Global Packaging Materials Market

Tamanho do mercado em biliões de dólares

CAGR :

%

USD

837.37 Billion

USD

1,096.78 Billion

2024

2032

USD

837.37 Billion

USD

1,096.78 Billion

2024

2032

| 2025 –2032 | |

| USD 837.37 Billion | |

| USD 1,096.78 Billion | |

| % | |

|

Global Packaging Materials Market, By Material Type (Plastic, Paper & Cardboard, Metal, Glass, Wood, Textile, and Others), Product (Corrugated Boxes, Bottles & Cans, Containers & Jars, Bags, Pouches & Wraps, Films, Boxes & Crates, Flexible Pouches, Blister Packaging, Clamshells, Shrink Film Tubing, Closures & Lids, Strapping, Polybags, Drums & IBC, Roll Bags, Carded Packaging, Shrink Bands, and Others), Material Form (Flexible and Rigid), Packaging Type (Primary Packaging, Secondary Packaging, and Tertiary Packaging), End-Use (Food & Beverage, Personal Care & Cosmetics, Medical, Electrical & Electronics, Homecare, Chemicals, Industrial Packaging, Agriculture, and Others) - Industry Trends and Forecast to 2031.

Packaging Materials Market Analysis and Size

The increasing demand for packaged food and beverages, driven by changing lifestyles and a growing population, significantly contributes to the rise in the utilization of packaging material such as plastic, paper, and cardboard is driving the market growth.

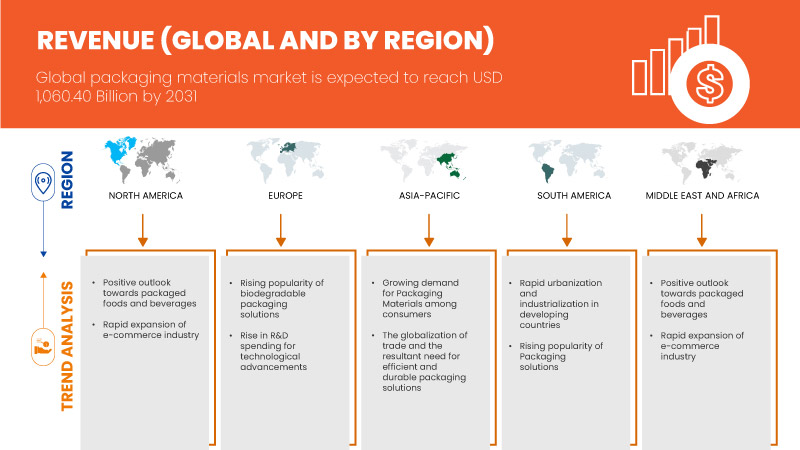

Data Bridge Market Research analyzes that the global packaging materials market is expected to reach USD 1,060.40 billion by 2031 from USD 814.46 billion in 2023, growing with a CAGR of 3.43% in the forecast period from 2024 to 2031.

The global packaging materials market report provides details of market share, new developments, and the impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, products approvals, strategic decisions, product launches, geographic expansions, and technological innovations in the market. To understand the analysis and the market scenario, contact us for an analyst brief. Our team will help you create a revenue-impact solution to achieve your desired goal.

|

Report Metric |

Details |

|

Forecast Period |

2024-2031 |

|

Base Year |

2023 |

|

Historic Years |

2022 (Customizable to 2016-2021) |

|

Quantitative Units |

Revenue in USD Billion, Volume in Kilo Tons |

|

Segments Covered |

Material Type (Plastic, Paper & Cardboard, Metal, Glass, Wood, Textile, and Others.), Product (Corrugated Boxes, Bottles & Cans, Containers & Jars, Bags, Pouches & Wraps, Films, Boxes & Crates, Flexible Pouches, Blister Packaging, Clamshells, Shrink Film Tubing, Closures & Lids, Strapping, Polybags, Drums & IBC, Roll Bags, Carded Packaging, Shrink Bands, and Others), Material Form (Flexible and Rigid), Packaging Type (Primary Packaging, Secondary Packaging, and Tertiary Packaging), End-Use (Food & Beverage, Personal Care & Cosmetics, Medical, Electrical & Electronics, Homecare, Chemicals, Industrial Packaging, Agriculture, and Others) |

|

Countries Covered |

U.S., Canada, Mexico, Germany, France, U.K., Italy, Russia, Spain, Sweden, Finland, Netherlands, Switzerland, Poland, Belgium, Turkey, Norway, Denmark, Rest of Europe, China, Japan, India, South Korea, Indonesia, Thailand, Malaysia, Philippines, Singapore, Australia, New Zealand, Rest of Asia-Pacific, Brazil, Argentina, Rest of South America, Saudi Arabia, South Africa, U.A.E., Egypt, Israel, Rest of Middle East and Africa |

|

Market Players Covered |

Exxon Mobil Corporation, Amcor plc, Novelis, INEOS, Dow, Smurfit Kappa, Stora Enso, SABIC, International Paper, WestRock Company, DS Smith, Braskem, Tata Steel, NIPPON STEEL CORPORATION, LyondellBasell Industries Holdings B.V., ArcelorMittal, UPM, Chevron Phillips Chemical Company LLC, Oji Holdings Corporation, Mondi, Sappi, NIPPON PAPER INDUSTRIES CO., LTD., Domtar Corporation, Formosa Plastics Corporation, U.S.A., and ProAmpac among others |

Market Definition

Packaging materials are materials used to enclose, protect, and present products for storage, distribution, sale, and use. They serve a crucial role in various industries, including food and beverages, pharmaceuticals, cosmetics, electronics, and more. Packaging materials come in a wide range of types, each with its own characteristics and suitability for different applications.

Global Packaging Materials Market Dynamic

This section deals with understanding the market drivers, advantages, opportunities, restraints, and challenges. All of this is discussed in detail below:

Drivers

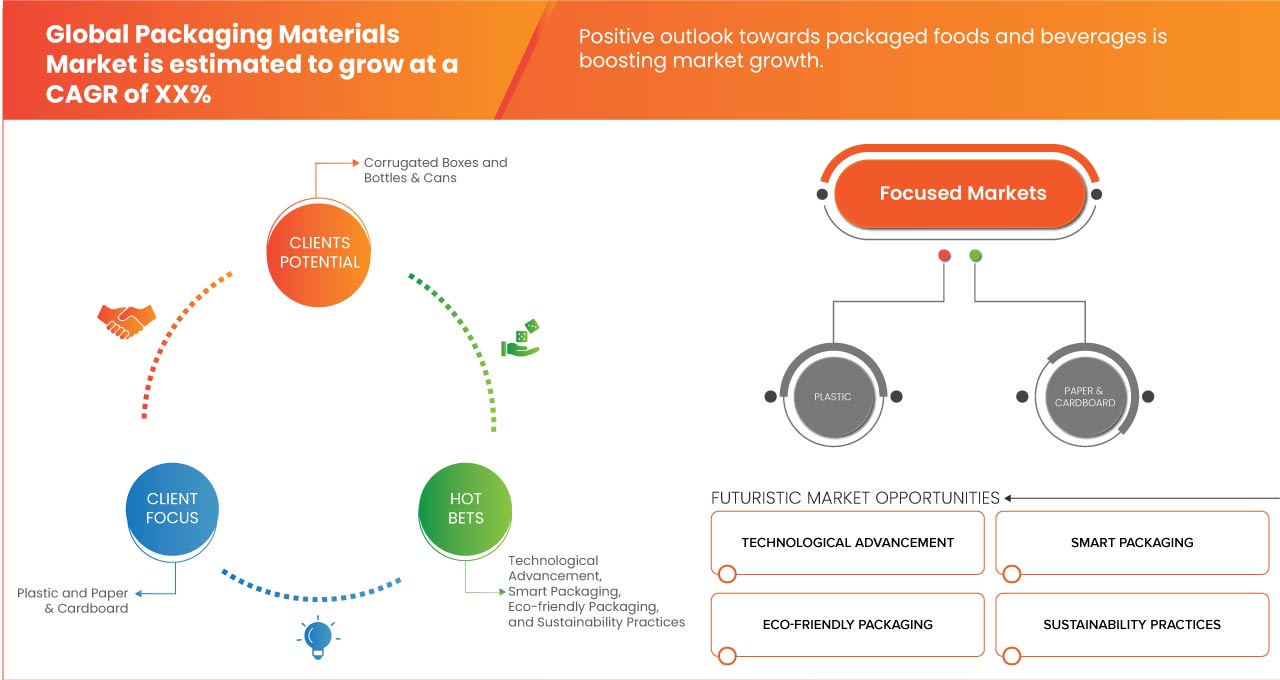

- Positive Outlook Towards Packaged Foods and Beverages

The increasing demand for packaged food and beverages, driven by changing lifestyles and a growing population, significantly contributes to the rise in the utilization of packaging materials such as plastic, paper, and cardboard. This trend is propelled by several interconnected factors. Firstly, as urbanization accelerates and consumers adopt busier lifestyles, there is a greater inclination towards convenience-oriented food and beverage options. Packaged products offer convenience in terms of storage, transportation, and consumption, aligning with the fast-paced routines of modern life.

In conclusion, the escalating demand for packaged food and beverages, spurred by evolving lifestyles and a burgeoning global population, underscores the critical importance of packaging materials in meeting consumer needs and industry demands. As urbanization progresses and consumer preferences shift towards convenience and variety, packaging materials such as plastic, paper, and cardboard play indispensable roles in preserving product freshness, ensuring safety, and enhancing shelf appeal. Moreover, with sustainability becoming a growing concern, the need for eco-friendly packaging solutions is more pronounced than ever, driving innovation and investment in recyclable and biodegradable materials.

- Rapid Expansion of E-Commerce Industry

The rapid expansion of the e-commerce industry has catalyzed a significant surge in the demand for packaging products and solutions, reshaping the landscape of the packaging industry in profound ways. This transformation is driven by several interrelated factors, such as the proliferation of online shopping platforms has led to an exponential increase in the volume of goods being shipped and delivered directly to consumers' doorsteps. With consumers embracing the convenience and accessibility of online shopping, there is a heightened need for robust and efficient packaging solutions that can withstand the rigors of transportation while safeguarding products against damage and tampering.

In conclusion, the rapid expansion of the e-commerce industry has become a driving force behind the growing demand for packaging materials, fueling innovation, sustainability, and efficiency across the packaging supply chain. As e-commerce continues to reshape the retail landscape, packaging material manufacturers and suppliers must remain agile and responsive to the evolving demands of this dynamic and rapidly growing market.

Opportunity

- Development of Smart Packaging

Smart packaging refers to the incorporation of sensors, indicators, and other intelligent features into packaging materials to provide additional functionality beyond traditional containment and protection. These features can include temperature monitoring, freshness indicators, tamper-evident seals, QR codes for tracking and traceability, and interactive elements for consumer engagement. By integrating smart technology with packaging materials, manufacturers and retailers can enhance product safety, improve supply chain visibility, reduce waste through better inventory management, and enhance consumer engagement and satisfaction. This convergence of traditional packaging materials with smart technology not only adds value to the packaging itself but also opens up new revenue streams and business opportunities for packaging material suppliers. Moreover, as the demand for smart packaging solutions continues to grow across various industries such as food and beverage, pharmaceuticals, and consumer goods, the global packaging materials market stands to benefit significantly from the increasing adoption of these innovative and high-value-added packaging solutions.

- Rise in R&D Spending for Technological Advancements

As companies allocate more resources to R&D, they can explore and develop innovative packaging solutions that offer enhanced functionality, efficiency, and sustainability. This heightened focus on R&D enables the creation of packaging materials with improved barrier properties, extended shelf life, and reduced environmental impact. For example, advancements in materials science can lead to the development of bio-based or compostable packaging materials, addressing growing concerns about plastic pollution and environmental sustainability. Additionally, investments in R&D facilitate the integration of advanced manufacturing technologies, such as nanotechnology and 3D printing, into packaging production processes, enabling the customization and optimization of packaging designs. These technological advancements not only meet evolving consumer preferences and regulatory requirements but also offer competitive advantages to companies in terms of product differentiation and market positioning. Moreover, innovative packaging solutions can drive cost savings through improved efficiency in storage, transportation, and distribution, further enhancing the value proposition for businesses across various industries. Therefore, the rise in R&D spending presents a compelling opportunity for stakeholders in the global packaging materials market to innovate and differentiate their offerings, driving growth and competitiveness in the industry.

Restraints/Challenges

- Fluctuation in Raw Material Prices

Packaging materials, including plastics, paper, cardboard, metals, and glass, rely heavily on raw materials sourced from natural resources such as petroleum, wood pulp, minerals, and metals. Any volatility or instability in the prices of these raw materials can have far-reaching effects on the packaging industry.

Fluctuations in raw material prices directly influence the manufacturing costs of packaging materials. When the prices of raw materials increase, it leads to higher production costs for packaging manufacturers. These increased costs may be passed on to consumers through higher prices for packaged goods or absorbed by manufacturers, affecting their profit margins and overall competitiveness in the market. Conversely, if raw material prices decrease, packaging manufacturers may experience margin improvements, but this could also lead to increased demand and strain on raw material supplies.

Moreover, the uncertainty surrounding raw material prices complicates long-term planning and investment decisions for packaging manufacturers. Volatile prices make it challenging to forecast production costs accurately, leading to potential budget constraints and resource allocation issues. This uncertainty may also deter investments in research and development initiatives aimed at innovation and sustainability in packaging materials.

- Increasing Consumer Resistance to Excessive Packaging Waste

Consumer resistance to excessive packaging waste has been growing due to increasing awareness of environmental issues and the desire to reduce the ecological footprint. The global packaging materials market is experiencing a notable shift as increasing consumer resistance to excessive packaging waste poses a significant restraint. This growing consumer awareness and demand for sustainable practices are reshaping market dynamics, compelling manufacturers and businesses to adapt to evolving preferences and regulatory landscapes

In addition, regulatory pressures, such as bans on single-use plastics and Extended Producer Responsibility (EPR) policies, are compelling manufacturers to shift towards eco-friendly materials. As a result, there is a notable decline in demand for traditional packaging, while the market for biodegradable, compostable, and recyclable options is growing. Therefore, companies are investing in innovative packaging designs and enhancing recycling infrastructure to meet these new demands.

Plastic is an important material for the global economy. At the same time, increasing plastic consumption is accompanied by serious environmental problems. Currently, the existing waste and recycling infrastructure cannot keep up with the growing volume of end-of-life plastic. An increasing amount of disposable packaging is one of the main causes of the waste problem, as plastic is especially used in consumer products. This includes, in particular, single-use plastic packaging, bags and bottles, all of which are most commonly found in global waste streams. Single-use plastic packaging has a short lifespan and it is then, typically, discarded carelessly by consumers.

Recent Developments

- In April 2024, International Paper Company and DS Smith are pleased to announce an all-share combination agreement. This merger combines complementary businesses, creating a global leader in sustainable packaging with strong positions in Europe and North America. The focus on sustainable solutions will serve a wide range of growing markets

- In March 2024, Amcor, a global leader in developing and producing responsible packaging solutions, is the proud recipient of eight Flexible Packaging Achievement Awards for innovative and sustainable contributions to the industry. The awards were presented at a ceremony last night during the 2024 Flexible Packaging Association (FPA) annual meeting in Tucson, Arizona

- In August 2022, LyondellBasell Industries Holdings B.V. partnered with Röchling Medical, a leading producer of secure medication packaging, to advance the circular economy. Together, they have introduced eye drop containers crafted by Röchling Medical using LyondellBasell's CirculenRenew polymers

- In May 2024, Chevron Phillips Chemical was honored with the Quality Award for customer loyalty and satisfaction in a national survey of polyethylene customers, competing against 10 major plastics companies. Additionally, Mastio & Company ranked CPChem as the top HDPE Supplier Overall based on interviews with 176 customers. This acknowledgment underscores CPChem's commitment to excellence in providing High-Density Polyethylene (HDPE), a versatile polymer used in various durable products and packaging solutions

- In March 2024, Shell Chemicals and Braskem have introduced certified bio-attributed and bio-circular propylene and polypropylene to the U.S. market. This development supports the growing consumer demand for more sustainable plastics. Braskem will utilize these feedstocks to produce bio-attributed and bio-circular polypropylene, offering more sustainable options for the packaging, film, automotive, and consumer goods markets

Global Packaging Materials Market Scope

The global packaging materials market is segmented into five notable segments based on material type, product, material form, packaging type, and end-use. The growth amongst these segments will help you analyze major growth segments in the industries and provide the users with a valuable market overview and market insights to make strategic decisions to identify core market applications.

Material Type

- Plastic

- Paper & Cardboard

- Metal

- Glass

- Textile

- Others

On the basis of material type, the market is segmented into plastic, paper & cardboard, metal, glass, wood, textile, and others.

Product

- Corrugated Boxes

- Bottles & Cans

- Containers & Jars

- Bags, Pouches & Wraps

- Films

- Boxes & Crates

- Flexible Pouches

- Blister Packaging

- Clamshells

- Shrink Film Tubing

- Closures & Lids

- Strapping

- Polybags

- Drums & IBC

- Roll Bags

- Carded Packaging

- Shrink Bands

- Others

On the basis of product, the market is segmented into corrugated boxes, bottles & cans, containers & jars, bags, pouches & wraps; films, boxes & crates, flexible pouches, blister packaging, clamshells, shrink film tubing, closures & lids, strapping, polybags, drums & IBC, roll bags, carded packaging, shrink bands, and others.

Material Form

- Flexible

- Rigid

On the basis of material form, the market is segmented into flexible and rigid.

Packaging Type

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

On the basis of packaging type, the market is segmented into primary packaging, secondary packaging, and tertiary packaging.

End-Use

- Food & Beverage

- Personal Care & Cosmetics

- Medical

- Electrical & Electronics

- Homecare

- Chemicals

- Industrial Packaging

- Agriculture

- Others

On the basis of end-use, the market is segmented into food & beverage, personal care & cosmetics, medical, electrical & electronics, homecare, chemicals, industrial packaging, agriculture, and others.

Global Packaging Materials Market Regional Analysis/Insights

The global packaging materials market is segmented into five notable segments based on material type, product, material form, packaging type, and end-use.

The countries in the global packaging materials market are U.S., Canada, Mexico, Germany, France, U.K., Italy, Russia, Spain, Sweden, Finland, Netherlands, Switzerland, Poland, Belgium, Turkey, Norway, Denmark, rest of Europe, China, Japan, India, South Korea, Indonesia, Thailand, Malaysia, Philippines, Singapore, Australia, New Zealand, rest of Asia-Pacific, Brazil, Argentina, rest of South America, Saudi Arabia, South Africa, U.A.E., Egypt, Israel, and rest of Middle East and Africa.

Asia-Pacific segment is expected to dominate the market due to rapid expansion of e-commerce industry in the region. China is expected to Asia-Pacific packaging materials market due to rapid urbanization and industrialization in the country. U.S. is expected to dominate the North America packaging materials market due to rise in R&D spending for technological advancements. Germany is expected to dominate the Europe packaging materials market due to development of smart packaging in the country.

The country section of the report also provides individual market-impacting factors and changes in market regulation that impact the current and future trends of the market. Data point downstream and upstream value chain analysis, technical trends porter's five forces analysis, and case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, the impact of domestic tariffs, and trade routes are considered while providing forecast analysis of the country data.

Competitive Landscape and Global Packaging Materials Market Share Analysis

The global packaging materials market competitive landscape provides details by competitors. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product trials pipelines, product approvals, patents, product width and breadth, application dominance, technology lifeline curve. The above data points provided are only related to the companies’ focus related to the global packaging materials market.

Some of the prominent participants operating in the global packaging materials market are Exxon Mobil Corporation, Amcor plc, Novelis, INEOS, Dow, Smurfit Kappa, Stora Enso, SABIC, International Paper, WestRock Company, DS Smith, Braskem, Tata Steel, NIPPON STEEL CORPORATION, LyondellBasell Industries Holdings B.V., ArcelorMittal, UPM, Chevron Phillips Chemical Company LLC, Oji Holdings Corporation, Mondi, Sappi, NIPPON PAPER INDUSTRIES CO., LTD., Domtar Corporation, Formosa Plastics Corporation, U.S.A., and ProAmpac among others.

SKU-

Obtenha acesso online ao relatório sobre a primeira nuvem de inteligência de mercado do mundo

- Painel interativo de análise de dados

- Painel de análise da empresa para oportunidades de elevado potencial de crescimento

- Acesso de analista de pesquisa para personalização e customização. consultas

- Análise da concorrência com painel interativo

- Últimas notícias, atualizações e atualizações Análise de tendências

- Aproveite o poder da análise de benchmark para um rastreio abrangente da concorrência

Metodologia de Investigação

A recolha de dados e a análise do ano base são feitas através de módulos de recolha de dados com amostras grandes. A etapa inclui a obtenção de informações de mercado ou dados relacionados através de diversas fontes e estratégias. Inclui examinar e planear antecipadamente todos os dados adquiridos no passado. Da mesma forma, envolve o exame de inconsistências de informação observadas em diferentes fontes de informação. Os dados de mercado são analisados e estimados utilizando modelos estatísticos e coerentes de mercado. Além disso, a análise da quota de mercado e a análise das principais tendências são os principais fatores de sucesso no relatório de mercado. Para saber mais, solicite uma chamada de analista ou abra a sua consulta.

A principal metodologia de investigação utilizada pela equipa de investigação do DBMR é a triangulação de dados que envolve a mineração de dados, a análise do impacto das variáveis de dados no mercado e a validação primária (especialista do setor). Os modelos de dados incluem grelha de posicionamento de fornecedores, análise da linha de tempo do mercado, visão geral e guia de mercado, grelha de posicionamento da empresa, análise de patentes, análise de preços, análise da quota de mercado da empresa, normas de medição, análise global versus regional e de participação dos fornecedores. Para saber mais sobre a metodologia de investigação, faça uma consulta para falar com os nossos especialistas do setor.

Personalização disponível

A Data Bridge Market Research é líder em investigação formativa avançada. Orgulhamo-nos de servir os nossos clientes novos e existentes com dados e análises que correspondem e atendem aos seus objetivos. O relatório pode ser personalizado para incluir análise de tendências de preços de marcas-alvo, compreensão do mercado para países adicionais (solicite a lista de países), dados de resultados de ensaios clínicos, revisão de literatura, mercado remodelado e análise de base de produtos . A análise de mercado dos concorrentes-alvo pode ser analisada desde análises baseadas em tecnologia até estratégias de carteira de mercado. Podemos adicionar quantos concorrentes necessitar de dados no formato e estilo de dados que procura. A nossa equipa de analistas também pode fornecer dados em tabelas dinâmicas de ficheiros Excel em bruto (livro de factos) ou pode ajudá-lo a criar apresentações a partir dos conjuntos de dados disponíveis no relatório.