Europe Bone Metastasis Market

Market Size in USD Billion

CAGR :

%

USD

3.54 Billion

USD

6.64 Billion

2025

2033

USD

3.54 Billion

USD

6.64 Billion

2025

2033

| 2026 –2033 | |

| USD 3.54 Billion | |

| USD 6.64 Billion | |

| % | |

|

Europe Bone Metastasis Market Size

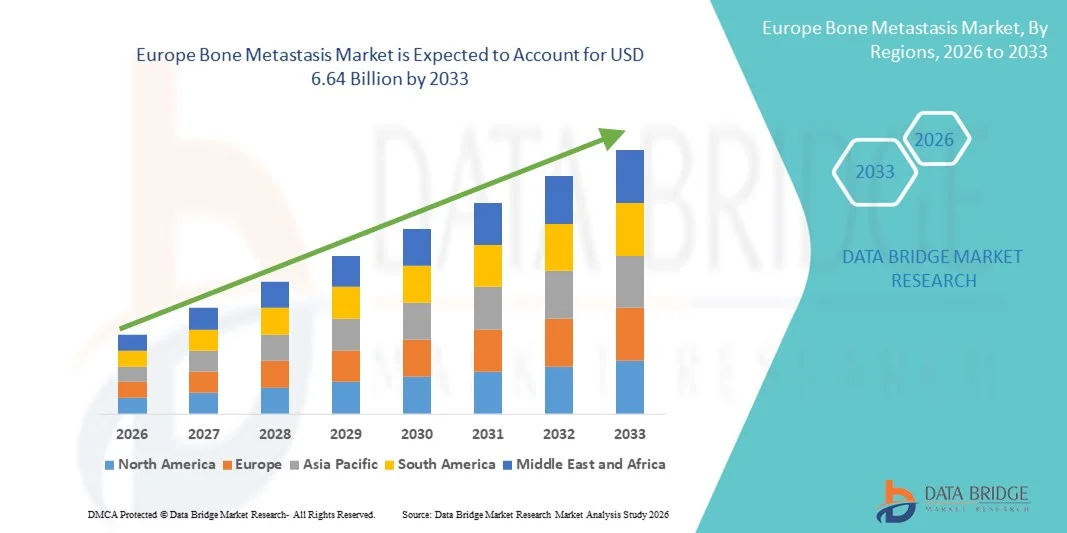

- The Europe bone metastasis market size was valued at USD 3.54 billion in 2025 and is expected to reach USD 6.64 billion by 2033, at a CAGR of 8.20% during the forecast period

- The market growth is largely fueled by rising incidence of cancers that frequently metastasize to bone, coupled with robust pharmaceutical R&D and improved access to advanced therapeutic and diagnostic solutions across European healthcare systems

- Furthermore, growing emphasis on early detection, personalized oncology care, and supportive regulatory frameworks for novel treatments are strengthening adoption of bone metastasis therapies across countries such as Germany, the UK, and France. These converging factors are accelerating uptake of innovative treatment regimens, thereby significantly boosting the industry’s growth

Europe Bone Metastasis Market Analysis

- Bone metastasis management in Europe, including diagnostic and therapeutic solutions such as radiopharmaceuticals, bisphosphonates, and targeted therapies, is increasingly vital in oncology care due to its role in early detection, pain management, and prevention of skeletal-related events across both hospital and outpatient settings

- The escalating demand for bone metastasis solutions is primarily fueled by rising incidence of cancers that commonly metastasize to bone, including breast, prostate, and lung cancers, growing awareness among clinicians and patients of advanced treatment options, and ongoing innovations in both diagnostic and therapeutic modalities that improve patient outcomes

- Germany dominated the Europe bone metastasis market with the largest revenue share of 24.7% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative therapies, and strong presence of key pharmaceutical players, with robust treatment uptake in hospitals and specialty clinics

- The United Kingdom is expected to be the fastest-growing country in the Europe bone metastasis market during the forecast period due to increasing cancer prevalence, expanding access to advanced diagnostics and therapeutics, and supportive government policies for oncology care

- Osteoclasts segment dominated the Europe bone metastasis market with a market share of 40.9% in 2025, driven by therapies that inhibit osteoclastic activity to prevent bone degradation

Report Scope and Europe Bone Metastasis Market Segmentation

|

Attributes |

Europe Bone Metastasis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Bone Metastasis Market Trends

Personalized and Targeted Therapy Adoption

- A significant and accelerating trend in the Europe bone metastasis market is the growing adoption of personalized and targeted therapies, including radiopharmaceuticals, bisphosphonates, and monoclonal antibodies, which improve efficacy and reduce side effects in patients with bone metastatic conditions

- For instance, radium-223 dichloride therapy is increasingly prescribed for metastatic prostate cancer patients to specifically target bone lesions, reducing tumor burden while preserving healthy bone tissue

- Targeted therapy adoption enables clinicians to design patient-specific treatment regimens based on genetic markers, prior response to therapies, and disease progression, thereby optimizing clinical outcomes and minimizing unnecessary toxicity

- The integration of diagnostic biomarkers with treatment planning allows early detection of skeletal-related events, timely intervention, and monitoring of therapeutic response, significantly improving quality of life for patients

- This trend toward more personalized and targeted interventions is reshaping treatment protocols, with pharmaceutical companies such as Bayer and Novartis developing next-generation bone-targeted therapies with enhanced efficacy and safety profiles

- The demand for therapies that are both disease-specific and patient-specific is growing rapidly across hospitals, specialty clinics, and outpatient oncology centers, as clinicians prioritize outcomes and quality of life in metastatic bone cancer management

- Increasing use of digital health tools, such as remote patient monitoring and AI-assisted imaging analysis, is enabling clinicians to better track treatment response and adjust therapy plans in real time

Europe Bone Metastasis Market Dynamics

Driver

Increasing Cancer Incidence and Awareness of Advanced Therapies

- The rising prevalence of cancers such as breast, prostate, and lung, which frequently metastasize to bone, coupled with increasing awareness of advanced treatment options, is a significant driver for the Europe bone metastasis market

- For instance, in March 2025, Novartis reported enhanced uptake of their bone-targeted therapies across multiple European oncology centers, reflecting heightened clinician awareness and patient access to effective treatments

- As clinicians and patients recognize the importance of early intervention and skeletal complication management, therapies targeting bone metastasis are increasingly prescribed, driving market adoption

- Furthermore, healthcare infrastructure improvements and reimbursement policies in countries such as Germany, France, and the UK support widespread access to both diagnostics and therapies for metastatic bone conditions

- The integration of bone metastasis treatments into standard oncology protocols, alongside growing clinical trial activity, is reinforcing their adoption in both inpatient and outpatient care settings, driving consistent market growth

- Improved patient education, awareness campaigns, and oncology specialist recommendations are further accelerating demand for targeted bone metastasis treatments across European healthcare systems

- Advancements in minimally invasive diagnostic and interventional procedures are supporting earlier detection and localized treatment of bone lesions, expanding the eligible patient population for therapies

- Collaborations between pharmaceutical companies and academic research centers are accelerating the development of next-generation therapies, fostering innovation and faster adoption across Europe

Restraint/Challenge

High Treatment Costs and Limited Access in Some Countries

- The high cost of advanced therapies, combined with limited access to specialized oncology centers in certain European countries, poses a significant challenge to market growth

- For instance, some therapies such as monoclonal antibodies and radiopharmaceuticals may be unaffordable or unavailable in smaller healthcare facilities, limiting patient reach despite clinical benefits

- Ensuring equitable access requires reimbursement coverage, government support, and regional distribution of treatments, which remain inconsistent across Europe, impacting overall adoption rates

- In addition, the complexity of administering certain injectable or infusion-based therapies in hospital or outpatient settings can restrict patient convenience and increase reliance on specialized staff

- While new oral and home-administered options are emerging, the higher perceived cost and infrastructure requirements for traditional therapies still pose a barrier for price-sensitive patients or smaller clinics

- Overcoming these challenges through improved access programs, cost-reduction strategies, and increased availability of outpatient-compatible therapies is vital for sustained growth in the Europe bone metastasis market

- Regulatory hurdles for approval of novel therapies, particularly radiopharmaceuticals and gene-targeted treatments, can delay market entry and limit availability in some countries

- Limited awareness among patients in rural areas regarding advanced treatment options can reduce therapy uptake, necessitating targeted education and outreach programs by healthcare providers

Europe Bone Metastasis Market Scope

The market is segmented on the basis of disease type, type of therapy, route of administration, population type, mode of purchase, end-user, and distribution channel.

- By Disease Type

On the basis of disease type, the Europe bone metastasis market is segmented into osteoblastic and osteoclasts. The osteoclasts segment dominated the market with the largest revenue share of 40.9% in 2025, driven by the widespread use of therapies that inhibit osteoclastic activity to prevent bone degradation and reduce skeletal-related complications. Patients with cancers that commonly metastasize to bone, such as breast and prostate cancer, benefit from osteoclast-targeted therapies, which slow disease progression and improve quality of life. Strong clinical evidence supporting bisphosphonates and RANK ligand inhibitors as effective agents further reinforces the dominance of this segment. Hospitals and oncology centers prioritize osteoclast-directed treatments due to their proven efficacy and integration into standard care protocols. In addition, favorable reimbursement policies in Western European countries enhance adoption. Pharmaceutical companies are actively expanding the portfolio of osteoclast-targeted agents, which maintains this segment’s market leadership.

The osteoblastic segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing research on agents that promote bone formation and improve structural integrity. Osteoblastic therapies are increasingly used in combination with other targeted treatments to enhance patient outcomes. Emerging clinical trials demonstrating efficacy in metastatic bone lesions are driving adoption among oncology specialists. The segment benefits from growing awareness of supportive therapies that complement conventional treatment regimens. Countries with advanced healthcare infrastructure, such as Germany and the UK, are leading early adoption. The trend toward personalized oncology care and biomarker-guided therapy further accelerates growth in this segment.

- By Type

On the basis of type, the Europe bone metastasis market is segmented into diagnosis and treatment. The treatment segment dominated the market with the largest revenue share in 2025, driven by widespread adoption of bisphosphonates, radiopharmaceuticals, and targeted therapies to manage skeletal complications and pain. Hospitals and specialty oncology clinics prioritize treatment options that reduce hospitalizations and improve quality of life. Robust clinical trial data demonstrating therapeutic efficacy reinforces clinician confidence. Advanced treatment options, including combination therapies with chemotherapy or immunotherapy, further strengthen market demand. Insurance coverage and reimbursement policies in countries such as France, Germany, and the UK support adoption. Pharmaceutical innovation, coupled with growing patient awareness, contributes to the segment’s continued dominance.

The diagnosis segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for early detection and monitoring of bone metastases through advanced imaging and biomarkers. PET-CT, MRI, and novel bone biomarkers enable timely intervention and personalized treatment planning. Hospitals and specialty clinics are increasingly investing in diagnostic technologies to support evidence-based therapy decisions. Increasing awareness of skeletal-related complications among clinicians drives the need for more frequent monitoring. Research on AI-assisted imaging and predictive analytics further accelerates growth. The rising focus on preventive oncology and early-stage intervention supports sustained expansion of the diagnostic segment.

- By Route of Administration

On the basis of route of administration, the Europe bone metastasis market is segmented into oral, parenteral, and others. The parenteral segment dominated the market with the largest revenue share in 2025 due to the widespread use of injectable bisphosphonates, monoclonal antibodies, and radiopharmaceuticals in clinical settings. Hospitals and outpatient oncology centers prefer parenteral administration for accurate dosing and controlled delivery. Parenteral therapies are integral to managing severe bone metastasis complications and are often required for patients with advanced disease. Regulatory approvals and clinical evidence supporting efficacy enhance adoption. Pharmaceutical companies are continuously expanding parenteral therapy portfolios, sustaining market leadership. The segment benefits from integration into standard care protocols in Western European countries.

The oral segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the introduction of orally bioavailable agents that offer convenience, improved patient adherence, and outpatient compatibility. Oral therapies enable home-based treatment, reducing hospital visits and associated costs. Increasing patient preference for less invasive options supports segment growth. Pharmaceutical innovation in oral formulations, such as selective bone-targeted agents, further accelerates adoption. Eastern European countries with growing access to modern oncology treatments are contributing to higher uptake. The trend toward personalized, patient-friendly therapy regimens enhances long-term growth prospects for oral administration.

- By Population Type

On the basis of population type, the Europe bone metastasis market is segmented into children and adults. The adults segment dominated the market with the largest revenue share in 2025, reflecting the higher prevalence of cancers that metastasize to bone, such as prostate, breast, and lung cancer, in adult populations. Treatment protocols and therapy options are primarily designed for adults, supporting strong adoption in hospitals and specialty oncology centers. Advanced therapies are often tailored to adult patient needs, including dosing and safety considerations. The segment benefits from comprehensive insurance coverage and government-supported oncology programs in Western Europe. Ongoing clinical trials targeting adult bone metastasis populations further reinforce dominance. Rising awareness of skeletal-related complications among adults drives continuous growth.

The children segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing focus on pediatric oncology and supportive bone metastasis therapies. Rare pediatric cancers with potential bone involvement are being diagnosed earlier due to better imaging and biomarker use. Hospitals and specialty pediatric oncology centers are investing in child-specific treatment protocols. Pharmaceutical companies are developing pediatric-friendly formulations and dosing strategies. Awareness campaigns and early detection programs further support growth. Personalized treatment approaches for pediatric patients accelerate market expansion in this segment.

- By Mode of Purchase

On the basis of mode of purchase, the Europe bone metastasis market is segmented into over the counter (OTC) and prescription. The prescription segment dominated the market with the largest revenue share in 2025, driven by regulatory requirements for controlled use of both diagnostics and therapeutic agents for bone metastasis. Hospitals, specialty clinics, and pharmacies primarily distribute prescription-based treatments. Prescription therapies offer targeted efficacy and safety profiles, supporting clinician confidence. Reimbursement coverage in European countries facilitates higher adoption. Advanced therapies, including monoclonal antibodies and radiopharmaceuticals, are exclusively prescription-based. Ongoing innovation in targeted treatments reinforces the segment’s leadership.

The OTC segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the rising availability of supportive care products such as calcium, vitamin D supplements, and pain management agents. Patients and caregivers increasingly seek convenient, self-managed solutions for bone health. Retail pharmacies and online platforms are expanding access to OTC products. Awareness campaigns regarding bone health and skeletal complication prevention support adoption. OTC formulations are gaining popularity in home healthcare and ambulatory care settings. Growth is further accelerated by an aging population seeking preventive and adjunctive therapies.

- By End-User

On the basis of end-user, the Europe bone metastasis market is segmented into hospitals, specialty clinics, home healthcare, ambulatory surgical centers, and others. The hospitals segment dominated the market with the largest revenue share in 2025 due to centralized oncology services, multidisciplinary care teams, and availability of advanced diagnostics and therapies. Hospitals serve as primary treatment hubs for complex cases requiring parenteral or radiopharmaceutical therapies. Government support and insurance reimbursement facilitate adoption in hospitals. Hospitals also lead in clinical trial participation and early access programs. Access to specialized staff and equipment enhances treatment efficacy. The segment benefits from continuous R&D collaborations with pharmaceutical companies.

The home healthcare segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of home-administered injectable therapies, oral agents, and remote patient monitoring solutions. Patients and caregivers increasingly prefer home-based care to reduce hospital visits. Telemedicine and digital health tools facilitate supervision of home treatments. Home healthcare expansion is supported by healthcare policies encouraging outpatient care. The segment is particularly growing in countries with high aging populations, such as Italy and Spain. Convenience, cost reduction, and patient comfort accelerate market uptake in this segment.

- By Distribution Channel

On the basis of distribution channel, the Europe bone metastasis market is segmented into direct tender, hospital pharmacies, online pharmacies, retail pharmacies, and others. The hospital pharmacies segment dominated the market with the largest revenue share in 2025 due to the centralized distribution of prescription therapies and advanced diagnostics. Hospital pharmacies ensure compliance with regulatory requirements and proper handling of parenteral and radiopharmaceutical treatments. Hospitals maintain strong procurement relationships with pharmaceutical manufacturers. Controlled access ensures safety and proper dosing. Hospital pharmacies also facilitate integration of therapies into multidisciplinary treatment protocols. The segment is reinforced by government reimbursement and insurance coverage.

The online pharmacies segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing patient preference for convenient access to supportive care products, oral medications, and prescription fulfillment. Digital platforms enable home delivery, adherence tracking, and teleconsultation integration. Online pharmacies are expanding rapidly in countries with strong e-commerce adoption, such as the UK and Germany. Rising awareness about bone metastasis management supports online sales. Expansion of online channels reduces geographic disparities in access. Convenience, privacy, and lower costs accelerate adoption in this segment.

Europe Bone Metastasis Market Regional Analysis

- Germany dominated the Europe bone metastasis market with the largest revenue share of 24.7% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative therapies, and strong presence of key pharmaceutical players, with robust treatment uptake in hospitals and specialty clinics

- Patients and clinicians in Germany highly value early detection, advanced diagnostics, and targeted treatment options, including bisphosphonates, radiopharmaceuticals, and monoclonal antibodies, which improve patient outcomes and quality of life

- This widespread adoption is further supported by favorable reimbursement policies, robust clinical research activity, and government initiatives promoting cancer care, establishing Germany as a leading country for both adult and pediatric bone metastasis management

The U.K. Bone Metastasis Market Insight

The U.K. bone metastasis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing cancer prevalence and rising demand for targeted and personalized therapies. Clinicians and patients are increasingly prioritizing early detection and intervention to manage skeletal-related events effectively. Hospitals and specialty oncology clinics are expanding access to advanced treatment options, including bisphosphonates, radiopharmaceuticals, and monoclonal antibodies. Strong government support, well-established healthcare infrastructure, and reimbursement schemes facilitate adoption of novel therapies. The U.K.’s focus on integrating diagnostics with treatment planning supports evidence-based care. Patient education initiatives and growing awareness of metastatic bone disease management are further propelling market growth.

Germany Bone Metastasis Market Insight

The Germany bone metastasis market captured the largest revenue during the forecast period, fueled by high adoption of innovative therapies and strong clinical research activity. Germany’s advanced healthcare system, specialized oncology centers, and supportive insurance coverage promote uptake of bone-targeted therapies. Increasing awareness among physicians and patients regarding early diagnosis, skeletal-related event management, and quality-of-life improvements drives market expansion. Hospitals and specialty clinics are investing in cutting-edge diagnostics, such as PET-CT and MRI, to enable personalized therapy selection. Government initiatives supporting oncology programs further strengthen adoption. Collaboration between pharmaceutical companies and research institutes accelerates the introduction of next-generation therapies in Germany.

France Bone Metastasis Market Insight

The France bone metastasis market is projected to witness steady growth during the forecast period, driven by rising cancer prevalence and expanding access to advanced bone-targeted therapies. Clinicians are increasingly integrating treatment protocols combining bisphosphonates, radiopharmaceuticals, and supportive care products for effective management of skeletal complications. Strong hospital infrastructure and reimbursement support facilitate adoption in both public and private healthcare settings. Awareness campaigns highlighting early detection and preventive strategies for skeletal-related events are boosting patient engagement. In addition, France is actively involved in clinical trials for novel therapeutics, fostering innovation and adoption. The focus on personalized treatment strategies enhances the market’s growth trajectory.

Italy Bone Metastasis Market Insight

The Italy bone metastasis market is expected to grow at a considerable CAGR due to rising incidence of cancers that metastasize to bone, coupled with growing awareness of advanced therapies and diagnostics. Hospitals and specialty oncology centers are increasingly adopting targeted treatments, including bisphosphonates, monoclonal antibodies, and radiopharmaceuticals. Government reimbursement policies and insurance coverage enhance patient access. The integration of diagnostics with therapy planning is enabling personalized care approaches. Efforts to improve quality of life through pain management and skeletal complication prevention are driving therapy adoption. Collaborative research initiatives and clinical trials in Italy support continuous innovation in bone metastasis management.

Europe Bone Metastasis Market Share

The Europe Bone Metastasis industry is primarily led by well-established companies, including:

- Amgen Inc. (U.S.)

- Novartis AG (Switzerland)

- F. Hoffmann La Roche Ltd (Switzerland)

- Pfizer Inc. (U.S.)

- Bayer AG (Germany)

- Eli Lilly and Company (U.S.)

- AstraZeneca (U.K.)

- Merck & Co., Inc. (U.S.)

- Bristol Myers Squibb Company (U.S.)

- Dr. Reddy’s Laboratories Ltd. (India)

- Fresenius Kabi AG (Germany)

- Viatris Inc. (U.S.)

- General Electric Company (GE Healthcare) (U.S.)

- Sanofi S.A. (France)

- Takeda Pharmaceutical Company Limited (Japan)

- AbbVie Inc. (U.S.)

- Cipla Limited (India)

- Ipsen Biopharmaceuticals (France)

What are the Recent Developments in Europe Bone Metastasis Market?

- In December 2025, the European Commission approved multiple denosumab biosimilars (including AVT03 marketed as Kefdensis®, Zvogra®, Ponlimsi®, and Degevma® across Europe), broadening the competitive biosimilar landscape for prevention of skeletal‑related events and treatment of bone loss associated with metastatic cancer, which is expected to increase access and lower patient costs

- In September 2025, Quantum Surgical’s Epione® robotic platform obtained CE mark approval for use in treating bone tumors and bone metastases, enabling minimally invasive percutaneous ablation and bone consolidation procedures, representing a significant technological advancement in interventional treatment options for metastatic bone lesions

- In July 2025, the European Commission authorized Biocon Biologics’ denosumab biosimilars Vevzuo® and Evfraxy®, aimed at prevention of skeletal‑related events in adults with advanced cancer involving bone and other bone‑health indications, underscoring growing access to more affordable biologic options in Europe

- In April 2025, the European Medicines Agency’s CHMP adopted a positive opinion recommending marketing authorization for Enwylma, a denosumab‑based monoclonal antibody for preventing bone complications in adults with advanced cancer involving bone and treating giant cell tumor of bone, signaling upcoming expanded access to this therapy in Europe

- In May 2024, Sandoz received European Commission approval for Wyost® and Jubbonti®, the first biosimilars of denosumab (reference drugs Xgeva® and Prolia®) in Europe, expanding treatment options for cancer‑related bone disease and osteoporosis with medicines that match the reference products in safety, efficacy, and quality

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.