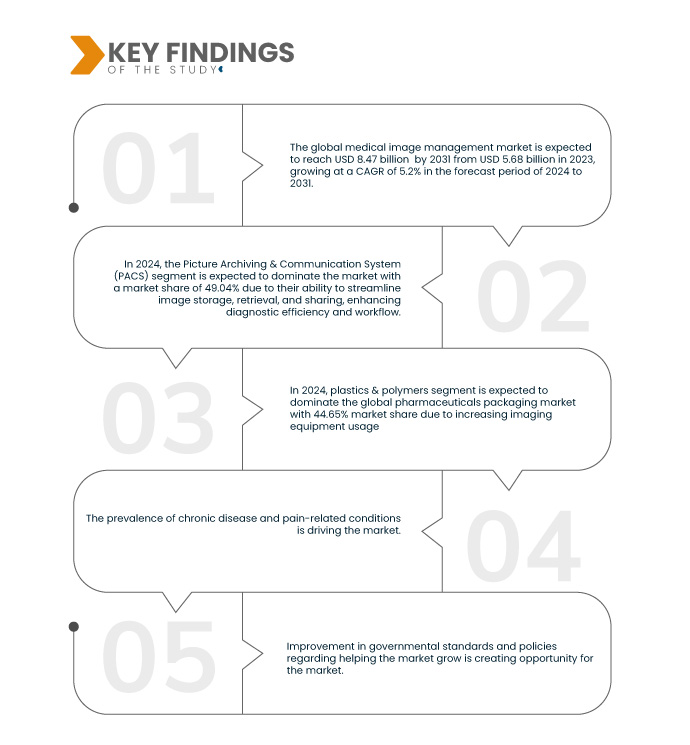

Der steigende Bedarf an Früherkennung von Krankheiten treibt den Markt für medizinisches Bildmanagement erheblich voran, da fortschrittliche Bildgebungstechnologien und effiziente Datenmanagementsysteme erforderlich sind. Mit dem wachsenden Bewusstsein für die Vorteile einer frühzeitigen Krankheitserkennung steigt der Bedarf an einem effizienten Management medizinischer Bilder. Gesundheitsdienstleister setzen daher zunehmend auf hochentwickelte Bildgebungsverfahren wie MRT, CT und Ultraschall . Dies umfasst die Speicherung, Abfrage und Analyse von Scans, Röntgenaufnahmen und anderen visuellen Daten. Effektive medizinische Bildmanagementsysteme ermöglichen Ärzten einen schnellen und einfachen Zugriff auf Patientendaten, was frühere Diagnosen ermöglicht und möglicherweise die Behandlungsergebnisse verbessert. Früherkennung kann nicht nur die Patientenprognose verbessern, sondern auch die Gesamtkosten des Gesundheitswesens senken, indem sie Präventivmaßnahmen ermöglicht und spätere teurere Eingriffe vermeidet. Medizinische Einrichtungen investieren in hochmoderne Bildmanagementsysteme, um Arbeitsabläufe zu optimieren, die Diagnosegenauigkeit zu erhöhen und die Patientenergebnisse zu verbessern. Der Vorstoß zur digitalen Transformation des Gesundheitswesens und die Einhaltung strenger regulatorischer Standards fördern die Einführung umfassender Bildmanagementsysteme, die Datensicherheit, Interoperabilität und eine effiziente Gesundheitsversorgung gewährleisten. Mit der steigenden Nachfrage nach frühzeitiger Krankheitserkennung steigt auch der Bedarf an robusten Lösungen zur medizinischen Bildverwaltung.

Vollständigen Bericht abrufen unter https://www.databridgemarketresearch.com/reports/global-medical-image-management-market

Data Bridge Market Research analysiert, dass der Markt für medizinisches Bildmanagement von 5,66 Milliarden US-Dollar im Jahr 2023 auf 8,47 Milliarden US-Dollar im Jahr 2031 anwachsen dürfte, was einem durchschnittlichen jährlichen Wachstumswachstum von 5,2 % im Prognosezeitraum von 2024 bis 2031 entspricht.

Wichtigste Ergebnisse der Studie

Zunehmende Nutzung bildgebender Geräte

Der zunehmende Einsatz bildgebender Geräte ist ein wichtiger Treiber im Markt für medizinisches Bildmanagement. Er erzeugt eine beträchtliche Menge an Diagnosedaten, die fortschrittliche Managementlösungen erfordern. Da Gesundheitsdienstleister für präzise Diagnostik und Behandlungsplanung zunehmend auf Bildgebungsverfahren wie MRT, CT, Röntgen und Ultraschall zurückgreifen, wächst die Menge der generierten Bilder exponentiell. Dieser Anstieg der Bilddaten erfordert robuste medizinische Bildmanagementsysteme für eine effiziente Speicherung, Abfrage und Analyse. Diese Systeme ermöglichen optimierte Arbeitsabläufe und verbessern die diagnostische Genauigkeit, indem sie schnellen Zugriff auf qualitativ hochwertige Bilder ermöglichen und diese nahtlos in elektronische Patientenakten integrieren. Die zunehmende Komplexität und Auflösung der Bildgebungsverfahren erfordert zudem anspruchsvolle Software, die große Datensätze verarbeiten und die Bildverarbeitung verbessern kann. Mit der fortschreitenden digitalen Transformation im Gesundheitswesen rücken Interoperabilität und Datensicherheit zunehmend in den Vordergrund, was die Einführung umfassender Bildmanagementlösungen weiter vorantreibt. Diese Systeme unterstützen nicht nur die Einhaltung gesetzlicher Vorschriften, sondern ermöglichen auch erweiterte Funktionen wie 3D-Rekonstruktion, Bildfusion und KI-gestützte Diagnostik und verbessern so die klinische Entscheidungsfindung und die Patientenergebnisse. Infolgedessen erlebt der Markt für medizinisches Bildmanagement ein erhebliches Wachstum, das durch die zunehmende Nutzung bildgebender Geräte und den daraus resultierenden Bedarf an effizienten Datenmanagementlösungen vorangetrieben wird.

Berichtsumfang und Marktsegmentierung

Berichtsmetrik

|

Details

|

Prognosezeitraum

|

2024–2031

|

Basisjahr

|

2023

|

Historisches Jahr

|

2022 (Anpassbar auf 2016–2021)

|

Quantitative Einheiten

|

Umsatz in Milliarden USD

|

Abgedeckte Segmente

|

Produkt (Bildarchivierungs- und Kommunikationssystem (PACS), anbieterneutrale Archive (VNA), anwendungsunabhängiges klinisches Archiv (AICA), Enterprise Viewer/Universal Viewer), Bereitstellungsmodell (Hybrid, web-/cloudbasiert und vor Ort), Fachgebiet (Chirurgie, Onkologie, Zahnmedizin und andere), Endbenutzer (Krankenhäuser, Radiologieketten/-zentren, ambulante Operationszentren und andere) und Vertriebskanal (direkte Ausschreibungen, Drittanbieter-Administratoren und andere)

|

Abgedeckte Länder

|

USA, Kanada, Mexiko, Deutschland, Italien, Großbritannien, Frankreich, Schweiz, Spanien, Russland, Türkei, Belgien, Niederlande, übriges Europa, China, Indien, Südkorea, Japan, Thailand, Australien, Singapur, Indonesien, Malaysia, Philippinen, übriger Asien-Pazifik-Raum, Brasilien, Argentinien, übriges Südamerika, Saudi-Arabien, Vereinigte Arabische Emirate, Südafrika, Ägypten, Israel und übriger Naher Osten und Afrika

|

Abgedeckte Marktteilnehmer

|

Unter anderem Agfa-Gevaert Group (Belgien), FUJIFILM Corporation (Japan), Koninklijke Philips NV (Europa), Sectra AB (Europa) und GE HealthCare (USA).

|

Im Bericht behandelte Datenpunkte

|

Zusätzlich zu den Einblicken in Marktszenarien wie Marktwert, Wachstumsrate, Segmentierung, geografische Abdeckung und wichtige Akteure enthalten die von Data Bridge Market Research kuratierten Marktberichte auch ausführliche Expertenanalysen, geografisch dargestellte Produktion und Kapazität nach Unternehmen, Netzwerklayouts von Distributoren und Partnern, detaillierte und aktuelle Preistrendanalysen und Defizitanalysen der Lieferkette und Nachfrage.

|

Segmentanalyse

Der Markt für medizinisches Bildmanagement ist basierend auf Produkt, Liefermodell, Fachgebiet, Endbenutzer und Vertriebskanal in fünf wichtige Segmente unterteilt.

- Basierend auf dem Produkt ist der Markt in Bildarchivierungs- und Kommunikationssysteme (PACS), herstellerneutrale Archive (VNA), anwendungsunabhängige klinische Archive (AICA), Enterprise Viewer/Universal Viewer segmentiert

Im Jahr 2024 wird erwartet, dass das Bildarchivierungs- und Kommunikationssystem (PACS) des Produktsegments den Markt dominieren wird

Im Jahr 2024 wird das Segment der Bildarchivierungs- und Kommunikationssysteme (PACS) voraussichtlich mit einem Marktanteil von 49,04 % den Markt dominieren, da es die Speicherung, Abfrage und Freigabe von Bildern rationalisiert und so die Diagnoseeffizienz und den Arbeitsablauf verbessert.

- Basierend auf dem Bereitstellungsmodell ist der Markt in Hybrid-, Web-/Cloud-basierte und On-Premises-Modelle unterteilt.

Im Jahr 2024 wird das Liefermodell des Angebotssegments voraussichtlich den Markt dominieren

Im Jahr 2024 wird das Hybridsegment voraussichtlich mit einem Marktanteil von 47,83 % den Markt dominieren, da es durch die flexible Integration von lokalen und Cloud-basierten Lösungen sowohl die Datensicherheit als auch die Zugänglichkeit optimiert.

- Der Markt ist nach Fachgebieten in Chirurgie, Onkologie, Zahnmedizin und andere Bereiche unterteilt. Im Jahr 2024 wird das Segment Chirurgie voraussichtlich mit einem Marktanteil von 46,06 % den Markt dominieren.

- Basierend auf dem Endverbraucher ist der Markt in Krankenhäuser, Radiologieketten/-zentren, ambulante Operationszentren und andere segmentiert. Im Jahr 2024 wird das Krankenhaussegment voraussichtlich den Markt mit einem Marktanteil von 46,61 % dominieren.

- Basierend auf den Vertriebskanälen ist der Markt in Direktausschreibungen, Drittanbieter-Administratoren und andere segmentiert. Im Jahr 2024 wird das Segment der Direktausschreibungen voraussichtlich den Markt mit einem Marktanteil von 44,09 % dominieren.

Hauptakteure

Data Bridge Market Research erkennt die folgenden Unternehmen als die wichtigsten Akteure auf dem Markt für medizinisches Bildmanagement an, darunter unter anderem die Agfa-Gevaert Group (Belgien), die FUJIFILM Corporation (Japan), Koninklijke Philips NV (Europa), Sectra AB (Europa) und GE HealthCare (USA).

Marktentwicklung

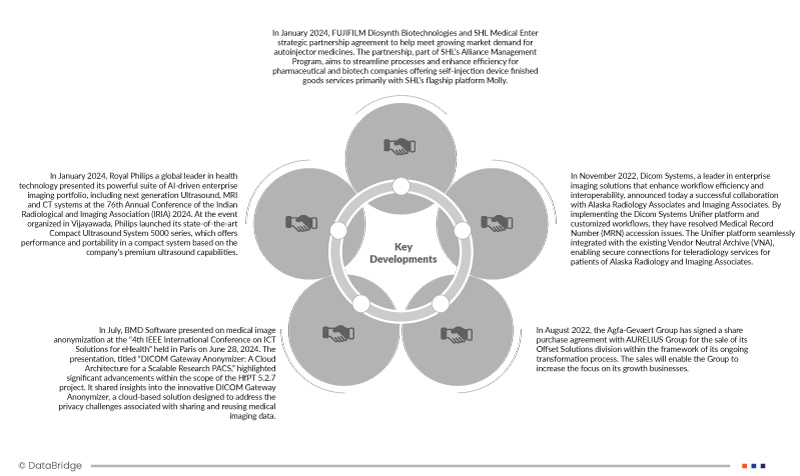

- Im Januar 2024 schließen FUJIFILM Diosynth Biotechnologies und SHL Medical eine strategische Partnerschaft, um die wachsende Marktnachfrage nach Autoinjektoren zu bedienen. Die Partnerschaft, Teil des SHL Alliance Management Programs, zielt darauf ab, Prozesse zu optimieren und die Effizienz für Pharma- und Biotech-Unternehmen zu steigern, die Dienstleistungen für Fertigprodukte im Bereich Selbstinjektionsgeräte anbieten, vor allem mit der SHL-Flaggschiffplattform Molly.

- Im Januar 2024 präsentierte Royal Philips, ein weltweit führendes Unternehmen im Bereich Gesundheitstechnologie, auf der 76. Jahreskonferenz der Indian Radiological and Imaging Association (IRIA) 2024 sein leistungsstarkes Portfolio an KI-gestützter Bildgebung für Unternehmen, darunter Ultraschall-, MRT- und CT-Systeme der nächsten Generation. Auf der in Vijayawada organisierten Veranstaltung stellte Philips seine hochmoderne Compact Ultrasound System 5000-Serie vor, die Leistung und Mobilität in einem kompakten System bietet, das auf den erstklassigen Ultraschallfunktionen des Unternehmens basiert.

- Im Juli präsentierte BMD Software auf der 4. IEEE International Conference on ICT Solutions for eHealth, die am 28. Juni 2024 in Paris stattfand, die Anonymisierung medizinischer Bilder. Der Vortrag mit dem Titel „DICOM Gateway Anonymizer: Eine Cloud-Architektur für ein skalierbares Forschungs-PACS“ hob bedeutende Fortschritte im Rahmen des HfPT 5.2.7-Projekts hervor. Er gab Einblicke in den innovativen DICOM Gateway Anonymizer, eine Cloud-basierte Lösung, die die Datenschutzherausforderungen im Zusammenhang mit der Weitergabe und Wiederverwendung medizinischer Bilddaten adressiert.

- Im August 2022 hat die Agfa-Gevaert-Gruppe im Rahmen ihres laufenden Transformationsprozesses einen Aktienkaufvertrag mit der AURELIUS-Gruppe über den Verkauf ihres Geschäftsbereichs Offset Solutions unterzeichnet. Der Verkauf ermöglicht es dem Konzern, sich stärker auf seine Wachstumsgeschäfte zu konzentrieren.

Regionale Analyse

Geografisch betrachtet sind die im globalen Marktbericht zum medizinischen Bildmanagement abgedeckten Länder die USA, Kanada, Mexiko, Deutschland, Italien, Großbritannien, Frankreich, die Schweiz, Spanien, Russland, die Türkei, Belgien, die Niederlande und das übrige Europa, China, Indien, Südkorea, Japan, Thailand, Australien, Singapur, Indonesien, Malaysia, die Philippinen und der übrige asiatisch-pazifische Raum, Brasilien, Argentinien, das übrige Südamerika, Saudi-Arabien, die Vereinigten Arabischen Emirate, Südafrika, Ägypten, Israel und der übrige Nahe Osten und Afrika

Laut Marktforschungsanalyse von Data Bridge:

Nordamerika ist die dominierende und am schnellsten wachsende Region im Markt für medizinisches Bildmanagement im Prognosezeitraum von 2024 bis 2031

Im Jahr 2024 wird Nordamerika voraussichtlich den Markt dominieren. Dies ist auf die gut ausgebaute Gesundheitsinfrastruktur, die weit verbreitete Nutzung fortschrittlicher Bildgebungstechnologien und hohe Investitionen in die Gesundheits-IT zurückzuführen. Der starke regulatorische Rahmen und die hohe Nachfrage nach effizienten Diagnoseinstrumenten tragen ebenfalls zur Marktführerschaft der Region bei.

Die USA werden voraussichtlich in Nordamerika dominieren. Grund dafür sind ihr hochentwickeltes Gesundheitssystem, der breite Einsatz fortschrittlicher Bildgebungstechnologien und hohe Investitionen in Gesundheits-IT und digitale Gesundheitsinitiativen. Die Präsenz führender Marktteilnehmer, ein starkes regulatorisches Umfeld und der Fokus auf die Verbesserung der Patientenergebnisse durch effiziente Diagnoseinstrumente stärken die Dominanz der USA in diesem Markt zusätzlich.

Für detailliertere Informationen zum globalen Marktbericht zum medizinischen Bildmanagement klicken Sie hier – https://www.databridgemarketresearch.com/reports/global-medical-image-management-market