 CONCLUSION

4.4 TECHNOLOGICAL ADVANCEMENTS

4.4.1 IOT-ENABLED SMART ENCLOSURES (REAL-TIME MONITORING + CLOUD CONNECTIVITY)

4.4.2 SMART THERMAL MANAGEMENT SYSTEMS (ENERGY-OPTIMIZED COOLING)

4.4.3 SENSOR-BASED CONDITION MONITORING (PREDICTIVE MAINTENANCE SYSTEMS)

4.4.4 INDUSTRIAL IOT INTERFACES AND PROTOCOL STANDARDIZATION

4.4.5 MODULAR & SYSTEM-BASED ENCLOSURE ENGINEERING

4.4.6 SUSTAINABLE MATERIAL/PRODUCT TYPES & ECO-DESIGN ENGINEERING

4.4.7 EDGE COMPUTING & MICRO DATA CENTER INTEGRATION

4.5 VALUE CHAIN ANALYSIS

4.5.1 RESEARCH AND DEVELOPMENT

4.5.2 RAW MATERIAL/PRODUCT TYPE SUPPLIERS (UPSTREAM)

4.5.3 COMPONENT & SUBSYSTEM SUPPLIERS

4.5.4 ELECTRIC ENCLOSURE MANUFACTURERS

4.5.5 SYSTEM INTEGRATORS & OEMS

4.5.6 DISTRIBUTION & CHANNEL PARTNERS

4.5.7 END USERS

4.5.8 SERVICE & LIFECYCLE (AFTERMARKET)

4.6 PATENT ANALYSIS

4.6.1 EP4531508A1 (SCHNEIDER ELECTRIC – MICRO DATA CENTER / POWER DISTRIBUTION ENCLOSURE SYSTEM)

4.6.2 TECHNICAL SUMMARY

4.6.3 KEY INNOVATION HIGHLIGHTS

4.6.4 TECHNICAL EFFECTS / ADVANTAGES

4.6.5 STRATEGIC IMPORTANCE (MARKET VIEW)

4.6.6 PATENT 2: EP4485721A1 (ABB SCHWEIZ AG – PRESSURIZED METAL ELECTRICAL ENCLOSURE SYSTEM)

4.6.7 TECHNICAL SUMMARY

4.6.8 KEY INNOVATION HIGHLIGHTS

4.6.9 TECHNICAL EFFECTS / ADVANTAGES

4.6.10 STRATEGIC IMPORTANCE

4.6.11 KEY PATENT TRENDS IN EUROPE ELECTRIC ENCLOSURE MARKET

4.6.12 SHIFT TOWARD SMART AND IOT-ENABLED ENCLOSURES

4.6.13 STRONG GROWTH IN MODULAR AND CONFIGURABLE ENCLOSURE DESIGNS

4.6.14 ADVANCEMENT IN THERMAL MANAGEMENT AND HIGH-DENSITY DESIGN

4.6.15 RISING FOCUS ON SUSTAINABLE AND ECO-DESIGNED ENCLOSURES

4.6.16 INCREASED PATENTING IN SAFETY, IP PROTECTION, AND HARSH-ENVIRONMENT SYSTEMS

4.6.17 INTEGRATION OF DIGITALIZATION AND INDUSTRY 4.0 ECOSYSTEMS

4.7 PROFIT MARGINS SCENARIO

4.7.1 MARGIN DRIVERS IN EUROPE

4.7.2 MARGIN PRESSURE FACTORS

4.7.3 BENCHMARK FROM ELECTRICAL EQUIPMENT INDUSTRY

4.8 INNOVATION TRACKER AND STRATEGIC ANALYSIS

4.8.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.8.2 JOINT VENTURES

4.8.3 MERGERS AND ACQUISITIONS

4.8.4 LICENSING AND PARTNERSHIP

4.8.5 TECHNOLOGY COLLABORATIONS

4.8.6 STRATEGIC DIVESTMENTS

4.8.7 NUMBER OF PRODUCTS IN DEVELOPMENT

4.8.8 STAGE OF DEVELOPMENT

4.8.9 TIMELINES AND MILESTONES

4.8.10 INNOVATION STRATEGIES AND METHODOLOGIES

4.8.11 RISK ASSESSMENT AND MITIGATION

4.8.12 FUTURE OUTLOOK

4.9 PRICING ANALYSIS

4.1 SUPPLY CHAIN ANALYSIS

4.10.1 OVERVIEW:

4.10.2 RAW MATERIAL/PRODUCT TYPE SUPPLIERS:

4.10.3 COMPONENT & SUBSYSTEM SUPPLIERS:

4.10.4 ELECTRIC ENCLOSURE MANUFACTURERS (OEMS):

4.10.5 DISTRIBUTION CHANNELS:

4.10.6 SYSTEM INTEGRATORS & PANEL BUILDERS:

4.10.7 END-USE INDUSTRIES:

4.10.8 CONCLUSION:

4.11 INDUSTRY ECOSYSTEM ANALYSIS

4.11.1 PROMINENT COMPANIES

4.11.2 SMALL & MEDIUM SIZE COMPANIES

4.11.3 END USERS

4.12 IMPACT OF WAR ON SUPPLY CHAIN, GEOGRAPHIC FOOTPRINT & STRUCTURAL SHIFTS AND ADAPTIVE STRATEGIES

4.12.1 IMPACT OF WAR ON SUPPLY CHAIN

4.12.2 RAW MATERIAL/PRODUCT TYPE SUPPLY SHOCK

4.12.3 ENERGY CRISIS AND MANUFACTURING COST ESCALATION

4.12.4 LOGISTICS AND TRANSPORTATION DISRUPTIONS

4.12.5 DISRUPTION OF INDUSTRIAL ELECTRONICS & AUTOMATION COMPONENTS

4.12.6 SUPPLY CHAIN FRAGMENTATION AND SUPPLIER REQUALIFICATION

4.12.7 TRACEABILITY AND COMPLIANCE CHALLENGES

4.12.8 SHIFT FROM LEAN SUPPLY CHAINS TO RESILIENT SUPPLY CHAINS

4.12.9 TRACEABILITY AND COMPLIANCE CHALLENGES

4.12.10 GEOGRAPHIC FOOTPRINT CHANGES

4.12.11 REDUCED DEPENDENCE ON EASTERN SUPPLY CORRIDORS

4.12.12 REGIONALIZATION OF MANUFACTURING

4.12.13 SHIFT TOWARD “FRIENDSHORING” AND “CHINA+1” STRATEGIES

4.12.14 EXPANSION AROUND RENEWABLE ENERGY CORRIDORS

4.12.15 STRUCTURAL SHIFTS IN THE MARKET

4.12.16 SHIFT FROM GLOBALIZED TO RESILIENT SUPPLY CHAINS

4.12.17 REINDUSTRIALIZATION AND STRATEGIC AUTONOMY IN EUROPE

4.12.18 DEFENSE, ENERGY SECURITY, AND INFRASTRUCTURE-LED DEMAND SHIFT

4.12.19 SUPPLY CHAIN RECONFIGURATION AND REGIONALIZATION OF PRODUCTION

4.12.20 INDUSTRIAL POLICY SHIFT TOWARD PROTECTIONISM AND LOCAL CONTENT REQUIREMENTS

4.12.21 VALUE CHAIN UPGRADING AND INDUSTRY SPECIALIZATION

4.12.22 ADAPTIVE STRATEGIES

4.12.23 SUPPLIER DIVERSIFICATION

4.12.24 NEARSHORING AND LOCAL MANUFACTURING EXPANSION

4.12.25 STRATEGIC INVENTORY AND BUFFER STOCK MANAGEMENT

4.12.26 DIGITAL SUPPLY CHAIN VISIBILITY AND RISK MONITORING

4.12.27 MATERIAL/PRODUCT TYPE INNOVATION AND PRODUCT REDESIGN

4.12.28 FOCUS ON HIGH-GROWTH AND RESILIENT END MARKETS

4.13 VALUE CHAIN ANALYSIS

4.13.1 RESEARCH AND DEVELOPMENT

4.13.2 RAW MATERIAL/PRODUCT TYPE SUPPLIERS (UPSTREAM)

4.13.3 COMPONENT & SUBSYSTEM SUPPLIERS

4.13.4 ELECTRIC ENCLOSURE MANUFACTURERS

4.13.5 SYSTEM INTEGRATORS & OEMS

4.13.6 DISTRIBUTION & CHANNEL PARTNERS

4.13.7 END USERS

4.13.8 SERVICE & LIFECYCLE (AFTERMARKET)

4.14 SALES CHANNEL ANALYSIS

4.14.1 DIRECT SALES CHANNEL ANALYSIS

4.14.2 INDIRECT SALE CHANNEL ANALYSIS

5 TARIFFS AND IMPACT ON THE MARKET

5.1 CURRENT TARIFF RATE(S) IN TOP-5 COUNTRY MARKETS

5.2 OUTLOOK: LOCAL PRODUCTION V/S IMPORT RELIANCE

5.3 VENDOR SELECTION CRITERIA DYNAMICS

5.4 IMPACT ON SUPPLY CHAIN

5.4.1 RAW MATERIAL/PRODUCT TYPE PROCUREMENT

5.4.2 MANUFACTURING AND PRODUCTION

5.4.3 LOGISTICS AND DISTRIBUTION

5.4.4 PRICE PITCHING AND POSITION OF MARKET

5.5 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.5.1 SUPPLY CHAIN OPTIMIZATION

5.5.2 JOINT VENTURE ESTABLISHMENTS

5.6 IMPACT ON PRICES

5.7 REGULATORY INCLINATION

5.7.1 GEOPOLITICAL SITUATION

5.7.2 TRADE PARTNERSHIPS BETWEEN THE COUNTRIES

5.7.2.1 FREE TRADE AGREEMENTS

5.7.2.2 ALLIANCES ESTABLISHMENTS

5.7.3 STATUS ACCREDITION (INCLUDING MFN)

5.7.4 DOMESTIC COURSE OF CORRECTION

5.7.4.1 INCENTIVE SCHEMES TO BOOST PRODUCTION OUTPUTS

5.7.4.2 ESTABLISHMENT OF SPECIAL ECONOMIC ZONES / INDUSTRIAL PARKS

6 REGULATION COVERAGE

6.1 PRODUCT CODES

6.2 CERTIFIED STANDARDS

6.3 SAFETY STANDARDS

6.3.1 MATERIAL/PRODUCT TYPE HANDLING & STORAGE

6.3.2 TRANSPORT & PRECAUTIONS

6.3.3 HAZARD IDENTIFICATION

6.4 CONCLUSION

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 INCREASING EXPANSION AND UPGRADATION OF POWER TRANSMISSION AND DISTRIBUTION INFRASTRUCTURE ACROSS EUROPE.

7.1.2 GROWING INTEGRATION OF RENEWABLE ENERGY SOURCES REQUIRING ADVANCED ELECTRICAL PROTECTION SYSTEMS.

7.1.3 RISING DEMAND FOR RELIABLE AND SECURE ELECTRICAL NETWORKS TO SUPPORT GRID STABILITY AND RURAL ELECTRIFICATION.

7.1.4 ONGOING MODERNIZATION AND REPLACEMENT OF AGING ELECTRICAL INFRASTRUCTURE ACROSS INDUSTRIAL AND UTILITY SECTORS.

7.2 RESTRAINTS

7.2.1 HIGH INITIAL CAPITAL INVESTMENT ASSOCIATED WITH ADVANCED ELECTRIC ENCLOSURE INSTALLATION AND INTEGRATION

7.2.2 AVAILABILITY OF ALTERNATIVE PROTECTION AND HOUSING SOLUTIONS LIMITING MARKET PENETRATION.

7.3 OPPORTUNITIES

7.3.1 RAPID INDUSTRIALIZATION AND INFRASTRUCTURE DEVELOPMENT IN EMERGING EUROPEAN ECONOMIES.

7.3.2 INCREASING DEMAND FOR COMPACT, SPACE-EFFICIENT, AND WEATHER-RESISTANT ELECTRIC ENCLOSURE SOLUTIONS

7.3.3 GROWING DEPLOYMENT OF SMART GRID TECHNOLOGIES AND INTELLIGENT POWER DISTRIBUTION SYSTEMS.

7.4 CHALLENGES

7.4.1 HIGH TECHNICAL COMPLEXITY RELATED TO ENCLOSURE DESIGN, CUSTOMIZATION, AND SYSTEM INTEGRATIO

7.4.2 SUPPLY CHAIN DISRUPTIONS AND VOLATILITY IN RAW MATERIAL/PRODUCT TYPE PRICES IMPACTING MANUFACTURING COSTS AND DELIVERY TIMELINES

8 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE

8.1 OVERVIEW

8.2 NON METALLIC

8.3 METALLIC

8.4 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

8.4.1 NON METALLIC

8.4.2 METALLIC

8.5 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY AVERAGE SELLING PRICE, 2018-2033, (USD PER UNIT)

8.5.1 NON METALLIC

8.5.2 METALLIC

8.6 STAINLESS STEEL

8.7 ALUMINIUM

8.8 MILD STEEL

8.9 EUROPE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

8.9.1 STAINLESS STEEL

8.9.2 MILD STEEL

8.9.3 ALUMINIUM

8.1 EUROPE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

8.10.1 FIBERGLASS ENCLOSURES

8.10.2 POLYCARBONATE ENCLOSURES

8.10.3 POLYESTER ENCLOSURES

8.10.4 PVC ENCLOSURES

8.10.5 ACRYLINITRILE-BUTADIENE-STYRENE

8.10.6 OTHERS

8.11 EUROPE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

8.11.1 POLYESTER ENCLOSURES

8.11.2 FIBERGLASS ENCLOSURES

8.11.3 PVC ENCLOSURES

8.11.4 ACRYLINITRILE-BUTADIENE-STYRENE

8.11.5 POLYCARBONATE ENCLOSURES

8.11.6 OTHERS

9 EUROPE ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE

9.1 OVERVIEW

9.2 WALL MOUNTED ENCLOSURE

9.3 FREE STANDING ENCLOSURE

9.4 UNDERGROUND ELECTRIC ENCLOSURE

9.5 EUROPE WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

9.5.1 STANDARD

9.5.2 CUSTOM

9.6 EUROPE STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

9.6.1 NON METALLIC

9.6.2 METALLIC

9.7 EUROPE NON METALLIC STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

9.7.1 POLYCARBONATE

9.7.2 FIBERGLASS

9.7.3 POLYSTER

9.7.4 ABS

9.7.5 PVC

9.7.6 OTHERS

10 EUROPE ELECTRIC ENCLOSURE MARKET, BY USAGE

10.1 OVERVIEW

10.2 INDOOR

10.3 OUTDOOR

11 EUROPE ELECTRIC ENCLOSURE MARKET, BY APPLICATION

11.1 OVERVIEW

11.2 DUST TIGHT

11.3 HAZARDOUS EQUIPMENT

11.4 DRIP TIGHT

11.5 FLAME EXPLOSION

11.6 OTHERS

12 EUROPE ELECTRIC ENCLOSURE MARKET, BY DESIGN

12.1 OVERVIEW

12.2 STANDARD

12.3 CUSTOM

13 EUROPE ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR

13.1 OVERVIEW

13.2 COMPACT ELECTRIC ENCLOSURES

13.3 FREE SIZE ELECTRIC ENCLOSURES

13.4 SMALL ENCLOSURES

13.5 EUROPE SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

13.5.1 ALUMINIUM ENCLOSURES

13.5.2 ELECTRICAL BOX ENCLOSURES

13.5.3 BUS ENCLOSURES

13.6 EUROPE COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

13.6.1 SLOPED ROOF ENCLOSURES

13.6.2 HYGIENIC DESIGN ENCLOSURES

13.6.3 MINING ENCLOSURE

13.6.4 SINGLE STANDING ENCLOSURES

13.7 EUROPE FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

13.7.1 SYSTEM ENCLOSURES

13.7.2 OPERATOR CONSOLES

13.7.3 BAYING SYSTEMS

14 EUROPE ELECTRIC ENCLOSURE MARKET, BY VERTICAL

14.1 OVERVIEW

14.2 POWER GENERATION AND DISTRIBUTION

14.3 OIL AND GAS

14.4 MEDICAL

14.5 FOOD AND BEVERAGES

14.6 METAL AND MINNING

14.7 TRANSPORTATION

14.8 PULP AND PAPER

14.9 OTHERS

14.1 EUROPE TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

14.10.1 ROADWAYS

14.10.2 RAILWAYS

14.10.3 AIRWAYS

15 EUROPE ELECTRIC ENCLOSURE MARKET, BY COUNTRY

15.1 EUROPE

15.1.1 GERMANY

15.1.2 U.K.

15.1.3 FRANCE

15.1.4 ITALY

15.1.5 SPAIN

15.1.6 NETHERLANDS

15.1.7 SWITZERLAND

15.1.8 SWEDEN

15.1.9 DENMARK

15.1.10 TURKEY

15.1.11 FINLAND

15.1.12 RUSSIA

15.1.13 BELGIUM

15.1.14 NORWAY

15.1.15 ICELAND

15.1.16 REST OF EUROPE

16 EUROPE ELECTRIC ENCLOSURE MARKET COMPANY LANDSCAPE

16.1 COMPANY SHARE ANALYSIS: EUROPE

17 SWOT ANALYSIS

18 COMPANY PROFILE

18.1 SCHNEIDER ELECTRIC

18.1.1 COMPANY SNAPSHOT

18.1.2 REVENUE ANALYSIS

18.1.3 PRODUCT PORTFOLIO

18.1.4 RECENT DEVELOPMENT/NEWS

18.2 ABB

18.2.1 COMPANY SNAPSHOT

18.2.2 REVENUE ANALYSIS

18.2.3 PRODUCT PORTFOLIO

18.2.4 RECENT DEVELOPMENT/NEWS

18.3 RITTAL LLC

18.3.1 COMPANY SNAPSHOT

18.3.2 PRODUCT PORTFOLIO

18.3.3 RECENT DEVELOPMENTS

18.4 EATON

18.4.1 COMPANY SNAPSHOT

18.4.2 REVENUE ANALYSIS

18.4.3 PRODUCT PORTFOLIO

18.4.4 RECENT DEVELOPMENT

18.5 LEGRAND

18.5.1 COMPANY SNAPSHOT

18.5.2 REVENUE ANALYSIS

18.5.3 PRODUCT PORTFOLIO

18.5.4 RECENT DEVELOPMENT/NEWS

18.6 ADALETENCLOSURES

18.6.1 COMPANY SNAPSHOT

18.6.2 PRODUCT PORTFOLIO

18.6.3 RECENT DEVELOPMENTS

18.7 AZZ INC.

18.7.1 COMPANY SNAPSHOT

18.7.2 REVENUE ANALYSIS

18.7.3 PRODUCT PORTFOLIO

18.7.4 RECENT DEVELOPMENTS

18.8 CUBIC-MODULSYSTEM A/S

18.8.1 COMPANY SNAPSHOT

18.8.2 PRODUCT PORTFOLIO

18.8.3 RECENT DEVELOPMENT

18.9 DELTRON ENCLOSURES

18.9.1 COMPANY SNAPSHOT

18.9.2 PRODUCT PORTFOLIO

18.9.3 RECENT DEVELOPMENTS

18.1 ELDON HOLDING AB

18.10.1 COMPANY SNAPSHOT

18.10.2 PRODUCT PORTFOLIO

18.10.3 RECENT DEVELOPMENTS

18.11 EMERSON ELECTRIC CO.

18.11.1 COMPANY SNAPSHOT

18.11.2 REVENUE ANALYSIS

18.11.3 PRODUCT PORTFOLIO

18.11.4 RECENT DEVELOPMENTS

18.12 ENSTO GROUP

18.12.1 COMPANY SNAPSHOT

18.12.2 PRODUCT PORTFOLIO

18.12.3 RECENT DEVELOPMENTS

18.13 FIBOX

18.13.1 COMPANY SNAPSHOT

18.13.2 PRODUCT PORTFOLIO

18.13.3 RECENT DEVELOPMENTS

18.14 FEEL - FLAMEPROOF ELECTRICAL ENCLOSURES LTD.

18.14.1 COMPANY SNAPSHOT

18.14.2 PRODUCT PORTFOLIO

18.14.3 RECENT DEVELOPMENT

18.15 GE VERNOVA

18.15.1 COMPANY SNAPSHOT

18.15.2 PRODUCT PORTFOLIO

18.15.3 RECENT DEVELOPMENTS

18.16 GEWISS S.P.A.

18.16.1 COMPANY SNAPSHOT

18.16.2 PRODUCT PORTFOLIO

18.16.3 RECENT DEVELOPMENT

18.17 HAGER GROUP (BOCCHIOTTI)

18.17.1 COMPANY SNAPSHOT

18.17.2 PRODUCT PORTFOLIO

18.17.3 RECENT DEVELOPMENTS

18.18 HAMMOND MANUFACTURING LTD.

18.18.1 COMPANY SNAPSHOT

18.18.2 REVENUE ANALYSIS

18.18.3 PRODUCT PORTFOLIO

18.18.4 RECENT DEVELOPMENTS

18.19 HUBBELL

18.19.1 COMPANY SNAPSHOT

18.19.2 REVENUE ANALYSIS

18.19.3 PRODUCT PORTFOLIO

18.19.4 RECENT DEVELOPMENTS

18.2 LEVITON MANUFACTURING CO., INC.

18.20.1 COMPANY SNAPSHOT

18.20.2 PRODUCT PORTFOLIO

18.20.3 RECENT DEVELOPMENTS

18.21 MCAREE ENGINEERING LTD.

18.21.1 COMPANY SNAPSHOT

18.21.2 PRODUCT PORTFOLIO

18.21.3 RECENT DEVELOPMENTS

18.22 NVENT

18.22.1 COMPANY SNAPSHOT

18.22.2 REVENUE ANALYSIS

18.22.3 PRODUCT PORTFOLIO

18.22.4 RECENT DEVELOPMENTS

18.23 OMEGA ENGINEERING, INC. (A SUBSIDIARY OF SPECTRIS PLC)

18.23.1 COMPANY SNAPSHOT

18.23.2 PRODUCT PORTFOLIO

18.23.3 RECENT DEVELOPMENTS

18.24 PHOENIX MECANO AG

18.24.1 COMPANY SNAPSHOT

18.24.2 REVENUE ANALYSIS

18.24.3 PRODUCT PORTFOLIO FOR BOPLA GEHÄUSE SYSTEME GMBH

18.24.4 PRODUCT PORTFOLIO FOR ROSE SYSTEMTECHNIK GMBH

18.24.5 RECENT DEVELOPMENTS

18.25 SOCOMEC

18.25.1 COMPANY SNAPSHOT

18.25.2 PRODUCT PORTFOLIO

18.25.3 RECENT DEVELOPMENTS

19 QUESTIONNAIRE

20 RELATED REPORTS

List of Table

TABLE 1 COMPARATIVE OVERVIEW OF RAW MATERIAL/PRODUCT TYPES

TABLE 2 CONSUMER BUYING BEHAVIOUR

TABLE 3 LIST OF POTENTIAL CUSTOMERS:

TABLE 4 BASIC PATENT INFORMATION

TABLE 5 BASIC PATENT INFORMATION

TABLE 6 ESTIMATED PROFIT MARGIN STRUCTURE

TABLE 7 TYPICAL MARGIN SCENARIO BY PRODUCT CATEGORY

TABLE 8 SCENARIO OUTLOOK (2026–20303)

TABLE 9 LIST OF POTENTIAL CUSTOMERS:

TABLE 10 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 11 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 12 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY AVERAGE SELLING PRICE, 2018-2033, (USD PER UNIT)

TABLE 13 EUROPE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 14 EUROPE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 15 EUROPE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 16 EUROPE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 17 EUROPE ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 18 EUROPE WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 19 EUROPE STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 20 EUROPE NON METALLIC STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 21 EUROPE ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 22 EUROPE ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 23 EUROPE ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 24 EUROPE ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 25 EUROPE SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 26 EUROPE COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 27 EUROPE FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 28 EUROPE ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 29 EUROPE TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 30 EUROPE ELECTRIC ENCLOSURE MARKET, BY COUNTRY, 2018-2033, (USD MILLION)

TABLE 31 EUROPE ELECTRIC ENCLOSURE MARKET, BY COUNTRY, 2018-2033 (MILLION UNITS)

TABLE 32 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 33 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 34 EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY AVERAGE SELLING PRICE, 2018-2033, (USD PER UNIT)

TABLE 35 EUROPE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 36 EUROPE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 37 EUROPE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 38 EUROPE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 39 EUROPE ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 40 EUROPE WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 41 EUROPE STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 42 EUROPE NON METALLIC STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 43 EUROPE ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 44 EUROPE ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 45 EUROPE ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 46 EUROPE ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 47 EUROPE SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 48 EUROPE COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 49 EUROPE FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 50 EUROPE ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 51 EUROPE TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 52 GERMANY ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 53 GERMANY ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 54 GERMANY METALLIC ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY AVERAGE SELLING PRICE, 2018-2033, (USD PER UNIT)

TABLE 55 GERMANY METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 56 GERMANY METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 57 GERMANY NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 58 GERMANY NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 59 GERMANY ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 60 GERMANY WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 61 GERMANY STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 62 GERMANY NON METALLIC STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 63 GERMANY ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 64 GERMANY ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 65 GERMANY ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 66 GERMANY ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 67 GERMANY SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 68 GERMANY COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 69 GERMANY FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 70 GERMANY ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 71 GERMANY TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 72 U.K. ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 73 U.K. METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 74 U.K. NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 75 U.K. ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 76 U.K. ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 77 U.K. ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 78 U.K. ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 79 U.K. ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 80 U.K. SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 81 U.K. COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 82 U.K. FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 83 U.K. ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 84 U.K. TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 85 FRANCE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 86 FRANCE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 87 FRANCE METALLIC ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY AVERAGE SELLING PRICE, 2018-2033, (USD PER UNIT)

TABLE 88 FRANCE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 89 FRANCE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 90 FRANCE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 91 FRANCE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 92 FRANCE ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 93 FRANCE WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 94 FRANCE STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 95 FRANCE NON METALLIC STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 96 FRANCE ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 97 FRANCE ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 98 FRANCE ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 99 FRANCE ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 100 FRANCE SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 101 FRANCE COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 102 FRANCE FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 103 FRANCE ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 104 FRANCE TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 105 ITALY ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 106 ITALY ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 107 ITALY METALLIC ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY AVERAGE SELLING PRICE, 2018-2033, (USD MILLION)

TABLE 108 ITALY METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 109 ITALY METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 110 ITALY NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 111 ITALY NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 112 ITALY ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 113 ITALY WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 114 ITALY STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 115 ITALY NON METALLIC STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 116 ITALY ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 117 ITALY ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 118 ITALY ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 119 ITALY ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 120 ITALY SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 121 ITALY COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 122 ITALY FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 123 ITALY ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 124 ITALY TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 125 SPAIN ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 126 SPAIN ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 127 SPAIN METALLIC ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY AVERAGE SELLING PRICE, 2018-2033, (USD MILLION)

TABLE 128 SPAIN METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 129 SPAIN METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 130 SPAIN NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 131 SPAIN NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 132 SPAIN ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 133 SPAIN WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 134 SPAIN STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 135 SPAIN NON METALLIC STANDARD WALL MOUNTED ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 136 SPAIN ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 137 SPAIN ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 138 SPAIN ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 139 SPAIN ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 140 SPAIN SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 141 SPAIN COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 142 SPAIN FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 143 SPAIN ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 144 SPAIN TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 145 NETHERLANDS ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 146 NETHERLANDS METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 147 NETHERLANDS NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 148 NETHERLANDS ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 149 NETHERLANDS ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 150 NETHERLANDS ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 151 NETHERLANDS ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 152 NETHERLANDS ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 153 NETHERLANDS SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 154 NETHERLANDS COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 155 NETHERLANDS FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 156 NETHERLANDS ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 157 NETHERLANDS TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 158 SWITZERLAND ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 159 SWITZERLAND METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 160 SWITZERLAND NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 161 SWITZERLAND ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 162 SWITZERLAND ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 163 SWITZERLAND ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 164 SWITZERLAND ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 165 SWITZERLAND ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 166 SWITZERLAND SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 167 SWITZERLAND COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 168 SWITZERLAND FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 169 SWITZERLAND ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 170 SWITZERLAND TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 171 SWEDEN ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 172 SWEDEN METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 173 SWEDEN NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 174 SWEDEN ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 175 SWEDEN ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 176 SWEDEN ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 177 SWEDEN ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 178 SWEDEN ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 179 SWEDEN SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 180 SWEDEN COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 181 SWEDEN FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 182 SWEDEN ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 183 SWEDEN TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 184 DENMARK ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 185 DENMARK METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 186 DENMARK NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 187 DENMARK ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 188 DENMARK ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 189 DENMARK ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 190 DENMARK ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 191 DENMARK ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 192 DENMARK SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 193 DENMARK COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 194 DENMARK FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 195 DENMARK ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 196 DENMARK TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 197 TURKEY ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 198 TURKEY METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 199 TURKEY NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 200 TURKEY ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 201 TURKEY ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 202 TURKEY ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 203 TURKEY ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 204 TURKEY ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 205 TURKEY SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 206 TURKEY COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 207 TURKEY FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 208 TURKEY ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 209 TURKEY TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 210 FINLAND ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 211 FINLAND METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 212 FINLAND NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 213 FINLAND ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 214 FINLAND ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 215 FINLAND ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 216 FINLAND ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 217 FINLAND ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 218 FINLAND SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 219 FINLAND COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 220 FINLAND FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 221 FINLAND ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 222 FINLAND TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 223 RUSSIA ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 224 RUSSIA METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 225 RUSSIA NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 226 RUSSIA ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 227 RUSSIA ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 228 RUSSIA ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 229 RUSSIA ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 230 RUSSIA ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 231 RUSSIA SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 232 RUSSIA COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 233 RUSSIA FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 234 RUSSIA ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 235 RUSSIA TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 236 BELGIUM ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 237 BELGIUM METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 238 BELGIUM NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 239 BELGIUM ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 240 BELGIUM ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 241 BELGIUM ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 242 BELGIUM ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 243 BELGIUM ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 244 BELGIUM SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 245 BELGIUM COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 246 BELGIUM FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 247 BELGIUM ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 248 BELGIUM TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 249 NORWAY ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 250 NORWAY METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 251 NORWAY NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 252 NORWAY ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 253 NORWAY ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 254 NORWAY ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 255 NORWAY ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 256 NORWAY ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 257 NORWAY SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 258 NORWAY COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 259 NORWAY FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 260 NORWAY ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 261 NORWAY TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 262 ICELAND ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 263 ICELAND METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 264 ICELAND NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 265 ICELAND ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 266 ICELAND ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 267 ICELAND ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 268 ICELAND ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 269 ICELAND ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 270 ICELAND SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 271 ICELAND COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 272 ICELAND FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 273 ICELAND ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 274 ICELAND TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 275 REST OF EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2018-2033, (USD MILLION)

TABLE 276 REST OF EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 277 REST OF EUROPE METALLIC ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, BY AVERAGE SELLING PRICE, 2018-2033, (USD PER UNIT)

TABLE 278 REST OF EUROPE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 279 REST OF EUROPE METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 280 REST OF EUROPE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 281 REST OF EUROPE NON METALLIC ELECTRIC ENCLOSURE MARKET, BY TYPE, BY VOLUME, 2018-2033, (MILLION UNITS)

TABLE 282 REST OF EUROPE ELECTRIC ENCLOSURE MARKET, BY MOUNTING TYPE, 2018-2033, (USD MILLION)

TABLE 283 REST OF EUROPE ELECTRIC ENCLOSURE MARKET, BY USAGE, 2018-2033, (USD MILLION)

TABLE 284 REST OF EUROPE ELECTRIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033, (USD MILLION)

TABLE 285 REST OF EUROPE ELECTRIC ENCLOSURE MARKET, BY DESIGN, 2018-2033, (USD MILLION)

TABLE 286 REST OF EUROPE ELECTRIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033, (USD MILLION)

TABLE 287 REST OF EUROPE SMALL ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 288 REST OF EUROPE COMPACT ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 289 REST OF EUROPE FREE SIZE ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

TABLE 290 REST OF EUROPE ELECTRIC ENCLOSURE MARKET, BY VERTICAL, 2018-2033, (USD MILLION)

TABLE 291 REST OF EUROPE TRANSPORTATION IN ELECTRIC ENCLOSURE MARKET, BY TYPE, 2018-2033, (USD MILLION)

List of Figure

FIGURE 1 EUROPE ELECTRIC ENCLOSURE MARKET: SEGMENTATION

FIGURE 2 EUROPE ELECTRIC ENCLOSURE MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE ELECTRIC ENCLOSURE MARKET: DROC ANALYSIS

FIGURE 4 EUROPE ELECTRIC ENCLOSURE MARKET: REGIONAL VS COUNTRY MARKET ANALYSIS

FIGURE 5 EUROPE ELECTRIC ENCLOSURE MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE ELECTRIC ENCLOSURE MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE ELECTRIC ENCLOSURE MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE ELECTRIC ENCLOSURE MARKET: DBMR VENDOR SHARE ANALYSIS

FIGURE 9 EUROPE ELECTRIC ENCLOSURE MARKET: MULTIVARIVATE MODELING

FIGURE 10 EUROPE ELECTRIC ENCLOSURE MARKET: MATERIAL/PRODUCT TYPE TIMELINE CURVE

FIGURE 11 EUROPE ELECTRIC ENCLOSURE MARKET: APPLICATION COVERAGE GRID

FIGURE 12 EUROPE ELECTRIC ENCLOSURE MARKET: SEGMENTATION

FIGURE 13 TWO SEGMENTS COMPRISE THE EUROPE ELECTRIC ENCLOSURE MARKET, BY MATERIAL/PRODUCT TYPE (2025)

FIGURE 14 GERMANY IS EXPECTED TO DOMINATE THE MARKET FOR EUROPE ELECTRIC ENCLOSURE MARKET WHEREAS U.K. IS EXPECTED TO BE GROWING WITH THE HIGHEST CAGR IN THE FORECAST PERIOD OF 2026 TO 2033

FIGURE 15 EUROPE ELECTRIC ENCLOSURE MARKET: EXECUTIVE SUMMARY

FIGURE 16 RISING DEMAND FOR RELIABLE AND SECURE ELECTRICAL NETWORKS TO SUPPORT GRID STABILITY AND RURAL ELECTRIFICATION ARE EXPECTED TO DRIVE EUROPE ELECTRIC ENCLOSURE MARKET IN THE FORECAST PERIOD OF 2026 TO 2033

FIGURE 17 NON-METALLIC SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE ELECTRIC ENCLOSURE MARKET IN 2025 & 2033

FIGURE 18 VALUE CHAIN ANALYSIS

FIGURE 19 NUMBER OF GRANTED EUROPEAN PATENTS FOR ELECTRIC ENCLOSURE FROM 2020-2025

FIGURE 20 AVERAGE SELLING PRICE (ASP) OF THE EUROPE ELECTRIC ENCLOSURE MARKET, BY, BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2020-2025 (USD PER UNIT)

FIGURE 21 VALUE CHAIN ANALYSIS

FIGURE 22 DROC ANALYSIS

FIGURE 23 EUROPE ELECTRIC ENCLOSURE MARKET: BY MATERIAL/PRODUCT TYPE/PRODUCT TYPE, 2025

FIGURE 24 EUROPE ELECTRIC ENCLOSURE MARKET: BY MOUNTING TYPE, 2025

FIGURE 25 EUROPE ELECTRIC ENCLOSURE MARKET: BY USAGE, 2025

FIGURE 26 EUROPE ELECTRIC ENCLOSURE MARKET: BY APPLICATION, 2025

FIGURE 27 EUROPE ELECTRIC ENCLOSURE MARKET: BY DESIGN, 2025

FIGURE 28 EUROPE ELECTRIC ENCLOSURE MARKET: BY FORM FACTOR, 2025

FIGURE 29 EUROPE ELECTRIC ENCLOSURE MARKET: BY VERTICAL, 2025

FIGURE 30 EUROPE ELECTRIC ENCLOSURE MARKET, SNAPSHOT (2025)

FIGURE 31 EUROPE ELECTRIC ENCLOSURE MARKET: COMPANY SHARE 2025 (%)

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.