Global Semiconductor Automated Test Equipment Market

Market Size in USD Billion

CAGR :

%

USD

5.46 Billion

USD

8.35 Billion

2024

2032

USD

5.46 Billion

USD

8.35 Billion

2024

2032

| 2025 –2032 | |

| USD 5.46 Billion | |

| USD 8.35 Billion | |

| % | |

|

Semiconductor Automated Test Equipment Market Size

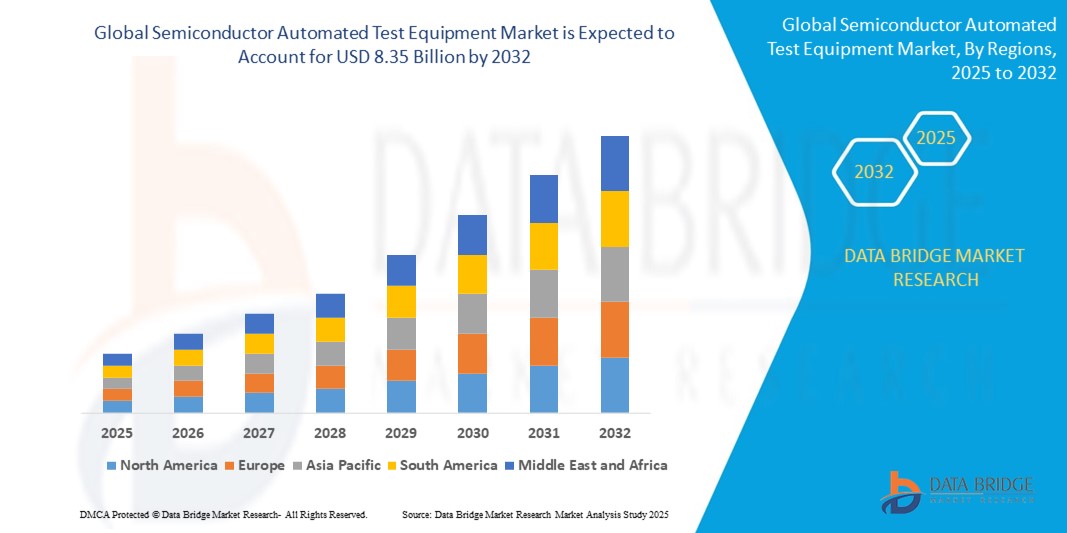

- The Global Semiconductor Automated Test Equipment Market size was valued at USD 5.46 billion in 2024 and is expected to reach USD 8.35 billion by 2032, at a CAGR of 5.45% during the forecast period

- The market growth is largely fueled by rising demand and adoption of connected devices coupled with rising demand for cost effective testing of devices

Semiconductor Automated Test Equipment Market Analysis

- Automated Test Equipment (ATE) plays a pivotal role in semiconductor manufacturing by enabling precise testing, validation, and quality assurance of semiconductor devices. These systems improve production yield, reduce time-to-market, and ensure the reliability of increasingly complex semiconductor chips used in consumer electronics, automotive, telecommunications, and industrial applications.

- Market growth is driven by rising demand for advanced semiconductor devices, especially in emerging technologies such as 5G, artificial intelligence (AI), Internet of Things (IoT), and automotive electronics. The need for high-throughput and accurate testing solutions for smaller, more complex chips propels the adoption of sophisticated ATE systems.

- North America is projected to lead the global Semiconductor Automated Test Equipment Market with 56.90% in 2024 , supported by the presence of major semiconductor manufacturers, strong R&D investments, and early adoption of cutting-edge test technologies. The region’s focus on innovation and quality control contributes to its dominant market position.

- The Asia Pacific region is expected to register the fastest growth during the forecast period, driven by rapid semiconductor industry expansion in China, Taiwan, South Korea, and Japan. Government initiatives to boost local semiconductor fabrication capacity, coupled with growing consumer electronics demand, fuel the need for automated test equipment.

- The Wafer ATE segment dominates and holds the larger market share of 51.80% in 2024, driven by the increasing demand for wafer-level testing in semiconductor fabrication to ensure early defect detection and improve production yield. Wafer ATE’s role in testing integrated circuits at the wafer stage is critical for reducing downstream failures and enhancing product quality

Report Scope and Semiconductor Automated Test Equipment Market Segmentation

|

Attributes |

Semiconductor Automated Test Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Semiconductor Automated Test Equipment Market Trends

“Increasing Integration of AI and Machine Learning in Test Automation”

- A key trend transforming the semiconductor automated test equipment market is the incorporation of artificial intelligence (AI) and machine learning (ML) technologies to enhance test accuracy, speed, and predictive maintenance.

- These advanced algorithms enable real-time data analysis during testing, optimizing test parameters dynamically and reducing test cycle time and costs.

- For instance, in 2024, major semiconductor manufacturers in Taiwan adopted AI-powered test platforms to analyze test data patterns and predict potential failures before they occur. This integration led to improved yield rates and shortened time-to-market for new chips.

- The combination of AI, big data analytics, and automation is accelerating smarter and more efficient testing processes, vital for complex semiconductor devices such as SoCs and advanced memory chips.

Semiconductor Automated Test Equipment Market Dynamics

Driver

“Rising Demand for High-Performance and Complex Semiconductor Devices”

- The growing demand for advanced semiconductor devices in applications such as 5G, AI, automotive electronics, and IoT is a major driver fueling the need for sophisticated automated test equipment.

- As chip complexity increases with smaller nodes and multi-functional integration, testing requirements become more stringent, pushing manufacturers to invest heavily in advanced ATE solutions

- For example, in early 2025, semiconductor fabs in South Korea expanded their ATE capacities to support testing of 5nm and below technology node chips for smartphone and automotive applications.

- This trend ensures consistent product quality, enhances yield, and supports rapid innovation in semiconductor design and manufacturing

Restraint/Challenge

“High Capital Expenditure and Complexity in Test Equipment Deployment”

- A significant challenge faced by the semiconductor ATE market is the high cost and complexity associated with acquiring and deploying automated test systems.

- Advanced ATE platforms require substantial upfront investments, long development cycles, and specialized expertise to integrate and maintain, which can be prohibitive for small and medium-sized manufacturers.

- For example, a mid-sized fab in Europe delayed expansion plans in 2024 due to the steep costs and technical challenges of upgrading to the latest ATE for next-generation chip testing.

- Additionally, rapid technological changes in semiconductor design demand continuous updates and customization of ATE systems, adding to operational challenges and expenses.

Semiconductor Automated Test Equipment Market Scope

The market is segmented on the basis of type, product type, and application.

- By Type

On the basis of type, the Semiconductor Automated Test Equipment Market is segmented into Wafer ATE and Packaged Device ATE. The Wafer ATE segment dominates and holds the larger market share of 51.80% in 2024, driven by the increasing demand for wafer-level testing in semiconductor fabrication to ensure early defect detection and improve production yield. Wafer ATE’s role in testing integrated circuits at the wafer stage is critical for reducing downstream failures and enhancing product quality

The Packaged Device ATE segment is anticipated to witness the fastest growth rate of 21.17% from 2025 to 2032, the rising complexity of packaged ICs and the growing need for comprehensive final testing solutions across various industries.

- By Product Type

On the basis of Product Type, the Semiconductor Automated Test Equipment Market is segmented into Memory, Non-Memory, Discrete, and Others. Non-Memory segment dominates the market revenue share in 2024, propelled by the growing application of logic, analog, and mixed-signal ICs in smartphones, consumer electronics, and automotive electronics.

The Memory segment is also expanding steadily due to the increasing use of memory chips in data centers, IoT devices, and consumer electronics, requiring high-throughput and accurate testing solutions.

- By Application

On the basis of application, the Semiconductor Automated Test Equipment Market is segmented into Automotive Electronics, Consumer Electronics, Telecom and IT, Industrial, Medical, Military and Defence, and Others. Consumer Electronics holds the largest market share as of 2024, driven by booming demand for smartphones, wearables, and smart devices requiring rigorous chip testing to meet quality and performance standards.

Automotive Electronics is witnessing the fastest growth, spurred by the rising adoption of electric vehicles (EVs), ADAS systems, and connected car technologies that demand high reliability and precision in semiconductor testing. Telecom and IT applications are also growing robustly due to the expansion of 5G networks and data center infrastructure, which rely heavily on advanced semiconductor testing solutions.

Semiconductor Automated Test Equipment Market Regional Analysis

- North America is projected to lead the global Semiconductor Automated Test Equipment Market with 56.90% in 2024 , supported by the presence of major semiconductor manufacturers, strong R&D investments, and early adoption of cutting-edge test technologies. The region’s focus on innovation and quality control contributes to its dominant market position.

- The region benefits from robust demand for high-speed processors and memory components, especially in data centers, autonomous vehicles, and consumer electronics.

U.S. Semiconductor Automated Test Equipment Market Insight

- The U.S. Semiconductor Automated Test Equipment Market captured the largest revenue share of 81% in 2024 within North America, owing to its advanced semiconductor ecosystem comprising key industry players like Intel, NVIDIA, and Texas Instruments.

- Demand for ATE is accelerating due to increased wafer production, expansion of fabrication plants (fabs), and the shift toward 3nm and below process nodes.

Europe Semiconductor Automated Test Equipment Market Insight

- Europe is expected to grow steadily through the forecast period, backed by rising investments in semiconductor self-sufficiency, particularly through the EU Chips Act.

- The demand for ATE is being driven by the automotive sector, where strict safety and reliability standards require rigorous IC testing.

- Countries like Germany, France, and the Netherlands are expanding semiconductor R&D and chip manufacturing, increasing the need for both wafer and packaged device ATE.

Germany Semiconductor Automated Test Equipment Market Insight

- Germany leads the European market with a strong emphasis on automotive-grade semiconductor testing.

- The growth is fueled by the rapid electrification of vehicles and adoption of ADAS (Advanced Driver Assistance Systems), which require extensive chip validation.

- German automotive suppliers and semiconductor fabs are investing in high-throughput test systems to ensure safety, performance, and regulatory compliance in electronic control units (ECUs).

Asia-Pacific Semiconductor Automated Test Equipment Market Insight

- The Asia-Pacific Semiconductor Automated Test Equipment Market is poised to grow at the fastest CAGR of 9.8% during the forecast period of 2025 to 2032, driven by the region’s dominance in global semiconductor manufacturing and testing activities.

- Major foundries in Taiwan, South Korea, and China are expanding capacity and investing in next-gen ATE to support growing demand for advanced chips in smartphones, electric vehicles, and industrial IoT applications.

- The region benefits from a cost-efficient workforce, well-developed electronics infrastructure, and increasing government initiatives to boost semiconductor capabilities.

Japan Semiconductor Automated Test Equipment Market Insight

- Japan continues to be a key market for ATE, supported by its long-standing expertise in semiconductor design, testing, and packaging.

- Japanese firms are modernizing legacy testing infrastructure to accommodate advanced chips used in automotive, robotics, and consumer electronics.

- The push for energy-efficient, high-precision testing equipment is also gaining momentum, aligning with Japan’s focus on quality and technological innovation.

China Semiconductor Automated Test Equipment Market Insight

- China represents the largest revenue share in Asia-Pacific as of 2025, fueled by national policies promoting chip self-reliance and the expansion of local fabs.

- Leading Chinese chip manufacturers are adopting sophisticated automated test equipment to improve defect detection and reduce time-to-market.

- The surge in electric vehicle production, 5G deployment, and industrial automation is boosting demand for high-volume and high-performance ATE systems.

Semiconductor Automated Test Equipment Market Share

The Semiconductor Automated Test Equipment industry is primarily led by well-established companies, including:

- Virgina Panel Corporation (US)

- MAC Panel Company (US)

- NATIONAL INSTRUMENTS CORP. (US)

- SPEA S.p.A. (Italy)

- Teradyne Inc. (US)

- ADVANTEST CORPORATION (Japan)

- Cohu, Inc. (US)

- Astronics Corporation (US)

- Chroma Systems Solutions, Inc. (Taiwan)

- Averna (Canada)

- Shibasoku Co., Ltd. (Japan)

- Hangzhou ChangChuan Technology Co., Ltd. (China)

- ROOS INSTRUMENTS, INC. (US)

- STAr Technologies Inc. (US)

- Aeroflex USA, Inc. (US)

- Danaher (US)

- Aemulus Corporation Sdn Bhd. (Malaysia)

- Marvin Test Solutions, Inc. (US)

- miconindia.com (India)

- METTLER TOLEDO (US)

Latest Developments in Global Semiconductor Automated Test Equipment Market

- In May 2025, Advantest introduced SiConic™, a scalable solution designed for automated silicon validation of complex system-on-chip (SoC) devices. SiConic™ aims to accelerate design verification and silicon validation processes, enabling engineers to achieve faster sign-offs with enhanced reliability and efficiency. This launch addresses the growing complexity in semiconductor designs, particularly in AI and high-performance computing applications.

- In January 2025, Continental announced a strategic partnership with Mobileye, a leader in advanced driver-assistance systems (ADAS), to jointly develop next-generation rear cross traffic alert solutions. The collaboration aims to leverage Mobileye’s computer vision expertise and Continental’s sensor technology to improve system reliability and reduce false alerts. This partnership is expected to accelerate the integration of RCTA systems in mid-range and luxury vehicles globally.

- In February 2025, Nissan expanded its vehicle safety suite by making Rear Cross Traffic Alert a standard feature across its newly launched SUV models. This move marks Nissan’s push toward enhancing driver safety and aligns with increasing consumer demand for advanced safety features in affordable vehicles. The company reported that early customer feedback indicates improved confidence in tight parking and reversing scenarios.

- In December 2024, Magna International completed the acquisition of Eyeris Technologies, a company specializing in AI-based vision systems for automotive applications. This acquisition is set to strengthen Magna’s position in the RCTA market by integrating AI-driven image processing and object detection capabilities, enabling more precise detection of cross traffic hazards. The deal supports Magna’s strategy to expand its sensor and software offerings for advanced vehicle safety.

- In April 2025, Hyundai launched an innovative Rear Cross Traffic Alert system that incorporates Vehicle-to-Everything (V2X) communication technology. This system enables vehicles to exchange real-time information about approaching cross traffic, including non-visible vehicles like bicycles and pedestrians, thereby enhancing alert accuracy and reaction time. Hyundai’s new system debuted in its latest electric vehicle model and showcases the company’s focus on smart mobility and connected vehicle safety.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Semiconductor Automated Test Equipment Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Semiconductor Automated Test Equipment Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Semiconductor Automated Test Equipment Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.