Asia-Pacific Polyols Market Analysis and Size

Polyols are organic compounds. This organic compound is a compound that contains carbon covalently bound to other atoms, especially carbon-carbon, and carbon-hydrogen. A class of polyols called sugar alcohols includes those that are derived from sugars. They may occur naturally or produce industrially. The growing demand for polyurethane foams, increasing demand in the construction and infrastructure sector, and increasing focus on energy-efficient insulation materials, and sustainable products are the major factors that act as a driving factor for the Asia-Pacific polyols market. However, environmental regulations and sustainability concerns, high costs associated with polyols are acting as a restraining factors for the growth of the Asia-Pacific polyols market. Increasing demand for polyols for packaging materials, usage of polyols in insulation applications, and growing demand for bio-based are estimated to provide opportunities for Asia-Pacific polyols market growth. However, fluctuations in raw material prices and technological limitations, and performance requirements are creating a challenging environment for the Asia-Pacific polyols market growth.

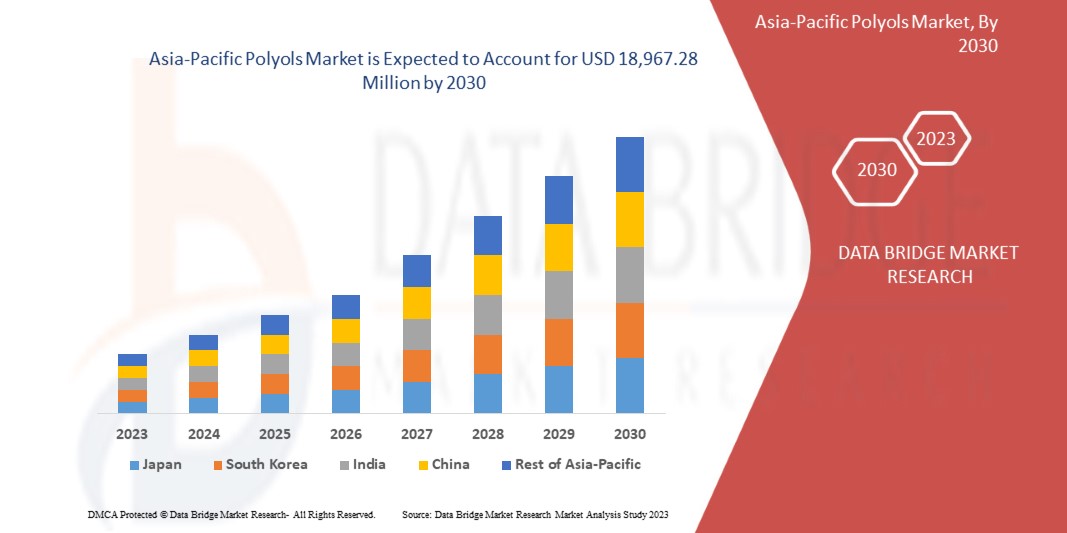

Data Bridge Market Research analyses that the Asia-Pacific polyols market is expected to reach a value of USD 18,967.28 million by 2030, at a CAGR of 6.2% during the forecast period. The Asia-Pacific polyols market report also comprehensively covers pricing analysis, patent analysis, and technological advancements.

|

Report Metric |

Details |

|

Forecast Period |

2023 to 2030 |

|

Base Year |

2022 |

|

Historic Years |

2021 (Customizable to 2015 - 2020) |

|

Quantitative Units |

Revenue in USD Million |

|

Segments Covered |

Type (Polyether Polyols and Polyester Polyols), Application (Flexible Polyurethane Foam, Rigid Polyurethane Foam, Coatings, Adhesive & Sealants, Elastomers, and Others), End User (Construction, Furniture, Transport, Packaging, Carpet Backing, and Others) |

|

Countries Covered |

China, Japan, South Korea, India, Australia and New Zealand, Singapore, Indonesia, Thailand, Malaysia, Philippines, and Rest of Asia-Pacific. |

|

Market Players Covered |

Huntsman International LLC, Repsol, Biesterfeld AG, DIC CORPORATION, Tosoh Corporation, Arkema, BASF SE, Dow, Cargill, Incorporated, LANXESS, Shell plc, Mitsubishi Chemical Corporation, Vertellus, Wanhua, Stepan Company, Gulshan Polyols Ltd, Perstorp Holding AB (Subsidiary of PETRONAS Chemicals Group), Emery Oleochemicals LLC, Covestro AG, Coim Group, and Shakun Industries, among others |

Market Definition

Polyols are alcohols with more than one hydroxyl group and they constitute one of the main raw materials for manufacturing polyurethane. They are commonly used as key raw materials in manufacturing various products, such as polyurethane foams, coatings, adhesives, sealants, elastomers, and more. Polyols are primarily derived from petrochemical sources or renewable resources like vegetable oils and sugar derivatives. They can be classified into different types based on their chemical structure, including polyether polyols and polyester polyols. Each type possesses specific properties and is suitable for different applications. The different types of polyols are polyether polyols and polyester polyols. The polyols are being used in different applications in different forms such as flexible polyurethane foam, rigid polyurethane foam, coatings, adhesives & sealants, elastomers, and others. Polyurethanes are versatile, modern, and safe. They have a huge range of applications for creating all kinds of industrial products and consumer basics to make our life more practical, comfortable, and environmentally friendly. Polyurethane is made up of plastic material presented and is available in various forms. It can be used in various forms such as rigid or flexible and is preferred based on material in a wide range of applications. One such polyol is Repsol which offers a portfolio of polyether polyols developed with home-grown technology with a wide range of alternatives.

Asia-Pacific Polyols Market Dynamics

This section deals with understanding the market drivers, advantages, opportunities, restraints, and challenges. All of this is discussed in detail below:

Drivers

- Growing Demand for Polyurethane Foams

Polyols are one of the two main components used in the production of polyurethane foams, with the other component being isocyanates. Polyols are polymeric compounds that contain multiple hydroxyl (-OH) functional groups. They can be derived from various sources, such as petroleum, vegetable oils, or polyesters. In the manufacturing process of polyurethane foam, polyols are reacted with isocyanates to form a polymer network. The growing demand for polyurethane foams is expected to drive the Asia-Pacific polyol market. Polyurethane foams are versatile materials used in various industries such as construction, automotive, furniture, and packaging due to their excellent insulation, cushioning, and durability properties.

Opportunity

- Increasing Demand for Polyols for Packaging Materials

The packaging materials are used to enclose, protect, and contain products for storage, distribution, and sale. Packaging serves various functions, including preserving the quality and integrity of products, ensuring their safety during transportation, providing information to consumers, and facilitating convenience in handling and storage. Packaging materials can be made from a wide range of materials, including plastics, paper and cardboard, glass, metals, and composite materials. Packaging materials play a vital role in ensuring the safety, preservation, and presentation of products. They contribute to the overall consumer experience and provide essential information about the product, such as ingredients, nutritional values, and usage instructions. Effective packaging materials help protect products from damage, extend their shelf life, and enhance their marketability

Restraints/Challenges

- High Cost Associated With Polyols

The cost of polyols is dependent on various factors such as raw materials, manufacturing process, and market demand. The prices of raw materials used for the production of polyols, such as propylene oxide and ethylene oxide, are volatile and can fluctuate frequently, leading to an increase in the production cost of polyols. Additionally, the production process for polyols is complex and requires specialized equipment and expertise, leading to higher capital and operating costs.

- Fluctuation In Raw Material Prices

The raw materials for polyol production can vary depending on the type of polyol being produced such as polyether polyols and polyester polyols.

Recent Developments

- In September 2022, Covestro AG announced the launch of polyether polyols based on bio-circular raw materials. The company will be able to offer selective prepolymers for various adhesive applications and their customer base. The main components for polyurethanes will be based on alternative raw materials. This step helps the company to offer substitutes to various industries and enhance its brand image in the market.

- In September 2022, Wanhua announced the launch of a new chemical that has developed a bio-based polyol to reduce its carbon footprint. The new bioproducts have been launched to contribute towards a sustainable environment and to increase production efficiency. This will help the company to enhance its product portfolio for the company.

Asia-Pacific Polyols Market Scope

The Asia-Pacific polyols market is segmented into three notable segments based type, application, and end user. The growth amongst these segments will help you analyse meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Type

- Polyether Polyols

- Polyester Polyols

On the basis of type, the Asia-Pacific polyols market is segmented into polyether polyols and polyester polyols.

Application

- Flexible Polyurethane Foam

- Rigid Polyurethane Foam

- Coatings

- Adhesives & Sealants

- Elastomers

- Others

On the basis of application, the Asia-Pacific polyols market is segmented into flexible polyurethane foam, rigid polyurethane foam, coatings, adhesives & sealants, elastomers, and others.

End User

- Construction

- Furniture

- Transport

- Packaging

- Carpet Backing

- Others

On the basis of end user, the Asia-Pacific polyols market is segmented into construction, furniture, transport, packaging, carpet backing, and others.

Asia-Pacific Polyols Market Regional Analysis/Insights

Asia-Pacific polyols market is analysed, and market size insights and trends are provided by country, type, application, and end user as referenced above.

The countries covered in the Asia-Pacific polyols market report are China, Japan, South Korea, India, Australia and New Zealand, Singapore, Indonesia, Thailand, Malaysia, the Philippines, and the rest of Asia-Pacific.

China is expected to dominate the Asia-Pacific polyols market as China has a massive manufacturing capacity and is known as the world's factory. The country has a vast network of production facilities, skilled labor, and cost-effective manufacturing processes. This enables China to produce polyol products in large quantities, meeting both domestic and international demand.

The region section of the report also provides individual market-impacting factors and changes in market regulation that impact the current and future trends of the market. Data points like downstream and upstream value chain analysis, technical trends, and Porter’s five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of Asia-Pacific brands and their challenges faced due to large or scarce competition from local and domestic brands, the impact of domestic tariffs, and trade routes are considered while providing forecast analysis of the region data.

Competitive Landscape and Asia-Pacific Polyols Market Share Analysis

The Asia-Pacific polyols market competitive landscape provides details of the competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, Asia-Pacific presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, and application dominance. The above data points provided are only related to the companies' focus related to Asia-Pacific polyols market.

Some of the major players operating in the Asia-Pacific polyols market are, Huntsman International LLC, Repsol, Biesterfeld AG, DIC CORPORATION, Tosoh Corporation, Arkema, BASF SE, Dow, Cargill, Incorporated, LANXESS, Shell plc, Mitsubishi Chemical Corporation, Vertellus, Wanhua, Stepan Company, Gulshan Polyols Ltd, Perstorp Holding AB (Subsidiary of PETRONAS Chemicals Group), Emery Oleochemicals LLC, Covestro AG, Coim Group, and Shakun Industries, among others.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE ASIA-PACIFIC POLYOLS MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 YEARS CONSIDERED FOR THE STUDY

2.3 GEOGRAPHIC SCOPE

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELLING

2.9 TYPE CURVE

2.1 MARKET APPLICATION COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 IMPORT-EXPORT DATA

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 GROWING DEMAND FOR POLYURETHANE FOAMS

5.1.2 INCREASING DEMAND IN THE CONSTRUCTION AND INFRASTRUCTURE SECTOR

5.1.3 ADVANCEMENTS IN POLYOLS TECHNOLOGY

5.1.4 GROWING DEMAND IN THE AUTOMOTIVE INDUSTRY

5.2 RESTRAINTS

5.2.1 ENVIRONMENTAL REGULATIONS AND SUSTAINABILITY CONCERNS

5.2.2 HIGH COST ASSOCIATED WITH POLYOLS

5.3 OPPORTUNITIES

5.3.1 INCREASING DEMAND FOR POLYOLS FOR PACKAGING MATERIALS

5.3.2 USE OF POLYOLS IN INSULATION APPLICATIONS

5.3.3 INCREASING PARTNERSHIP, ACQUISITION, AND COLLABORATION AMONG MARKET PLAYERS

5.3.4 HIGH DEMAND FOR BIO-BASED AND SUSTAINABLE POLYOLS

5.4 CHALLENGES

5.4.1 FLUCTUATION IN RAW MATERIAL PRICES

5.4.2 TECHNOLOGICAL LIMITATIONS AND PERFORMANCE REQUIREMENTS

6 ASIA-PACIFIC POLYOLS MARKET, BY TYPE

6.1 OVERVIEW

6.2 POLYETHER POLYOLS

6.3 POLYESTER POLYOLS

7 ASIA-PACIFIC POLYOLS MARKET, BY APPLICATION

7.1 OVERVIEW

7.2 FLEXIBLE POLYURETHANE FOAM

7.3 RIGID POLYURETHANE FOAM

7.4 COATINGS

7.5 ADHESIVES & SEALANTS

7.6 ELASTOMERS

7.7 OTHERS

8 ASIA-PACIFIC POLYOLS MARKET, BY END USER

8.1 OVERVIEW

8.2 CONSTRUCTION

8.2.1 POLYETHER POLYOLS

8.2.2 POLYESTER POLYOLS

8.3 FURNITURE

8.3.1 POLYETHER POLYOLS

8.3.2 POLYESTER POLYOLS

8.4 TRANSPORT

8.4.1 POLYETHER POLYOLS

8.4.2 POLYESTER POLYOLS

8.5 PACKAGING

8.5.1 POLYETHER POLYOLS

8.5.2 POLYESTER POLYOLS

8.6 CARPET BACKING

8.6.1 POLYETHER POLYOLS

8.6.2 POLYESTER POLYOLS

8.7 OTHERS

8.7.1 POLYETHER POLYOLS

8.7.2 POLYESTER POLYOLS

9 ASIA-PACIFIC POLYOLS MARKET, BY REGION

9.1 ASIA-PACIFIC

9.1.1 CHINA

9.1.2 JAPAN

9.1.3 SOUTH KOREA

9.1.4 INDIA

9.1.5 AUSTRALIA AND NEW ZEALAND

9.1.6 SINGAPORE

9.1.7 MALAYSIA

9.1.8 THAILAND

9.1.9 INDONESIA

9.1.10 PHILIPPINES

9.1.11 REST OF ASIA-PACIFIC

10 ASIA-PACIFIC POLYOLS MARKET, COMPANY LANDSCAPE

10.1 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

11 SWOT ANALYSIS

12 COMPANY PROFILINGS

12.1 SHELL PLC

12.1.1 COMPANY SNAPSHOT

12.1.2 REVENUE ANALYSIS

12.1.3 COMPANY SHARE ANALYSIS

12.1.4 PRODUCT PORTFOLIO

12.1.5 RECENT DEVELOPMENTS

12.2 COVESTRO AG

12.2.1 COMPANY SNAPSHOT

12.2.2 REVENUE ANALYSIS

12.2.3 COMPANY SHARE ANALYSIS

12.2.4 PRODUCT PORTFOLIO

12.2.5 RECENT DEVELOPMENTS

12.3 WANHUA

12.3.1 COMPANY SNAPSHOT

12.3.2 REVENUE ANALYSIS

12.3.3 COMPANY SHARE ANALYSIS

12.3.4 PRODUCT PORTFOLIO

12.3.5 RECENT DEVELOPMENTS

12.4 LANXESS

12.4.1 COMPANY SNAPSHOT

12.4.2 REVENUE ANALYSIS

12.4.3 COMPANY SHARE ANALYSIS

12.4.4 PRODUCT AND SOLUTION PORTFOLIO

12.4.5 RECENT DEVELOPMENTS

12.5 HUNTSMAN INTERNATIONAL LLC

12.5.1 COMPANY SNAPSHOT

12.5.2 REVENUE ANALYSIS

12.5.3 COMPANY SHARE ANALYSIS

12.5.4 PRODUCT PORTFOLIO

12.5.5 RECENT DEVELOPMENTS

12.6 ARKEMA

12.6.1 COMPANY SNAPSHOT

12.6.2 REVENUE ANALYSIS

12.6.3 PRODUCT PORTFOLIO

12.6.4 RECENT DEVELOPMENT

12.7 BASF SE

12.7.1 COMPANY SNAPSHOT

12.7.2 REVENUE ANALYSIS

12.7.3 PRODUCT PORTFOLIO

12.7.4 RECENT DEVELOPMENTS

12.8 BIESTERFELD AG

12.8.1 COMPANY SNAPSHOT

12.8.2 PRODUCT PORTFOLIO

12.8.3 RECENT DEVELOPMENTS

12.9 CARGILL, INCORPORATED.

12.9.1 COMPANY SNAPSHOT

12.9.2 PRODUCT AND SERVICE PORTFOLIO

12.9.3 RECENT DEVELOPMENT

12.1 COIM GROUP

12.10.1 COMPANY SNAPSHOT

12.10.2 PRODUCT PORTFOLIO

12.10.3 RECENT DEVELOPMENTS

12.11 DOW

12.11.1 COMPANY SNAPSHOT

12.11.2 REVENUE ANALYSIS

12.11.3 PRODUCT PORTFOLIO

12.11.4 RECENT DEVELOPMENTS

12.12 DIC CORPORATION

12.12.1 COMPANY SNAPSHOT

12.12.2 REVENUE ANALYSIS

12.12.3 PRODUCT PORTFOLIO

12.12.4 RECENT DEVELOPMENTS

12.13 EMERY OLEOCHEMICALS LLC

12.13.1 COMPANY SNAPSHOT

12.13.2 PRODUCT PORTFOLIO

12.13.3 RECENT DEVELOPMENTS

12.14 GULSHAN POLYOLS LTD.

12.14.1 COMPANY SNAPSHOT

12.14.2 REVENUE ANALYSIS

12.14.3 PRODUCT PORTFOLIO

12.14.4 RECENT DEVELOPMENT

12.15 MITSUBISHI CHEMICAL CORPORATION

12.15.1 COMPANY SNAPSHOT

12.15.2 REVENUE ANALYSIS

12.15.3 PRODUCT PORTFOLIO

12.15.4 RECENT DEVELOPMENTS

12.16 PERSTORP HOLDING AB (SUBSIDIARY OF PETRONAS CHEMICALS GROUP)

12.16.1 COMPANY SNAPSHOT

12.16.2 REVENUE ANALYSIS

12.16.3 PRODUCT PORTFOLIO

12.16.4 RECENT DEVELOPMENTS

12.17 REPSOL

12.17.1 COMPANY SNAPSHOT

12.17.2 REVENUE ANALYSIS

12.17.3 PRODUCT PORTFOLIO

12.17.4 RECENT DEVELOPMENTS

12.18 SHAKUN INDUSTRIES

12.18.1 COMPANY SNAPSHOT

12.18.2 PRODUCT PORTFOLIO

12.18.3 RECENT DEVELOPMENT

12.19 STEPAN COMPANY

12.19.1 COMPANY SNAPSHOT

12.19.2 REVENUE ANALYSIS

12.19.3 PRODUCT PORTFOLIO

12.19.4 RECENT DEVELOPMENTS

12.2 TOSOH CORPORATION

12.20.1 COMPANY SNAPSHOT

12.20.2 REVENUE ANALYSIS

12.20.3 PRODUCT PORTFOLIO

12.20.4 RECENT DEVELOPMENT

12.21 VERTELLUS

12.21.1 COMPANY SNAPSHOT

12.21.2 PRODUCT PORTFOLIO

12.21.3 RECENT DEVELOPMENT

13 QUESTIONNAIRE

14 RELATED REPORTS

List of Table

TABLE 1 ASIA-PACIFIC POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 2 ASIA-PACIFIC POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 3 ASIA-PACIFIC POLYETHER POLYOLS IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 4 ASIA-PACIFIC POLYETHER POLYOLS IN POLYOLS MARKET, BY REGION, 2021-2030 (MT)

TABLE 5 ASIA-PACIFIC POLYESTER POLYOLS IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 6 ASIA-PACIFIC POLYESTER POLYOLS IN POLYOLS MARKET, BY REGION, 2021-2030 (MT)

TABLE 7 ASIA-PACIFIC POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 8 ASIA-PACIFIC FLEXIBLE POLYURETHANE FOAM IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 9 ASIA-PACIFIC RIGID POLYURETHANE FOAM IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 10 ASIA-PACIFIC COATINGS IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 11 ASIA-PACIFIC ADHESIVES & SEALANTS IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 12 ASIA-PACIFIC ELASTOMERS IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 13 ASIA-PACIFIC OTHERS IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 14 ASIA-PACIFIC POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 15 ASIA-PACIFIC CONSTRUCTION IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 16 ASIA-PACIFIC CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 17 ASIA-PACIFIC FURNITURE IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 18 ASIA-PACIFIC FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 19 ASIA-PACIFIC TRANSPORT IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 20 ASIA-PACIFIC TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 21 ASIA-PACIFIC PACKAGING IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 22 ASIA-PACIFIC PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 23 ASIA-PACIFIC CARPET BACKING IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 24 ASIA-PACIFIC CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 25 ASIA-PACIFIC OTHERS IN POLYOLS MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 26 ASIA-PACIFIC OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 27 ASIA-PACIFIC POLYOLS MARKET, BY COUNTRY, 2021-2030 (USD MILLION)

TABLE 28 ASIA-PACIFIC POLYOLS MARKET, BY COUNTRY, 2021-2030 (MT)

TABLE 29 ASIA-PACIFIC POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 30 ASIA-PACIFIC POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 31 ASIA-PACIFIC POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 32 ASIA-PACIFIC POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 33 ASIA-PACIFIC CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 34 ASIA-PACIFIC FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 35 ASIA-PACIFIC TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 36 ASIA-PACIFIC PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 37 ASIA-PACIFIC CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 38 ASIA-PACIFIC OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 39 CHINA POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 40 CHINA POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 41 CHINA POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 42 CHINA POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 43 CHINA CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 44 CHINA FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 45 CHINA TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 46 CHINA PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 47 CHINA CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 48 CHINA OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 49 JAPAN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 50 JAPAN POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 51 JAPAN POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 52 JAPAN POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 53 JAPAN CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 54 JAPAN FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 55 JAPAN TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 56 JAPAN PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 57 JAPAN CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 58 JAPAN OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 59 SOUTH KOREA POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 60 SOUTH KOREA POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 61 SOUTH KOREA POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 62 SOUTH KOREA POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 63 SOUTH KOREA CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 64 SOUTH KOREA FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 65 SOUTH KOREA TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 66 SOUTH KOREA PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 67 SOUTH KOREA CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 68 SOUTH KOREA OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 69 INDIA POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 70 INDIA POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 71 INDIA POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 72 INDIA POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 73 INDIA CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 74 INDIA FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 75 INDIA TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 76 INDIA PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 77 INDIA CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 78 INDIA OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 79 AUSTRALIA AND NEW ZEALAND POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 80 AUSTRALIA AND NEW ZEALAND POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 81 AUSTRALIA AND NEW ZEALAND POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 82 AUSTRALIA AND NEW ZEALAND POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 83 AUSTRALIA AND NEW ZEALAND CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 84 AUSTRALIA AND NEW ZEALAND FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 85 AUSTRALIA AND NEW ZEALAND TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 86 AUSTRALIA AND NEW ZEALAND PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 87 AUSTRALIA AND NEW ZEALAND CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 88 AUSTRALIA AND NEW ZEALAND OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 89 SINGAPORE POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 90 SINGAPORE POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 91 SINGAPORE POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 92 SINGAPORE POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 93 SINGAPORE CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 94 SINGAPORE FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 95 SINGAPORE TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 96 SINGAPORE PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 97 SINGAPORE CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 98 SINGAPORE OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 99 MALAYSIA POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 100 MALAYSIA POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 101 MALAYSIA POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 102 MALAYSIA POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 103 MALAYSIA CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 104 MALAYSIA FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 105 MALAYSIA TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 106 MALAYSIA PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 107 MALAYSIA CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 108 MALAYSIA OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 109 THAILAND POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 110 THAILAND POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 111 THAILAND POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 112 THAILAND POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 113 THAILAND CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 114 THAILAND FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 115 THAILAND TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 116 THAILAND PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 117 THAILAND CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 118 THAILAND OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 119 INDONESIA POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 120 INDONESIA POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 121 INDONESIA POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 122 INDONESIA POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 123 INDONESIA CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 124 INDONESIA FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 125 INDONESIA TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 126 INDONESIA PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 127 INDONESIA CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 128 INDONESIA OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 129 PHILIPPINES POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 130 PHILIPPINES POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

TABLE 131 PHILIPPINES POLYOLS MARKET, BY APPLICATION, 2021-2030 (USD MILLION)

TABLE 132 PHILIPPINES POLYOLS MARKET, BY END USER, 2021-2030 (USD MILLION)

TABLE 133 PHILIPPINES CONSTRUCTION IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 134 PHILIPPINES FURNITURE IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 135 PHILIPPINES TRANSPORT IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 136 PHILIPPINES PACKAGING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 137 PHILIPPINES CARPET BACKING IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 138 PHILIPPINES OTHERS IN POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 139 REST OF ASIA-PACIFIC POLYOLS MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 140 REST OF ASIA-PACIFIC POLYOLS MARKET, BY TYPE, 2021-2030 (MT)

List of Figure

FIGURE 1 ASIA-PACIFIC POLYOLS MARKET: SEGMENTATION

FIGURE 2 ASIA-PACIFIC POLYOLS MARKET: DBMR TRIPOD DATA VALIDATION MODEL

FIGURE 3 ASIA-PACIFIC POLYOLS MARKET: DROC ANALYSIS

FIGURE 4 ASIA-PACIFIC POLYOLS MARKET: ASIA-PACIFIC VS REGIONAL MARKET ANALYSIS

FIGURE 5 ASIA-PACIFIC POLYOLS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 ASIA-PACIFIC POLYOLS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 ASIA-PACIFIC POLYOLS MARKET: DBMR MARKET POSITION GRID

FIGURE 8 ASIA-PACIFIC POLYOLS MARKET: VENDOR SHARE ANALYSIS

FIGURE 9 ASIA-PACIFIC POLYOLS MARKET: MULTIVARIATE MODELLING

FIGURE 10 ASIA-PACIFIC POLYOLS MARKET: TYPE CURVE

FIGURE 11 ASIA-PACIFIC POLYOLS MARKET: MARKET APPLICATION COVERAGE GRID

FIGURE 12 ASIA-PACIFIC POLYOLS MARKET: SEGMENTATION

FIGURE 13 INCREASING DEMAND IN THE CONSTRUCTION AND INFRASTRUCTURE SECTOR IS EXPECTED TO BE A KEY DRIVER FOR ASIA-PACIFIC POLYOLS MARKET GROWTH IN THE FORECAST PERIOD OF 2023 TO 2030

FIGURE 14 POLYETHER POLYOLS ARE EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE ASIA-PACIFIC POLYOLS MARKET FROM 2023 TO 2030

FIGURE 15 GRAPH 1: EXPORT DATA OF COUNTRIES ACROSS THE GLOBE (FROM JANUARY TO MAY 2023)

FIGURE 16 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE ASIA-PACIFIC POLYOLS MARKET

FIGURE 17 ASIA-PACIFIC POLYOLS MARKET: BY TYPE, 2022

FIGURE 18 ASIA-PACIFIC POLYOLS MARKET: BY APPLICATION, 2022

FIGURE 19 ASIA-PACIFIC POLYOLS MARKET: BY END USER, 2022

FIGURE 20 ASIA-PACIFIC POLYOLS MARKET: SNAPSHOT (2022)

FIGURE 21 ASIA-PACIFIC POLYOLS MARKET: BY COUNTRY (2022)

FIGURE 22 ASIA-PACIFIC POLYOLS MARKET: BY COUNTRY (2023 & 2030)

FIGURE 23 ASIA-PACIFIC POLYOLS MARKET: BY COUNTRY (2022 & 2030)

FIGURE 24 ASIA-PACIFIC POLYOLS MARKET: BY TYPE (2023-2030)

FIGURE 25 ASIA-PACIFIC POLYOLS MARKET: COMPANY SHARE 2022(%)

Asia Pacific Polyols Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Polyols Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Polyols Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.