North America Medical Display Market, By Technology (LED-Backlit LCD Display, CCFL-Backlit LCD Display, TFT LCD Display And OLED Display), Panel Size (Under 22.9" Inch Panels, 23.0"- 32.0" Inch Panels, 27.0-41.9 Inch Panels and Above 42 Inch Panels), Viewing Mode (2D and 3D), Megapixel (UP TO 2MP, 2.1–4MP, 4.1–8MP and above 8MP), Resolution (4K, Ultra Full HD, Full HD and Others), Display Type (Wall Mounted, Portable, Modular), Imaging Technology (Touch Screen, Scratch Resistant Font Glass, Failsafe Mode, Cleanable Options, Softglow & Spotview And Others), Display Color (Colour, Monochrome), Aspect Ratio (16.09, 21.09, 4.03), Component (Hardware and Services), Application (Consultation, Diagnostic, Surgical/Interventional, Telehealth, Teaching / Practice, Fetal Monitoring, Dentistry, Point Of Care, Patient-Worn Monitoring And Others) End User (Hospitals, Clinics, Nursing Facilities, Diagnostic Laboratories, Imaging/Radiology Lab, Laboratory, Rehabilitation Centers And Others), Distribution Channel (Direct Tender, Retail Sales and Others) - Industry Trends and Forecast to 2029.

North America Medical Display Market Analysis and Insights

The main reasons for the growth of the medical display market is the rising demand for minimally invasive treatments (MIT) due to multiple benefits such as less post-operative pain, fewer operative, and major post-operative complications, shortened hospital stay, faster recovery times, less scarring, less stress on the immune system, smaller incision, and for some procedures it reduced operating time and reduced costs as well.

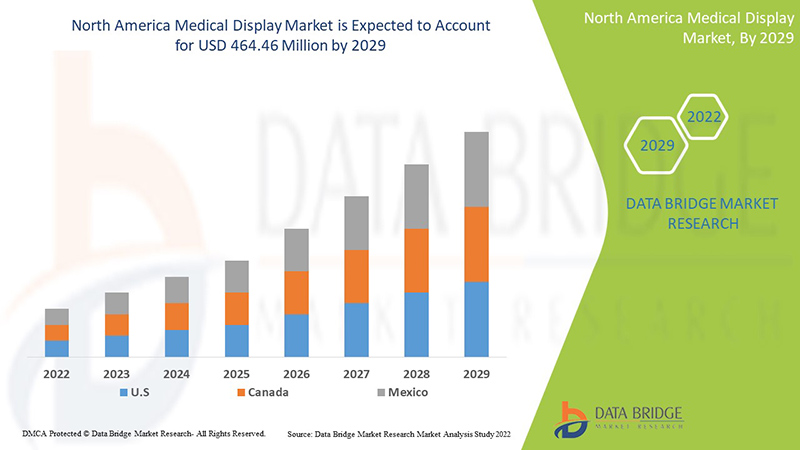

Data Bridge Market Research analyzes that the medical display market is expected to reach the value of USD 464.46 million by 2029, at a CAGR of 6.5% during the forecast period. This market report also covers pricing analysis, patent analysis, and technological advancements in depth.

|

Report Metric |

Details |

|

Forecast Period |

2022 to 2029 |

|

Base Year |

2021 |

|

Historic Years |

2020 (Customizable to 2019-2014) |

|

Quantitative Units |

Revenue in USD Million, Pricing in USD |

|

Segments Covered |

By Technology (LED-Backlit Lcd Display, CCFL-Backlit LCD Display, TFT LCD Display And OLED Display), Panel Size (Under 22.9" Inch Panels, 23.0"- 32.0" Inch Panels, 27.0-41.9 Inch Panels and Above 42 Inch Panels), Viewing Mode (2D and 3D), Megapixel (UP TO 2MP, 2.1–4MP, 4.1–8MP and above 8MP), Resolution (4K, Ultra Full HD, Full HD and Others), Display Type (Wall Mounted, Portable, Modular), Imaging Technology (Touch Screen, Scratch Resistant Font Glass, Failsafe Mode, Cleanable Options, Softglow & Spotview And Others), Display Color (Colour, Monochrome), Aspect Ratio (16.09, 21.09, 4.03), Component (Hardware and Services), Application (Consultation, Diagnostic, Surgical/Interventional, Telehealth, Teaching / Practice, Fetal Monitoring, Dentistry, Point Of Care, Patient-Worn Monitoring And Others) End User (Hospitals, Clinics, Nursing Facilities, Diagnostic Laboratories, Imaging/Radiology Lab, Laboratory, Rehabilitation Centers And Others), Distribution Channel (Direct Tender, Retail Sales and Others) |

|

Countries Covered |

U.S., Canada, Mexico |

|

Market Players Covered |

BenQ, ALPINION MEDICAL SYSTEMS Co., Ltd, Nanjing Jusha Commercial &Trading Co,Ltd, COJE CO.,LTD., Axiomtek Co., Ltd., Dell Inc., HP Development Company, L.P., Reshin, Onyx Healthcare Inc., Teguar Computers., Shenzhen Beacon Display Technology Co., Ltd., Rein Medical, STERIS., Barco., Hisense., Sony Corporation, Advantech Co., Ltd., LG Electronics., Sharp NEC Display Solutions, Koninklijke Philips N.V., EIZO INC., Novanta Inc., FSN Medical Technologies., Quest, Ampronix., Siemens Healthcare GmbH, Panasonic Corporation, among others. |

Medical Display Market Definition

A medical display is a monitor that meets the high demands of medical imaging. It usually comes with special image-enhancing technologies to ensure consistent brightness over the lifetime of the display, noise-free images, ergonomic reading and automated compliance with digital imaging and communications in medicine (DICOM) and other medical standards.

The development of medical imaging technologies has progressed healthcare, providing powerful diagnostic tools, supporting the non-invasive assessment of injuries and internal issues, and enabling diseases to be detected far earlier than ever before. Medical displays are preferred over consumer displays when used for medical imaging. The reason is simple: medical displays meet set requirements for image quality, medical regulations, and quality assurance.

The future of medical display devices are based on the developments in artificial intelligence (AI) and data analytics. Medical devices are advancing disease management by allowing clinicians to personalize medicine like never before. These technologies provide revelatory insights into individual patients in real-time.

Medical Display Market Dynamics

Cette section traite de la compréhension des moteurs, des avantages, des opportunités, des contraintes et des défis du marché. Tout cela est discuté en détail ci-dessous :

Conducteurs

- La tendance croissante vers un traitement minimalement invasif

Les principales raisons de la croissance du marché de l'affichage médical en Amérique du Nord sont la demande croissante de traitements mini-invasifs (MIT) en raison de multiples avantages tels que moins de douleurs postopératoires, moins de complications opératoires et postopératoires majeures, un séjour hospitalier raccourci, des temps de récupération plus rapides, moins de cicatrices, moins de stress sur le système immunitaire, une incision plus petite et, pour certaines procédures, une réduction du temps opératoire et des coûts également.

La chirurgie mini-invasive est une excellente approche pour diagnostiquer et traiter un large éventail de troubles thoraciques qui nécessitaient auparavant une sternotomie ou une thoracotomie ouverte. La prévalence des maladies chroniques nécessitant une intervention chirurgicale a augmenté dans le monde entier. En raison des nombreux avantages du traitement mini-invasif, de nombreux patients le préfèrent. De plus, les chirurgies vasculaires et endovasculaires, les chirurgies neurologiques et rachidiennes, les soins orthopédiques en traumatologie et les chirurgies cardiaques sont pratiqués dans des salles d'opération hybrides. Cette caractéristique permet aux hôpitaux d'effectuer des opérations chirurgicales avancées, ce qui augmente la demande d'écrans médicaux. En outre, l'augmentation des coûts des soins de santé et le nombre de laboratoires de pathologie et de radiologie stimulent la demande d'écrans médicaux.

La chirurgie mini-invasive permet aux chirurgiens d'utiliser des technologies modernes et des techniques chirurgicales avancées pour opérer le corps humain de manière moins nocive. Cela devrait stimuler la demande de chirurgies mini-invasives.

- Infrastructures de santé en pleine croissance

Les gouvernements et les organisations à but non lucratif de plusieurs pays se concentrent principalement sur le développement des infrastructures de santé pour minimiser la charge de morbidité et fournir de meilleurs services de santé. En outre, l'adoption d'appareils médicaux, d'écrans, de moniteurs et de divers autres appareils de pointe a augmenté. Tous ces facteurs sont susceptibles de créer des opportunités favorables à la croissance du marché au cours de la période de prévision. En outre, les investissements importants des principaux acteurs dans le lancement de produits innovants et la mise à jour des fonctionnalités au cours des prochaines années peuvent également stimuler le marché.

En outre, la demande croissante de services de santé rentables, la demande croissante de solutions techniques, la mobilité croissante des informations, l'augmentation des initiatives et des incitations gouvernementales et l'augmentation du financement des écrans médicaux de haute qualité dans les hôpitaux et les centres de recherche devraient stimuler ces établissements de santé sur le marché. L'infrastructure logicielle médicale a constitué la base des avancées récentes dans les écrans médicaux, les bibliothèques médicales numériques et les systèmes d'information de gestion. Ces facteurs devraient stimuler la croissance du marché nord-américain des écrans médicaux.

Opportunité

- Progrès technologiques dans les instruments d'affichage médical

Alors que le marché se concentre sur la production de formes galéniques à administration orale, il existe une lutte constante pour développer des formulations appropriées de nouvelles molécules qui permettent l'administration orale et, simultanément, garantissent au médicament une biodisponibilité optimale chez les patients. Pour surmonter ce problème, les fabricants d'excipients pharmaceutiques développent des produits plus simples et réduisent le temps et les coûts de développement. Le développement des technologies d'affichage médical a changé le secteur de la santé, en fournissant des outils de diagnostic, la télésanté, en fournissant un soutien pour les traitements non invasifs, en permettant l'évaluation des maladies et en permettant leur détection plus précoce.

Le lancement de développements technologiques dans les dispositifs d'affichage médical améliore l'efficacité de l'affichage médical et augmente la facilité d'utilisation des dispositifs d'affichage médical. L'essor des applications technologiques dans les dispositifs d'affichage médical entraînerait une réduction de la main-d'œuvre et un diagnostic et une guérison rapides des maladies. À l'avenir, la technologie de l'intelligence artificielle remplacera le marché de l'affichage médical. Ce facteur devrait constituer une opportunité pour la croissance du marché de l'affichage médical en Amérique du Nord au cours de la période de prévision.

Retenue/Défis

- Coûts élevés des dispositifs d’affichage médicaux

Le coût élevé des dispositifs d'affichage et leur mise en œuvre sont les principaux facteurs qui freinent la croissance du marché, en particulier dans les pays où le scénario de remboursement est médiocre. La plupart des établissements de santé des pays en développement, tels que les hôpitaux et les centres de diagnostic, ne peuvent pas se permettre ces appareils en raison des coûts d'installation et de maintenance élevés. En raison du coût élevé de ces équipements médicaux et des faibles ressources financières, les établissements de santé des pays émergents sont réticents à investir dans de nouveaux systèmes technologiquement avancés. Ces facteurs peuvent entraver la numérisation des établissements de santé et avoir un impact sur l'adoption de technologies avancées pour le diagnostic et l'analyse.

Les progrès technologiques conduisant au développement de dispositifs d'affichage avancés et innovants font grimper le coût de ces dispositifs. Ainsi, le coût élevé des dispositifs d'affichage devrait freiner la croissance du marché.

Développements récents

- En juin 2022, EIZO Corporation a lancé le RadiForce MX243W, un moniteur de 24,1 pouces et 2,3 mégapixels (1920 x 1200 pixels). Le moniteur de 24,1 pouces et 2,3 mégapixels (1920 x 1200 pixels) a été conçu pour une surveillance et un diagnostic minutieux de la physiologie complète du système du patient dans les cliniques et les hôpitaux. Le lancement a permis l'ajout d'un nouveau dispositif médical au portefeuille et a offert une pureté de marché exceptionnelle

- En mai 2021, Barco a lancé l'écran médical Nio Fusion 12MP. Le lancement du produit a donné lieu à un portefeuille de produits amélioré et à une augmentation des ventes et à l'expansion de la gamme de produits d'affichage médical en Amérique du Nord et en Europe

Portée du marché de l'affichage médical en Amérique du Nord

Le marché nord-américain des écrans médicaux est divisé en treize segments notables basés sur la technologie, la taille du panneau, le mode d'affichage, le mégapixel, la résolution, le type d'affichage, la technologie d'imagerie, la couleur d'affichage, le rapport hauteur/largeur, le composant, l'application, l'utilisateur final et le canal de distribution. La croissance entre les segments vous aide à analyser les niches de croissance et les stratégies pour aborder le marché et déterminer vos principaux domaines d'application et la différence entre vos marchés cibles.

MARCHÉ DES ÉCRANS MÉDICAUX EN AMÉRIQUE DU NORD, PAR TECHNOLOGIE

- ÉCRAN LCD RÉTROÉCLAIRÉ PAR LED

- ÉCRAN LCD RÉTROÉCLAIRÉ CCFL

- ÉCRAN LCD TFT

- ÉCRAN OLED

Sur la base de la technologie, le marché de l'affichage médical est segmenté en écran LCD rétroéclairé par LED, écran LCD rétroéclairé par CCFL, écran LCD TFT et écran OLED.

MARCHÉ DES AFFICHAGES MÉDICAUX EN AMÉRIQUE DU NORD, PAR TAILLE DE PANNEAU

- PANNEAUX DE MOINS DE 22,9 POUCES

- PANNEAUX DE 23,0 À 26,9 POUCES

- PANNEAUX DE 27,0 À 41,9 POUCES

- PANNEAUX DE PLUS DE 42 POUCES

Sur la base de la taille du panneau, le marché de l'affichage médical est segmenté en panneaux de moins de 22,9 pouces, panneaux de 23,0 à 32,0 pouces, panneaux de 27,0 à 41,9 pouces et panneaux de plus de 42 pouces.

MARCHÉ DE L'AFFICHAGE MÉDICAL EN AMÉRIQUE DU NORD, PAR MODE DE VISUALISATION

- 2D

- 3D

Sur la base du mode de visualisation, le marché de l’affichage médical est segmenté en 2D et 3D.

MARCHÉ DE L'AFFICHAGE MÉDICAL EN AMÉRIQUE DU NORD, PAR MEGAPIXEL

- JUSQU'À 2MP

- 2,1 à 4 MP

- 4,1 à 8 MP

- AU-DESSUS DE 8MP

Sur la base des mégapixels, le marché des écrans médicaux est segmenté en JUSQU'À 2 MP, 2,1-4 MP, 4,1-8 MP et plus de 8 MP.

MARCHÉ DE L'AFFICHAGE MÉDICAL EN AMÉRIQUE DU NORD, PAR RÉSOLUTION

- Full HD

- ULTRA FULL HD

- 4K

- AUTRES

Sur la base de la résolution, le marché de l'affichage médical est segmenté en Full HD, Ultra Full HD, 4K et autres.

MARCHÉ DES AFFICHAGES MÉDICAUX EN AMÉRIQUE DU NORD, PAR TYPE D'AFFICHAGE

- MONTAGE MURAL

- PORTABLE

- MODULAIRE

Sur la base du type d'affichage, le marché des écrans médicaux est segmenté en écrans muraux, portables et modulaires.

MARCHÉ DES AFFICHAGES MÉDICAUX EN AMÉRIQUE DU NORD, PAR TECHNOLOGIE D'IMAGERIE

- ÉCRAN TACTILE

- VERRE DE POLICE RÉSISTANT AUX RAYURES

- MODE DE SÉCURITÉ INTÉGRÉE

- OPTIONS DE NETTOYAGE

- SOFTGLOW ET SPOTVIEW

- AUTRES

Sur la base de la technologie d'imagerie, le marché de l'affichage médical est segmenté en écran tactile, verre de police résistant aux rayures, mode de sécurité intégrée, options de nettoyage, softglow et spotview et autres.

MARCHÉ DE L'AFFICHAGE MÉDICAL EN AMÉRIQUE DU NORD, PAR COULEUR D'AFFICHAGE

- COULEUR

- MONOCHROME

Sur la base de la couleur d'affichage, le marché de l'affichage médical est segmenté en couleur et monochrome.

MARCHÉ DES AFFICHAGES MÉDICAUX EN AMÉRIQUE DU NORD, PAR RAPPORT D'ASPECT

- 16:09

- 21:09

- 4:03

Sur la base du rapport hauteur/largeur, le marché de l'affichage médical est segmenté en 16:09, 21:09 et 4:03.

MARCHÉ DES AFFICHAGES MÉDICAUX EN AMÉRIQUE DU NORD, PAR COMPOSANT

- MATÉRIEL

- SERVICES

Sur la base des composants, le marché de l'affichage médical est segmenté en matériel et services.

- MARCHÉ DE L'AFFICHAGE MÉDICAL EN AMÉRIQUE DU NORD, PAR APPLICATION

- DIAGNOSTIC

- CHIRURGICAL/INTERVENTIONNEL

- SURVEILLANCE PORTÉE PAR LE PATIENT

- CONSULTATION

- TÉLÉSANTÉ

- ENSEIGNEMENT/PRATIQUE

- DENTISTERIE

- POINT DE SOINS

- SURVEILLANCE FŒTALE

- AUTRES

On the basis of application, the medical display market is segmented into consultation, diagnostic, surgical/interventional, telehealth, teaching / practice, fetal monitoring, dentistry, point of care, patient-worn monitoring and others.

NORTH AMERICA MEDICAL DISPLAY MARKET, BY END USER

- HOSPITALS

- BY TECHNOLOGY

- CLINICS

- NURSING FACILITIES

- DIAGNOSTIC LABORATORIES

- IMAGING/RADIOLOGY LAB

- LABORATORY

- REHABILITATION CENTERS

- OTHERS

On the basis of end user, the medical display market is segmented into hospitals, clinics, nursing facilities, diagnostic laboratories, imaging/radiology lab, laboratory, rehabilitation centers and others.

NORTH AMERICA MEDICAL DISPLAY MARKET, BY DISTRIBUTION CHANNEL

- DIRECT TENDER

- RETAIL SALES

- OTHERS

On the basis of distribution channel, the medical display market is segmented into direct tender, retail sales and others.

Medical Display Market Regional Analysis/Insights

The medical display market is analyzed and market size information is provided technology, panel size, viewing mode, megapixel, resolution, display type, imaging technology, display color, aspect ratio, component, application, end user and distribution channel.

The countries covered in this market report are U.S., Canada, Mexico.

North America is expected to dominate the market as it is the largest medical device market in the world. The U.S is expected to dominate the market due to rise in disposable income of the people.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impact the current and future trends of the market. Data points such as new sales, replacement sales, country demographics, regulatory acts, and import-export tariffs are some of the major pointers used to forecast the market scenario for individual countries. Also, presence and availability of North America brands and their challenges faced due to large or scarce competition from local and domestic brands, and impact of sales channels are considered while providing forecast analysis of the country data.

Competitive Landscape and Medical Display Market Share Analysis

The medical display market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in R&D, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product trials pipelines, product approvals, patents, product width and breath, application dominance, technology lifeline curve. The above data points provided are only related to the company’s focus on the medical display market.

Some of the major players operating in the,market are BenQ, ALPINION MEDICAL SYSTEMS Co., Ltd, Nanjing Jusha Commercial &Trading Co,Ltd, COJE CO.,LTD., Axiomtek Co., Ltd., Dell Inc., HP Development Company, L.P., Reshin, Onyx Healthcare Inc., Teguar Computers., Shenzhen Beacon Display Technology Co., Ltd., Rein Medical, STERIS., Barco., Hisense., Sony Corporation, Advantech Co., Ltd., LG Electronics., Sharp NEC Display Solutions, Koninklijke Philips N.V., EIZO INC., Novanta Inc., FSN Medical Technologies., Quest, Ampronix., Siemens Healthcare GmbH, Panasonic Corporation, among others.

Research Methodology: Medical Display Market

Data collection and base year analysis are done using data collection modules with large sample sizes. The market data is analyzed and estimated using market statistical and coherent models. In addition, market share analysis and key trend analysis are the major success factors in the market report. The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market, and primary (industry expert) validation. Apart from this, data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Company Market Share Analysis, Standards of Measurement, North America vs Regional, and Vendor Share Analysis. Please request analyst call in case of further inquiry.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Table des matières

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF NORTH AMERICA MEDICAL DISPLAY MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 TECHNOLOGYLIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET APPLICATION COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

3.1 PESTEL

3.2 PORTER'S FIVE FORCES MODEL

3.3 TECHNOLOGICAL LANDSCAPE IN THE NORTH AMERICA MEDICAL DISPLAY MARKET

3.3.1 ORGANIC LIGHT EMITTING DIODE (OLED)

3.3.2 LIGHT EMITTING DIODE (LED), TECHNOLOGY

3.3.3 LIQUID CRYSTAL DISPLAY (LCD)

4 VALUE CHAIN ANALYSIS: NORTH AMERICA MEDICAL DISPLAY MARKET

5 NORTH AMERICA MEDICAL DISPLAY MARKET: REGULATIONS

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 THE GROWING TREND TOWARDS MINIMALLY INVASIVE TREATMENT

6.1.2 GROWING HEALTHCARE INFRASTRUCTURE

6.1.3 SURGE IN THE NUMBER OF DIAGNOSTIC IMAGING CENTERS

6.2 RESTRAINTS

6.2.1 INCREASE IN USE OF REFURBISHED MEDICAL DISPLAYS

6.2.2 MEDICAL COMMUNITY HAS ATTEMPTED TO TAKE ADVANTAGE

6.2.3 HIGH COSTS OF MEDICAL DISPLAY DEVICES

6.3 OPPORTUNITIES

6.3.1 STRATEGIC INITIATIVES BY MARKET PLAYERS

6.3.2 TECHNOLOGICAL ADVANCEMENTS IN MEDICAL DISPLAY INSTRUMENTS

6.3.3 RISING DISPOSABLE INCOME

6.4 CHALLENGES

6.4.1 LACK OF SKILLED EXPERTISE

6.4.2 STRINGENT REGULATIONS

7 NORTH AMERICA MEDICAL DISPLAY MARKET, BY TECHNOLOGY

7.1 OVERVIEW

7.2 LED BACKLIT LCD DISPLAY

7.3 CCFL BACKLIT LCD DISPLAY

7.4 TFT BACKLIT LCD DISPLAY

7.5 OLED DISPLAY

7.5.1 AMOLED

7.5.2 PMOLED

8 NORTH AMERICA MEDICAL DISPLAY MARKET, BY PANEL SIZE

8.1 OVERVIEW

8.2 LESS THAN 22.9

8.2.1 LED BACKLIT LCD DISPLAY

8.2.2 CCFL BACKLIT LCD DISPLAY

8.2.3 TFT BACKLIT LCD DISPLAY

8.2.4 OLED DISPLAY

8.3 23.0- 32.0

8.3.1 LED BACKLIT LCD DISPLAY

8.3.2 CCFL BACKLIT LCD DISPLAY

8.3.3 TFT BACKLIT LCD DISPLAY

8.3.4 OLED DISPLAY

8.4 32.1-42.0

8.4.1 LED BACKLIT LCD DISPLAY

8.4.2 CCFL BACKLIT LCD DISPLAY

8.4.3 TFT BACKLIT LCD DISPLAY

8.4.4 OLED DISPLAY

8.5 MORE THAN 42

8.5.1 LED BACKLIT LCD DISPLAY

8.5.2 CCFL BACKLIT LCD DISPLAY

8.5.3 TFT BACKLIT LCD DISPLAY

8.5.4 OLED DISPLAY

9 NORTH AMERICA MEDICAL DISPLAY MARKET, BY VIEWING MODE

9.1 OVERVIEW

9.2 2D

9.3 3D

10 NORTH AMERICA MEDICAL DISPLAY MARKET, BY MEGAPIXEL

10.1 OVERVIEW

10.2 2.1-4MP

10.3 4.1-8MP

10.4 ABOVE 8MP

10.5 UPTO 2MP

11 NORTH AMERICA MEDICAL DISPLAY MARKET, BY RESOLUTION

11.1 OVERVIEW

11.2 4K

11.3 ULTRA FULL HD

11.4 FULL HD

11.5 OTHERS

12 NORTH AMERICA MEDICAL DISPLAY MARKET, BY DISPLAY TYPE

12.1 OVERVIEW

12.2 WALL MOUNTED

12.3 PORTABLE

12.4 MODULAR

13 NORTH AMERICA MEDICAL DISPLAY MARKET, BY DISPLAY COLOR

13.1 OVERVIEW

13.2 COLOR

13.2.1 LED BACKLIT LCD DISPLAY

13.2.2 CCFL BACKLIT LCD DISPLAY

13.2.3 TFT BACKLIT LCD DISPLAY

13.2.4 OLED DISPLAY

13.3 MONOCHROME

13.3.1 LED BACKLIT LCD DISPLAY

13.3.2 CCFL BACKLIT LCD DISPLAY

13.3.3 TFT BACKLIT LCD DISPLAY

13.3.4 OLED DISPLAY

14 NORTH AMERICA MEDICAL DISPLAY MARKET, BY COMPONENT

14.1 OVERVIEW

14.2 HARDWARE

14.2.1 ACCESSORIES

14.2.2 SENSORS

14.2.3 PANELS

14.2.4 OTHERS

14.3 SERVICES

14.3.1 CONSULTING

14.3.2 INSTALLATION

14.3.3 AFTER-SALE SERVICES

15 NORTH AMERICA MEDICAL DISPLAY MARKET, BY APPLICATION

15.1 OVERVIEW

15.2 DIAGNOSTICS

15.2.1 BY TYPE

15.2.1.1 GENERAL RADIOLOGY

15.2.1.2 MAMMOGRAPHY

15.2.1.3 DIGITAL PATHOLOGY

15.2.1.4 MULTI-MODALITY

15.2.2 BY PANEL SIZE

15.2.2.1 LESS THAN 22.9

15.2.2.2 23.0- 32.0

15.2.2.3 32.1-42.0

15.2.2.4 MORE THAN 42

15.3 SURGICAL/INTERVENTIONAL

15.3.1 BY TYPE

15.3.1.1 CARDIOVASCULAR

15.3.1.2 ONCOLOGY

15.3.1.3 NEUROLOGY

15.3.1.4 OPHTHALMOLOGY

15.3.1.5 OTHERS

15.3.2 BY PANEL SIZE

15.3.2.1 LESS THAN 22.9

15.3.2.2 23.0- 32.0

15.3.2.3 32.1-42.0

15.3.2.4 MORE THAN 42

15.4 PATIENT WORN MONITORING

15.5 CONSULTATION

15.6 TELEHEALTH

15.6.1 BY PANEL SIZE

15.6.1.1 LESS THAN 22.9

15.6.1.2 23.0- 32.0

15.6.1.3 32.1-42.0

15.6.1.4 MORE THAN 42

15.7 TEACHING/PRACTICE

15.7.1 BY PANEL SIZE

15.7.1.1 LESS THAN 22.9

15.7.1.2 23.0- 32.0

15.7.1.3 32.1-42.0

15.7.1.4 MORE THAN 42

15.8 DENTISTRY

15.8.1 BY PANEL SIZE

15.8.1.1 LESS THAN 22.9

15.8.1.2 23.0- 32.0

15.8.1.3 32.1-42.0

15.8.1.4 MORE THAN 42

15.9 POINT OF CARE

15.9.1 BY PANEL SIZE

15.9.1.1 LESS THAN 22.9

15.9.1.2 23.0- 32.0

15.9.1.3 32.1-42.0

15.9.1.4 MORE THAN 42

15.1 FETAL MONITORING

15.10.1 BY PANEL SIZE

15.10.1.1 LESS THAN 22.9

15.10.1.2 23.0- 32.0

15.10.1.3 32.1-42.0

15.10.1.4 MORE THAN 42

15.11 OTHERS

16 NORTH AMERICA MEDICAL DISPLAY MARKET, BY END USER

16.1 OVERVIEW

16.2 HOSPITALS

16.2.1 BY AREA

16.2.1.1 OPERATING ROOM

16.2.1.2 SURGERY UNIT

16.2.1.3 OTHERS

16.2.2 BY TECHNOLOGY

16.2.2.1 LED BACKLIT LCD DISPLAY

16.2.2.2 CCFL BACKLIT LCD DISPLAY

16.2.2.3 TFT BACKLIT LCD DISPLAY

16.2.2.4 OLED DISPLAY

16.2.3 CLINICS

16.2.3.1 LED BACKLIT LCD DISPLAY

16.2.3.2 CCFL BACKLIT LCD DISPLAY

16.2.3.3 TFT BACKLIT LCD DISPLAY

16.2.3.4 OLED DISPLAY

16.2.4 NURSING FACILITIES

16.2.4.1 LED BACKLIT LCD DISPLAY

16.2.4.2 CCFL BACKLIT LCD DISPLAY

16.2.4.3 TFT BACKLIT LCD DISPLAY

16.2.4.4 OLED DISPLAY

16.2.5 DIAGNOSTIC LABORATORIES

16.2.5.1 LED BACKLIT LCD DISPLAY

16.2.5.2 CCFL BACKLIT LCD DISPLAY

16.2.5.3 TFT BACKLIT LCD DISPLAY

16.2.5.4 OLED DISPLAY

16.3 IMAGING/ RADIOLOGY LABORATORY

16.3.1 LABORATORY

16.3.1.1 LED BACKLIT LCD DISPLAY

16.3.1.2 CCFL BACKLIT LCD DISPLAY

16.3.1.3 TFT BACKLIT LCD DISPLAY

16.3.1.4 OLED DISPLAY

16.3.2 REHABILITATION CENTERS

16.3.2.1 LED BACKLIT LCD DISPLAY

16.3.2.2 CCFL BACKLIT LCD DISPLAY

16.3.2.3 TFT BACKLIT LCD DISPLAY

16.3.2.4 OLED DISPLAY

16.4 OTHERS

17 NORTH AMERICA MEDICAL DISPLAY MARKET, BY IMAGING TECHNOLOGY

17.1 OVERVIEW

17.2 TOUCH SCREEN

17.3 SCRATCH RESISTANT FONT GLASS

17.4 FAILSAFE MODE

17.5 CLEANABLE OPTIONS

17.6 SOFTGLOW & SPOTVIEW

17.7 OTHERS

18 NORTH AMERICA MEDICAL DISPLAY MARKET, BY ASPECT RATIO

18.1 OVERVIEW

18.2 12/30/1899 4:09:00 PM

18.3 12/30/1899 9:09:00 PM

18.4 12/30/1899 4:03:00 AM

19 NORTH AMERICA MEDICAL DISPLAY MARKET, BY DISTRIBUTION CHANNEL

19.1 OVERVIEW

19.2 DIRECT TENDERS

19.3 RETAIL SALES

19.4 OTHERS

20 NORTH AMERICA MEDICAL DISPLAY MARKET, BY GEOGRAPHY

20.1 NORTH AMERICA

20.1.1 U.S.

20.1.2 CANADA

20.1.3 MEXICO

21 NORTH AMERICA MEDICAL DISPLAY MARKET: COMPANY LANDSCAPE

21.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

22 SWOT ANALYSIS

23 COMPANY PROFILE

23.1 ADVANTECH CO., LTD

23.1.1 COMPANY SNAPSHOT

23.1.2 REVENUE ANALYSIS

23.1.3 COMPANY SHARE ANALYSIS

23.1.4 PRODUCT PORTFOLIO

23.1.5 RECENT DEVELOPMENTS

23.2 HP DEVELOPMENT COMPANY, L.P

23.2.1 COMPANY SNAPSHOT

23.2.2 REVENUE ANALYSIS

23.2.3 COMPANY SHARE ANALYSIS

23.2.4 PRODUCT PORTFOLIO

23.2.5 RECENT DEVELOPMENT

23.3 DELL INC.

23.3.1 COMPANY SNAPSHOT

23.3.2 REVENUE ANALYSIS

23.3.3 COMPANY SHARE ANALYSIS

23.3.4 PRODUCT PORTFOLIO

23.3.5 RECENT DEVELOPMENTS

23.4 ALPINION MEDICAL SYSTEMS CO., LTD

23.4.1 COMPANY SNAPSHOT

23.4.2 COMPANY SHARE ANALYSIS

23.4.3 PRODUCT PORTFOLIO

23.4.4 RECENT DEVELOPMENTS

23.5 STERIS

23.5.1 COMPANY SNAPSHOT

23.5.2 REVENUE ANALYSIS

23.5.3 COMPANY SHARE ANALYSIS

23.5.4 PRODUCT PORTFOLIO

23.5.5 RECENT DEVELOPMENT

23.6 AMPRONIX

23.6.1 COMPANY SNAPSHOT

23.6.2 PRODUCT PORTFOLIO

23.6.3 RECENT DEVELOPMENT

23.7 AXIOMTEK CO., LTD.

23.7.1 COMPANY SNAPSHOT

23.7.2 REVENUE ANALYSIS

23.7.3 PRODUCT PORTFOLIO

23.7.4 RECENT DEVELOPMENT

23.8 BARCO

23.8.1 COMPANY SNAPSHOT

23.8.2 REVENUE ANALYSIS

23.8.3 PRODUCT PORTFOLIO

23.8.4 RECENT DEVELOPMENTS

23.9 BENQ

23.9.1 COMPANY SNAPSHOT

23.9.2 PRODUCT PORTFOLIO

23.9.3 RECENT DEVELOPMENTS

23.1 COJE CO., LTD.

23.10.1 COMPANY SNAPSHOT

23.10.2 PRODUCT PORTFOLIO

23.10.3 RECENT DEVELOPMENTS

23.11 EIZO INC (2021)

23.11.1 COMPANY SNAPSHOT

23.11.2 REVENUE ANALYSIS

23.11.3 PRODUCT PORTFOLIO

23.11.4 RECENT DEVELOPMENT

23.12 FSN MEDICAL TECHNOLOGIES.

23.12.1 COMPANY SNAPSHOT

23.12.2 PRODUCT PORTFOLIO

23.12.3 RECENT DEVELOPMENT

23.13 HISENSE MEDICAL EQUIPMENT CO, LTD (A SUBSIDIARY OF HISENSE GROUP)

23.13.1 COMPANY SNAPSHOT

23.13.2 REVENUE ANALYSIS

23.13.3 PRODUCT PORTFOLIO

23.13.4 RECENT DEVELOPMENT

23.14 KONINKLIJKE PHILIPS N.V.( 2021)

23.14.1 COMPANY SNAPSHOT

23.14.2 REVENUE ANALYSIS

23.14.3 PRODUCT PORTFOLIO

23.14.4 RECENT DEVELOPMENT

23.15 LG DISPLAY CO., LTD.

23.15.1 COMPANY SNAPSHOT

23.15.2 REVENUE ANALYSIS

23.15.3 PRODUCT PORTFOLIO

23.15.4 RECENT DEVELOPMENT

23.16 NANJING JUSHA COMMERCIAL &TRADING CO,LTD

23.16.1 COMPANY SNAPSHOT

23.16.2 PRODUCT PORTFOLIO

23.16.3 RECENT DEVELOPMENTS

23.17 NOVANTA INC. (2021)

23.17.1 COMPANY SNAPSHOT

23.17.2 REVENUE ANALYSIS

23.17.3 PRODUCT PORTFOLIO

23.17.4 RECENT DEVELOPMENTS

23.18 ONYX HEALTHCARE INC. (SUBSIDIARY OF AAEON TECHNOLOGY INC.)

23.18.1 COMPANY SNAPSHOT

23.18.2 REVENUE ANALYSIS

23.18.3 PRODUCT PORTFOLIO

23.18.4 RECENT DEVELOPMENTS

23.19 PANASONIC HOLDINGS CORPORATION

23.19.1 COMPANY SNAPSHOT

23.19.2 REVENUE ANALYSIS

23.19.3 RECENT DEVELOPMENT

23.2 QUEST MEDICAL, INC. (A SUBSIDIARY OF ATRION CORPORATION)

23.20.1 COMPANY SNAPSHOT

23.20.2 REVENUE ANALYSIS

23.20.3 PRODUCT PORTFOLIO

23.20.4 RECENT DEVELOPMENTS

23.21 REIN MEDICAL GMBH

23.21.1 COMPANY SNAPSHOT

23.21.2 PRODUCT PORTFOLIO

23.21.3 RECENT DEVELOPMENTS

23.22 SHARP NEC DISPLAY SOLUTIONS ( 2021)

23.22.1 COMPANY SNAPSHOT

23.22.2 PRODUCT PORTFOLIO

23.22.3 RECENT DEVELOPMENTS

23.23 SHENZHEN BEACON DISPLAY TECHNOLOGY CO., LTD.

23.23.1 COMPANY SNAPSHOT

23.23.2 PRODUCT PORTFOLIO

23.23.3 RECENT DEVELOPMENT

23.24 SHENZHEN JLD DISPLAY EXPERT CO., LTD

23.24.1 COMPANY SNAPSHOT

23.24.2 PRODUCT PORTFOLIO

23.24.3 RECENT DEVELOPMENTS

23.25 SIEMENS HEALTHCARE GMBH

23.25.1 COMPANY SNAPSHOT

23.25.2 REVENUE ANALYSIS

23.25.3 PRODUCT PORTFOLIO

23.25.4 RECENT DEVELOPMENT

23.26 SONY GROUP CORPORATION

23.26.1 COMPANY SNAPSHOT

23.26.2 REVENUE ANALYSIS

23.26.3 PRODUCT PORTFOLIO

23.26.4 RECENT DEVELOPMENT

23.27 TEGUAR COMPUTERS

23.27.1 COMPANY SNAPSHOT

23.27.2 PRODUCT PORTFOLIO

23.27.3 RECENT DEVELOPMENTS

24 QUESTIONNAIRE

25 RELATED REPORTS

Liste des tableaux

TABLE 1 NORTH AMERICA MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 2 NORTH AMERICA LED BACKLIT LCD DISPLAY MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 3 NORTH AMERICA CCFL BACKLIT LCD DISPLAY IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 4 NORTH AMERICA TFT BACKLIT LCD DISPLAY IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 5 NORTH AMERICA OLED DISPLAY IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 6 NORTH AMERICA OLED DISPLAY TYPE IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 7 NORTH AMERICA MEDICAL DISPLAY MARKET, BY PANEL SIZE, 2020-2029 (USD MILLION)

TABLE 8 NORTH AMERICA LESS THAN 22.9 IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 9 NORTH AMERICA LESS THAN 22.9 IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 10 NORTH AMERICA 23.0- 32.0 IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 11 NORTH AMERICA 23.0- 32.0 IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 12 NORTH AMERICA 32.1-42.0 IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 13 NORTH AMERICA 32.1-40.0 IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 14 NORTH AMERICA MORE THAN 42 IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 15 NORTH AMERICA MORE THAN 42 IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 16 NORTH AMERICA MEDICAL DISPLAY MARKET, BY VIEWING MODE, 2020-2029 (USD MILLION)

TABLE 17 NORTH AMERICA 2D IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 18 NORTH AMERICA 3D IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 19 NORTH AMERICA MEDICAL DISPLAY MARKET, BY MEGAPIXEL, 2020-2029 (USD MILLION)

TABLE 20 NORTH AMERICA 2.1-4MP IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 21 NORTH AMERICA 4.1-8MP IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 22 NORTH AMERICA ABOVE 8MP IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 23 NORTH AMERICA UPTO 2MP IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 24 NORTH AMERICA MEDICAL DISPLAY MARKET, BY RESOLUTION, 2020-2029 (USD MILLION)

TABLE 25 NORTH AMERICA 4K IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 26 NORTH AMERICA ULTRA FULL HD IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 27 NORTH AMERICA FULL HD IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 28 NORTH AMERICA OTHERS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 29 NORTH AMERICA MEDICAL DISPLAY MARKET, BY DISPLAY TYPE, 2020-2029 (USD MILLION)

TABLE 30 NORTH AMERICA WALL MOUNTED IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 31 NORTH AMERICA PORTABLE IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 32 NORTH AMERICA MODULAR IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 33 NORTH AMERICA MEDICAL DISPLAY MARKET, BY DISPLAY COLOR, 2020-2029 (USD MILLION)

TABLE 34 NORTH AMERICA COLOR IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 35 NORTH AMERICA COLOR IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 36 NORTH AMERICA MONOCHROME IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 37 NORTH AMERICA MONOCHROME IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 38 NORTH AMERICA MEDICAL DISPLAY MARKET, BY COMPONENT, 2020-2029 (USD MILLION)

TABLE 39 NORTH AMERICA HARDWARE IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 40 NORTH AMERICA HARDWARE IN MEDICAL DISPLAY MARKET, BY COMPONENT, 2020-2029 (USD MILLION)

TABLE 41 NORTH AMERICA SERVICES IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 42 NORTH AMERICA SERVICES IN MEDICAL DISPLAY MARKET, BY COMPONENT, 2020-2029 (USD MILLION)

TABLE 43 NORTH AMERICA MEDICAL DISPLAY MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 44 NORTH AMERICA DIAGNOSTICS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 45 NORTH AMERICA DIAGNOSTICS IN MEDICAL DISPLAY MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 46 NORTH AMERICA BY TYPE IN MEDICAL DISPLAY MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 47 NORTH AMERICA BY PANEL SIZE IN MEDICAL DISPLAY MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 48 NORTH AMERICA SURGICAL/INTERVENTIONAL IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 49 NORTH AMERICA SURGICAL/INTERVENTIONAL IN MEDICAL DISPLAY MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 50 NORTH AMERICA BY TYPE IN MEDICAL DISPLAY MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 51 NORTH AMERICA BY PANEL SIZE IN MEDICAL DISPLAY MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 52 NORTH AMERICA PATIENT WORN MONITORING IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 53 NORTH AMERICA CONSULTATION IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 54 NORTH AMERICA TELEHEALTH IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 55 NORTH AMERICA TELEHEALTH IN MEDICAL DISPLAY MARKET, BY PANEL SIZE, 2020-2029 (USD MILLION)

TABLE 56 NORTH AMERICA TEACHING/PRACTICE IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 57 NORTH AMERICA TEACHING/PRACTICE IN MEDICAL DISPLAY MARKET, BY PANEL SIZE, 2020-2029 (USD MILLION)

TABLE 58 NORTH AMERICA DENTISTRY IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 59 NORTH AMERICA DENTISTRY IN MEDICAL DISPLAY MARKET, BY PANEL SIZE, 2020-2029 (USD MILLION)

TABLE 60 NORTH AMERICA POINT OF CARE IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 61 NORTH AMERICA POINT OF CARE IN MEDICAL DISPLAY MARKET, BY PANEL SIZE, 2020-2029 (USD MILLION)

TABLE 62 NORTH AMERICA FETAL MONITORING IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 63 NORTH AMERICA FETAL MONITORING IN MEDICAL DISPLAY MARKET, BY PANEL SIZE, 2020-2029 (USD MILLION)

TABLE 64 NORTH AMERICA OTHERS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 65 NORTH AMERICA MEDICAL DISPLAY MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 66 NORTH AMERICA HOSPITALS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 67 NORTH AMERICA HOSPITALS IN MEDICAL DISPLAY MARKET, BY END USERS, 2020-2029 (USD MILLION)

TABLE 68 NORTH AMERICA BY AREA IN MEDICAL DISPLAY MARKET, BY END USERS, 2020-2029 (USD MILLION)

TABLE 69 NORTH AMERICA BY TECHNOLOGY IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 70 NORTH AMERICA CLINICS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 71 NORTH AMERICA CLINICS IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 72 NORTH AMERICA NURSING FACILITIES IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 73 NORTH AMERICA NURSING FACILITIES IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 74 NORTH AMERICA DIAGNOSTIC LABORATORIES IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 75 NORTH AMERICA DIAGNOSTIC LABORATORIES IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 76 NORTH AMERICA IMAGING/ RADIOLOGY LABORATORY IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 77 NORTH AMERICA LABORATORY IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 78 NORTH AMERICA LABORATORY IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 79 NORTH AMERICA REHABILITATION CENTERS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 80 NORTH AMERICA REHABILITATION CENTERS IN MEDICAL DISPLAY MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 81 NORTH AMERICA OTHERS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 82 NORTH AMERICA MEDICAL DISPLAY MARKET, BY IMAGING TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 83 NORTH AMERICA TOUCH SCREEN IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 84 NORTH AMERICA SCRATCH RESISTANT FONT GLASS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 85 NORTH AMERICA FAILSAFE MODE IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 86 NORTH AMERICA CLEANABLE OPTIONS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 87 NORTH AMERICA SOFTGLOW & SPOTVIEW IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 88 NORTH AMERICA OTHERS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 89 NORTH AMERICA MEDICAL DISPLAY MARKET, BY ASPECT RATIO, 2020-2029 (USD MILLION)

TABLE 90 NORTH AMERICA 16:09 IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 91 NORTH AMERICA 21:09 IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 92 NORTH AMERICA 4:03 IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 93 NORTH AMERICA MEDICAL DISPLAY MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 94 NORTH AMERICA DIRECT TENDERS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 95 NORTH AMERICA RETAIL SALES IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 96 NORTH AMERICA OTHERS IN MEDICAL DISPLAY MARKET, BY REGION, 2020-2029 (USD MILLION)

Liste des figures

FIGURE 1 NORTH AMERICA MEDICAL DISPLAYMARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA MEDICAL DISPLAYMARKET : DATA TRIANGULATION

FIGURE 3 NORTH AMERICA MEDICAL DISPLAYMARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA MEDICAL DISPLAYMARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA MEDICAL DISPLAYMARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA MEDICAL DISPLAYMARKET: MULTIVARIATE MODELLING

FIGURE 7 NORTH AMERICA MEDICAL DISPLAYMARKET: INTERVIEW DEMOGRAPHICS

FIGURE 8 NORTH AMERICA MEDICAL DISPLAYMARKET: DBMR MARKET POSITION GRID

FIGURE 9 NORTH AMERICA MEDICAL DISPLAYMARKET: MARKET APPLICATION COVERAGE GRID

FIGURE 10 NORTH AMERICA MEDICAL DISPLAYMARKET: VENDOR SHARE ANALYSIS

FIGURE 11 NORTH AMERICA MEDICAL DISPLAY MARKET: SEGMENTATION

FIGURE 12 RISE IN GENERIC DRUG PRODUCTION AND TECHNOLOGICAL FOCUS IN MEDICAL DISPLAYIS DRIVING THE NORTH AMERICA MEDICAL DISPLAYMARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 13 TECHNOLOGYSEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA MEDICAL DISPLAYMARKET IN 2022 & 2029

FIGURE 14 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE NORTH AMERICA MEDICAL DISPLAY MARKET

FIGURE 15 NORTH AMERICA MEDICAL DISPLAY MARKET : BY TECHNOLOGY, 2021

FIGURE 16 NORTH AMERICA MEDICAL DISPLAY MARKET : BY TECHNOLOGY, 2022-2029 (USD MILLION)

FIGURE 17 NORTH AMERICA MEDICAL DISPLAY MARKET : BY TECHNOLOGY, CAGR (2022-2029)

FIGURE 18 NORTH AMERICA MEDICAL DISPLAY MARKET : BY TECHNOLOGY, LIFELINE CURVE

FIGURE 19 NORTH AMERICA MEDICAL DISPLAY MARKET : BY PANEL SIZE, 2021

FIGURE 20 NORTH AMERICA MEDICAL DISPLAY MARKET : BY PANEL SIZE, 2022-2029 (USD MILLION)

FIGURE 21 NORTH AMERICA MEDICAL DISPLAY MARKET : BY PANEL SIZE, CAGR (2022-2029)

FIGURE 22 NORTH AMERICA MEDICAL DISPLAY MARKET : BY PANEL SIZE, LIFELINE CURVE

FIGURE 23 NORTH AMERICA MEDICAL DISPLAY MARKET : BY VIEWING MODE, 2021

FIGURE 24 NORTH AMERICA MEDICAL DISPLAY MARKET : BY VIEWING MODE, 2022-2029 (USD MILLION)

FIGURE 25 NORTH AMERICA MEDICAL DISPLAY MARKET : BY VIEWING MODE, CAGR (2022-2029)

FIGURE 26 NORTH AMERICA MEDICAL DISPLAY MARKET : BY VIEWING MODE, LIFELINE CURVE

FIGURE 27 NORTH AMERICA MEDICAL DISPLAY MARKET : BY MEGAPIXEL, 2021

FIGURE 28 NORTH AMERICA MEDICAL DISPLAY MARKET : BY MEGAPIXEL, 2022-2029 (USD MILLION)

FIGURE 29 NORTH AMERICA MEDICAL DISPLAY MARKET : BY MEGAPIXEL, CAGR (2022-2029)

FIGURE 30 NORTH AMERICA MEDICAL DISPLAY MARKET : BY MEGAPIXEL, LIFELINE CURVE

FIGURE 31 NORTH AMERICA MEDICAL DISPLAY MARKET : BY RESOLUTION, 2021

FIGURE 32 NORTH AMERICA MEDICAL DISPLAY MARKET : BY RESOLUTION, 2022-2029 (USD MILLION)

FIGURE 33 NORTH AMERICA MEDICAL DISPLAY MARKET : BY RESOLUTION, CAGR (2022-2029)

FIGURE 34 NORTH AMERICA MEDICAL DISPLAY MARKET : BY RESOLUTION, LIFELINE CURVE

FIGURE 35 NORTH AMERICA MEDICAL DISPLAY MARKET : BY DISPLAY TYPE, 2021

FIGURE 36 NORTH AMERICA MEDICAL DISPLAY MARKET : BY DISPLAY TYPE, 2022-2029 (USD MILLION)

FIGURE 37 NORTH AMERICA MEDICAL DISPLAY MARKET : BY DISPLAY TYPE, CAGR (2022-2029)

FIGURE 38 NORTH AMERICA MEDICAL DISPLAY MARKET : BY DISPLAY TYPE, LIFELINE CURVE

FIGURE 39 NORTH AMERICA MEDICAL DISPLAY MARKET : BY DISPLAY COLOR, 2021

FIGURE 40 NORTH AMERICA MEDICAL DISPLAY MARKET : BY DISPLAY COLOR, 2022-2029 (USD MILLION)

FIGURE 41 NORTH AMERICA MEDICAL DISPLAY MARKET : BY DISPLAY COLOR, CAGR (2022-2029)

FIGURE 42 NORTH AMERICA MEDICAL DISPLAY MARKET : BY DISPLAY COLOR, LIFELINE CURVE

FIGURE 43 NORTH AMERICA MEDICAL DISPLAY MARKET : BY COMPONENT, 2021

FIGURE 44 NORTH AMERICA MEDICAL DISPLAY MARKET : BY COMPONENT, 2022-2029 (USD MILLION)

FIGURE 45 NORTH AMERICA MEDICAL DISPLAY MARKET : BY COMPONENT, CAGR (2022-2029)

FIGURE 46 NORTH AMERICA MEDICAL DISPLAY MARKET : BY COMPONENT, LIFELINE CURVE

FIGURE 47 NORTH AMERICA MEDICAL DISPLAY MARKET: BY APPLICATION, 2021

FIGURE 48 NORTH AMERICA MEDICAL DISPLAY MARKET: BY APPLICATION, 2022-2029 (USD MILLION)

FIGURE 49 NORTH AMERICA MEDICAL DISPLAY MARKET: BY APPLICATION, CAGR (2022-2029)

FIGURE 50 NORTH AMERICA MEDICAL DISPLAY MARKET: BY APPLICATION, LIFELINE CURVE

FIGURE 51 NORTH AMERICA MEDICAL DISPLAY MARKET: BY END USER, 2021

FIGURE 52 NORTH AMERICA MEDICAL DISPLAY MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 53 NORTH AMERICA MEDICAL DISPLAY MARKET: BY END USER, CAGR (2022-2029)

FIGURE 54 NORTH AMERICA MEDICAL DISPLAY MARKET: BY END USER, LIFELINE CURVE

FIGURE 55 NORTH AMERICA MEDICAL DISPLAY MARKET: BY IMAGING TECHNOLOGY, 2021

FIGURE 56 NORTH AMERICA MEDICAL DISPLAY MARKET: BY IMAGING TECHNOLOGY, 2022-2029 (USD MILLION)

FIGURE 57 NORTH AMERICA MEDICAL DISPLAY MARKET: BY IMAGING TECHNOLOGY, CAGR (2022-2029)

FIGURE 58 NORTH AMERICA MEDICAL DISPLAY MARKET: BY IMAGING TECHNOLOGY, LIFELINE CURVE

FIGURE 59 NORTH AMERICA MEDICAL DISPLAY MARKET: BY ASPECT RATIO, 2021

FIGURE 60 NORTH AMERICA MEDICAL DISPLAY MARKET: BY ASPECT RATIO, 2022-2029 (USD MILLION)

FIGURE 61 NORTH AMERICA MEDICAL DISPLAY MARKET: BY ASPECT RATIO, CAGR (2022-2029)

FIGURE 62 NORTH AMERICA MEDICAL DISPLAY MARKET: BY ASPECT RATIO, LIFELINE CURVE

FIGURE 63 NORTH AMERICA MEDICAL DISPLAY MARKET: BY DISTRIBUTION CHANNEL, 2021

FIGURE 64 NORTH AMERICA MEDICAL DISPLAY MARKET: BY DISTRIBUTION CHANNEL, 2022-2029 (USD MILLION)

FIGURE 65 NORTH AMERICA MEDICAL DISPLAY MARKET: BY DISTRIBUTION CHANNEL, CAGR (2022-2029)

FIGURE 66 NORTH AMERICA MEDICAL DISPLAY MARKET: BY DISTRIBUTION CHANNEL, LIFELINE CURVE

FIGURE 67 NORTH AMERICA MEDICAL DISPLAY MARKET: SNAPSHOT (2021)

FIGURE 68 NORTH AMERICA MEDICAL DISPLAY MARKET: BY COUNTRY (2021)

FIGURE 69 NORTH AMERICA MEDICAL DISPLAY MARKET: BY COUNTRY (2022 & 2029)

FIGURE 70 NORTH AMERICA MEDICAL DISPLAY MARKET: BY COUNTRY (2021 & 2029)

FIGURE 71 NORTH AMERICA MEDICAL DISPLAY MARKET: BY TECHNOLOGY (2022-2029)

FIGURE 72 NORTH AMERICA MEDICAL DISPLAY MARKET: COMPANY SHARE 2021 (%)

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.