Asia Pacific Optical Films Market

Market Size in USD Billion

USD

17.60 Billion

USD

32.58 Billion

2025

2033

USD

17.60 Billion

USD

32.58 Billion

2025

2033

| 2026 - 2033 | |

| USD 17.60 Billion | |

| USD 32.58 Billion | |

| % | |

|

Asia-Pacific Optical Films Market Size

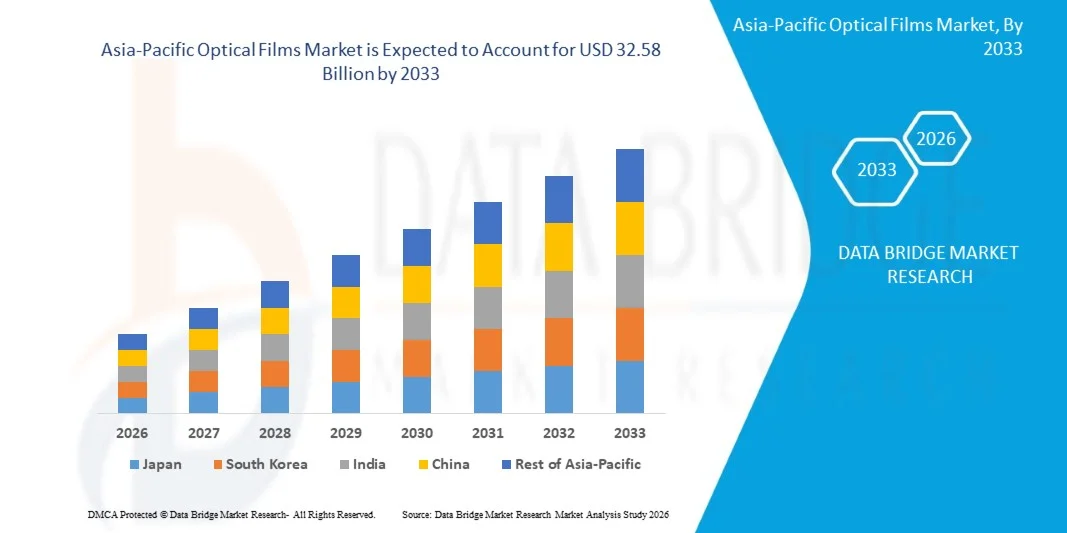

- The Asia-Pacific Optical Films Market size was valued at USD 17.60 billion in 2025 and is expected to reach USD 32.58 billion by 2033, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by the increasing demand for high-resolution display panels across consumer electronics such as smartphones, televisions, laptops, and tablets, driving the need for advanced optical films that enhance brightness, contrast, and energy efficiency

- Furthermore, rising adoption of OLED and LCD technologies along with growing investments in advanced display manufacturing is establishing optical films as essential components for improving visual performance and reducing power consumption. These converging factors are accelerating the integration of optical films across multiple applications, thereby significantly boosting the industry's growth

Asia-Pacific Optical Films Market Analysis

- Optical films are specialized thin-layer materials used in display systems to control light transmission, reflection, diffusion, and polarization, enhancing overall display quality and performance in electronic devices and digital signage applications

- The escalating demand for optical films is primarily fueled by rapid advancements in display technologies, increasing consumer preference for high-quality visual experiences, and growing deployment of displays across sectors such as consumer electronics, automotive, and advertising

- China dominated the Asia-Pacific Optical Films Market in 2025, due to its extensive electronics manufacturing base, strong presence of display panel production facilities, and rising demand for consumer electronics such as smartphones, televisions, and digital signage

- India is expected to be the fastest growing country in the Asia-Pacific Optical Films Market during the forecast period due to increasing adoption of consumer electronics, rising smartphone penetration, and growing investments in electronics manufacturing

- Polarizer and sub-films segment dominated the market with a market share of 39% in 2025, due to their critical role in controlling light transmission and enhancing display clarity in LCD and OLED panels. These films are essential components in televisions, smartphones, and monitors, ensuring improved contrast, brightness, and color accuracy. Increasing demand for high-resolution displays and advancements in display technologies have significantly strengthened their adoption

Report Scope and Asia-Pacific Optical Films Market Segmentation

|

Attributes |

Optical Films Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Optical Films Market Trends

“Rising Adoption of Advanced Display Technologies”

- A significant trend in the Asia-Pacific Optical Films Market is the increasing adoption of advanced display technologies such as OLED, AMOLED, and high-resolution LCD panels, driven by growing consumer demand for superior visual experiences across electronic devices. This trend is strengthening the role of optical films as critical components that enhance brightness, contrast, and energy efficiency in modern displays

- For instance, Samsung Electronics and LG Display are actively expanding OLED and next-generation display production, which heavily relies on high-performance optical films to improve image quality and panel efficiency

- The increasing penetration of ultra-high-definition televisions and premium smartphones is driving the integration of advanced optical films that support enhanced color accuracy and viewing angles. This is reinforcing their importance in delivering immersive viewing experiences across consumer electronics

- The demand for thinner and lightweight display panels is encouraging the development of innovative optical films that enable compact designs without compromising performance. This is supporting the evolution of sleek and portable electronic devices

- Industries such as automotive and digital signage are rapidly adopting advanced display systems that require durable and high-efficiency optical films for consistent performance. This is expanding the application scope of optical films beyond traditional consumer electronics

- The continuous innovation in display technologies and increasing investments in next-generation panels are reinforcing the long-term growth of optical films. This trend is positioning optical films as indispensable materials in the advancement of modern display ecosystems across global markets

Asia-Pacific Optical Films Market Dynamics

Driver

“Increasing Demand for High-Resolution and Energy-Efficient Displays”

- The increasing demand for high-resolution and energy-efficient displays is a key driver for the Asia-Pacific Optical Films Market, as consumers and industries seek enhanced visual clarity while minimizing power consumption. Optical films play a vital role in optimizing light management, thereby improving display efficiency and reducing energy usage in electronic devices

- For instance, 3M supplies brightness enhancement and reflective films that are widely used in televisions and monitors to improve luminance while lowering energy consumption, supporting manufacturers in achieving performance and sustainability goals

- The rapid growth of smartphones, tablets, and laptops is accelerating the need for optical films that can support high pixel density and improved screen performance. This is increasing their integration across a wide range of consumer electronics

- The expansion of large-format displays in commercial and advertising sectors is further driving demand for optical films that ensure uniform brightness and durability. These applications require efficient light control to maintain visibility across various environments

- The rising preference for high-quality and energy-efficient displays continues to strengthen this driver. The need for improved performance, reduced energy usage, and enhanced user experience is significantly influencing the growth trajectory of the Asia-Pacific Optical Films Market

Restraint/Challenge

“High Production Costs and Raw Material Price Volatility”

- The Asia-Pacific Optical Films Market faces challenges due to high production costs and volatility in raw material prices, as manufacturing these films requires advanced materials and precision processing technologies. These factors increase overall production expenses and impact profit margins for manufacturers

- For instance, Toray Industries utilizes specialized materials such as polyethylene terephthalate and polyvinyl alcohol in optical films, where fluctuations in raw material prices directly influence manufacturing costs and supply chain stability

- The complexity of production processes, including coating, stretching, and lamination, requires sophisticated equipment and skilled labor, further elevating operational costs. This makes large-scale production more challenging for manufacturers

- Dependence on high-quality raw materials and limited suppliers increases vulnerability to supply disruptions and price fluctuations. This creates uncertainty in cost management and production planning

- The ongoing challenges related to cost optimization and raw material sourcing continue to restrain market growth. Manufacturers are under pressure to balance performance, pricing, and supply stability while meeting the increasing demand for advanced optical films

Asia-Pacific Optical Films Market Scope

The market is segmented on the basis of product type, function, and application.

• By Product Type

On the basis of product type, the Asia-Pacific Optical Films Market is segmented into polarizer and sub-films, polyvinyl alcohol (PVA) film, polyvinyl alcohol (PVA) protection film, compensation film, surface treatment film, polyethylene terephthalate (PET) protection film/release film, backlight optical films, diffuser film, reflector film, and light guide plate (LGP). The polarizer and sub-films segment dominated the largest market revenue share of 39% in 2025, driven by their critical role in controlling light transmission and enhancing display clarity in LCD and OLED panels. These films are essential components in televisions, smartphones, and monitors, ensuring improved contrast, brightness, and color accuracy. Increasing demand for high-resolution displays and advancements in display technologies have significantly strengthened their adoption. The widespread integration of polarizer films across consumer electronics continues to reinforce their leading position in the market.

The backlight optical films segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising demand for energy-efficient and high-brightness displays. These films enhance light uniformity and optimize brightness in display panels, making them highly suitable for large-screen TVs and commercial displays. Growing adoption of advanced display systems in automotive dashboards and digital signage further accelerates demand. Continuous innovation in light management technologies and increasing preference for thinner, more efficient displays are supporting the rapid expansion of this segment.

• By Function

On the basis of function, the Asia-Pacific Optical Films Market is segmented into display surface films, brightness enhancement films (BEF), reflective polarizer films (DBEF), backlight reflector films (ESR), and light control/privacy films (ACLF). The brightness enhancement films (BEF) segment held the largest market revenue share in 2025, driven by their ability to significantly improve display luminance without increasing power consumption. These films are widely used in televisions, laptops, and mobile devices to deliver brighter visuals while maintaining energy efficiency. Rising consumer preference for vivid and high-quality display output has increased their integration across multiple devices. The growing focus on reducing power usage in electronic devices further strengthens the demand for BEF solutions.

The light control/privacy films (ACLF) segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing concerns regarding data security and visual privacy in public and professional environments. These films restrict viewing angles, making them highly suitable for laptops, ATMs, and corporate displays. The growing use of digital devices in shared spaces and workplaces is accelerating their adoption. Advancements in privacy technologies and increasing awareness about information security are contributing to the strong growth trajectory of this segment.

• By Application

On the basis of application, the Asia-Pacific Optical Films Market is segmented into TV, laptops, tablets, smartphones, billboards, smart electronic wearable, control panel displays and signage, and advertising display boards. The smartphone segment dominated the largest market revenue share in 2025, driven by the massive global adoption of smartphones and continuous advancements in display technologies such as OLED and AMOLED. Optical films play a crucial role in enhancing screen brightness, durability, and visual clarity, making them indispensable in modern smartphones. Increasing consumer demand for high-resolution and immersive display experiences continues to drive segment growth. Rapid product innovation and frequent device upgrades further reinforce the dominance of this segment.

The smart electronic wearable segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising adoption of smartwatches, fitness trackers, and AR-based wearable devices. These devices require compact, lightweight, and high-performance optical films to deliver clear and energy-efficient displays. Growing health awareness and increasing integration of wearable technology into daily life are boosting demand. Continuous innovation in flexible and miniaturized display technologies is further accelerating the expansion of this segment.

Asia-Pacific Optical Films Market Regional Analysis

- China dominated the Asia-Pacific Optical Films Market with the largest revenue share in 2025, driven by its extensive electronics manufacturing base, strong presence of display panel production facilities, and rising demand for consumer electronics such as smartphones, televisions, and digital signage

- Robust government support for domestic semiconductor and display industries, combined with increasing investments in OLED and LCD production and rapid industrialization, reinforce China’s leadership in the regional market

- The presence of leading manufacturers, collaborations with global electronics companies such as BOE Technology Group and TCL Technology, and continuous advancements in display technologies continue to consolidate China’s dominant position during the forecast period. Expanding exports and strong domestic consumption of electronic devices further strengthen market penetration across urban and industrial sectors

Japan Asia-Pacific Optical Films Market Insight

The Japan market is anticipated to grow steadily from 2026 to 2033, supported by its advanced material science capabilities and strong presence of leading optical film manufacturers. Japanese companies are increasingly focusing on high-performance and energy-efficient optical films to support next-generation display technologies. The demand for precision-engineered films used in premium electronics and automotive displays is rising due to the country’s emphasis on quality and innovation. Continuous research and development investments and collaborations between companies such as Toray Industries and Nitto Denko Corporation reinforce the market’s steady growth outlook. Japan’s focus on advanced materials, reliability, and technological leadership underpins its strong regional positioning.

India Asia-Pacific Optical Films Market Insight

India is projected to register the fastest CAGR in the Asia-Pacific Optical Films Market during 2026–2033, fueled by increasing adoption of consumer electronics, rising smartphone penetration, and growing investments in electronics manufacturing. Expanding middle-class population, urbanization, and government initiatives supporting domestic production are accelerating market growth. The demand for cost-effective and high-performance display components is particularly strong across mobile devices and televisions. Expanding retail networks, rapid growth of e-commerce, and collaborations with companies such as Samsung Electronics and LG Electronics are enhancing product availability. Increasing focus on digitalization and domestic manufacturing ensures India’s emergence as the fastest-growing market in the region.

Asia-Pacific Optical Films Market Share

The optical films industry is primarily led by well-established companies, including:

- LG Chem. (South Korea)

- Hyosung Chemical Co., Ltd. (South Korea)

- Toray Industries, Inc. (Japan)

- Sumitomo Chemical Co., Ltd. (Japan)

- Zeon Corporation (Japan)

- 3M Company (U.S.)

- UFO Display Solutions (U.S.)

- Mitsubishi Polyester Film, Inc. (U.S.)

- Nitto Denko Corporation (Japan)

- Samsung SDI Co., Ltd. (South Korea)

- Kolon Industries, Inc. (South Korea)

- Sanritz Automation Co., Ltd. (Japan)

- Dexerials Corporation (Japan)

- Teijin Limited (Japan)

Latest Developments in Asia-Pacific Optical Films Market

- In 2025, Zeon Corporation focused on the development of high-performance optical films with enhanced uniformity and extended operational life, targeting professional displays and commercial digital signage applications. This advancement improves consistency in brightness and color reproduction across large screens, which is critical for commercial environments requiring continuous operation. The longer lifespan of these films reduces maintenance and replacement costs for end users, increasing their attractiveness in large-scale deployments. As demand rises for reliable display infrastructure in advertising and information systems, this development is strengthening Zeon Corporation’s positioning in premium and commercial optical films segments

- In 2024, Toray Industries introduced thinner and lightweight optical films with improved light diffusion properties, aimed at enabling slimmer display designs and more energy-efficient backlight systems. These films support the trend toward ultra-thin consumer electronics by reducing overall panel thickness without compromising display quality. Improved diffusion enhances uniform brightness, which is essential for high-end televisions and portable devices. The energy efficiency benefits align with growing regulatory and consumer focus on low-power electronics, thereby expanding adoption across multiple device categories and reinforcing Toray Industries’ competitive edge in advanced materials

- In 2024, Samsung SDI strengthened its optical film solutions by focusing on improved durability and thermal stability, particularly for advanced monitors and large-format displays. These enhancements enable the films to withstand prolonged usage and higher operating temperatures, which are common in professional and industrial environments. Increased durability reduces performance degradation over time, ensuring consistent display output and reliability. This development supports the rising demand for high-performance display systems in sectors such as control rooms and digital signage, thereby enhancing Samsung SDI’s presence in high-value optical film applications

- In 2023, Sumitomo Chemical advanced next-generation optical film materials designed for high-resolution and high-refresh-rate displays used in premium consumer electronics and industrial visualization systems. These materials enable smoother motion rendering and sharper image quality, which are essential for gaming, professional design, and simulation applications. The ability to support higher refresh rates improves user experience and aligns with evolving display standards. This innovation is driving adoption in premium device segments and strengthening Sumitomo Chemical’s role in supplying cutting-edge materials for next-generation display technologies

- In 2023, LG Chem expanded the development of high-efficiency polarizing films optimized for large-size televisions and professional monitors, with a focus on improved brightness retention and reduced light leakage. These improvements enhance visual clarity and energy efficiency, particularly in large display formats where light management is critical. Reduced light leakage contributes to better contrast ratios and viewing experiences, which are key factors in consumer purchasing decisions. This development supports the increasing demand for high-quality large-screen displays and reinforces LG Chem’s leadership in polarizer film technology within the Asia-Pacific Optical Films Market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Optical Films Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Optical Films Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Optical Films Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.