Global Medical Equipment Maintenance Market

Taille du marché en milliards USD

TCAC :

%

USD

28.31 Billion

USD

58.09 Billion

2024

2032

USD

28.31 Billion

USD

58.09 Billion

2024

2032

| 2025 –2032 | |

| USD 28.31 Billion | |

| USD 58.09 Billion | |

| % | |

|

Segmentation du marché mondial de la maintenance des équipements médicaux, par type de service (préventif, correctif et performance/opérationnel), fournisseurs de services (fournisseurs de services internes et fournisseurs de services externes), type d'appareil (équipement d'imagerie, appareils endoscopiques, équipements électromédicaux, instruments chirurgicaux, dispositifs de surveillance et de maintien des fonctions vitales des patients, équipements dentaires et autres équipements médicaux), niveau de maintenance (niveau 3, spécialisé, niveau 2, technicien, niveau 1 et utilisateur (ou de première ligne)), technologie (OEM multifournisseurs, OEM monofournisseurs, organisation de services indépendante et maintenance interne), utilisateur final (hôpitaux, cliniques, laboratoires et autres centres de soins de santé) - Tendances et prévisions de l'industrie jusqu'en 2031

Analyse du marché de la maintenance des équipements médicaux

Le marché de la maintenance des équipements médicaux est crucial pour garantir la fonctionnalité et la longévité des dispositifs de santé essentiels. Ce marché englobe les services d'entretien, de réparation et de support de divers équipements médicaux, notamment les appareils d'imagerie , les instruments chirurgicaux et les systèmes de surveillance des patients . La prévalence croissante des maladies chroniques et la demande croissante de technologies médicales avancées sont des facteurs clés qui propulsent la croissance du marché. En outre, la pandémie de COVID-19 a souligné l'importance de la fiabilité des équipements, ce qui a conduit à une augmentation des investissements dans les services de maintenance. Les développements récents incluent des innovations en matière de maintenance prédictive alimentées par l'intelligence artificielle , permettant aux établissements de santé d'optimiser la gestion de leurs équipements et de réduire les temps d'arrêt. Alors que les prestataires de soins de santé s'efforcent d'améliorer l'efficacité opérationnelle et les résultats des patients, le marché de la maintenance des équipements médicaux est sur le point de poursuivre sa croissance, tirée par les avancées technologiques et l'accent mis sur la qualité des soins.

Taille du marché de la maintenance des équipements médicaux

Français La taille du marché mondial de la maintenance des équipements médicaux était évaluée à 25,88 milliards USD en 2023 et devrait atteindre 53,11 milliards USD d'ici 2031, avec un TCAC de 9,40 % au cours de la période de prévision de 2024 à 2031. En plus des informations sur les scénarios de marché tels que la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux acteurs, les rapports de marché organisés par Data Bridge Market Research comprennent également une analyse approfondie des experts, l'épidémiologie des patients, l'analyse du pipeline, l'analyse des prix et le cadre réglementaire.

Tendances du marché de la maintenance des équipements médicaux

« Adoption de la maintenance prédictive »

Le marché de la maintenance des équipements médicaux connaît des tendances importantes, portées par les progrès technologiques et l’évolution des besoins des prestataires de soins de santé. L’une des principales tendances est l’adoption croissante de la maintenance prédictive, qui s’appuie sur l’analyse des données et les appareils IoT pour anticiper les pannes d’équipement avant qu’elles ne surviennent. Cette innovation minimise les temps d’arrêt et réduit les coûts de maintenance, améliorant ainsi l’efficacité opérationnelle dans les établissements de santé. En outre, la demande croissante de technologies médicales avancées nécessite des solutions de maintenance plus sophistiquées. Alors que les établissements de santé accordent la priorité à la fiabilité et aux performances des équipements, l’accent mis sur les stratégies de maintenance proactive continuera de façonner le marché. Dans l’ensemble, ces tendances soulignent l’importance d’intégrer la technologie moderne dans les pratiques de maintenance pour garantir une fonctionnalité et des soins aux patients optimaux.

Portée du rapport et segmentation du marché de la maintenance des équipements médicaux

|

Attributs |

Informations clés sur le marché de la maintenance des équipements médicaux |

|

Segments couverts |

|

|

Pays couverts |

États-Unis, Canada et Mexique en Amérique du Nord, Allemagne, France, Royaume-Uni, Pays-Bas, Suisse, Belgique, Russie, Italie, Espagne, Turquie, Reste de l'Europe en Europe, Chine, Japon, Inde, Corée du Sud, Singapour, Malaisie, Australie, Thaïlande, Indonésie, Philippines, Reste de l'Asie-Pacifique (APAC) en Asie-Pacifique (APAC), Arabie saoudite, Émirats arabes unis, Afrique du Sud, Égypte, Israël, Reste du Moyen-Orient et de l'Afrique (MEA) en tant que partie du Moyen-Orient et de l'Afrique (MEA), Brésil, Argentine et Reste de l'Amérique du Sud en tant que partie de l'Amérique du Sud. |

|

Principaux acteurs du marché |

Koninklijke Philips NV (Pays-Bas), Siemens Healthineers AG (Allemagne), General Electric Company (États-Unis), Medtronic (Irlande), TeraRecon (États-Unis), Carestream Health (États-Unis), Shimadzu Corporation (Japon), Olympus Corporation (Japon), Boston Scientific Corporation (États-Unis), Cook (États-Unis), Hoya Corporation (Japon), Richard Wolf GmbH (Allemagne), KARL STORZ (Allemagne), Smith+Nephew (Royaume-Uni), Zimmer Biomet (États-Unis) |

|

Opportunités de marché |

|

|

Ensembles d'informations sur les données à valeur ajoutée |

Outre les informations sur les scénarios de marché tels que la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux acteurs, les rapports de marché organisés par Data Bridge Market Research comprennent également une analyse approfondie des experts, une épidémiologie des patients, une analyse du pipeline, une analyse des prix et un cadre réglementaire. |

Définition du marché de la maintenance des équipements médicaux

La maintenance des équipements médicaux désigne le processus systématique visant à garantir que les dispositifs et équipements médicaux fonctionnent efficacement et en toute sécurité tout au long de leur durée de vie opérationnelle. Cela comprend une série d'activités, telles que les inspections de routine, la maintenance préventive, l'étalonnage, les réparations et les mises à jour logicielles. Une maintenance efficace est essentielle pour se conformer aux normes réglementaires, réduire le risque de défaillance des équipements et garantir des performances optimales dans les environnements cliniques.

Dynamique du marché de la maintenance des équipements médicaux

Conducteurs

- Croissance de l'utilisation des équipements de diagnostic et d'imagerie

L'utilisation croissante d'appareils de diagnostic tels que les appareils d'IRM, de tomodensitométrie et de radiographie stimule considérablement la demande de services de maintenance sur le marché des équipements médicaux. Ces appareils sont essentiels pour un diagnostic précis et une planification du traitement, ce qui rend leur fonctionnement continu et efficace essentiel pour les prestataires de soins de santé. Avec l'incidence croissante des maladies chroniques et le vieillissement croissant de la population, on s'appuie de plus en plus sur l'imagerie diagnostique pour la détection et la surveillance précoces des maladies. Comme ces machines sont sophistiquées et nécessitent un entretien régulier pour garantir la précision et éviter les pannes coûteuses, les établissements de santé accordent la priorité à leur maintenance. La base d'installation croissante d'appareils de diagnostic, associée à la nécessité de se conformer à des normes réglementaires strictes, accélère encore la demande de services de maintenance fiables, ce qui en fait un moteur de marché crucial.

- Améliorer la précision du diagnostic et l'efficacité du traitement

Les dispositifs médicaux modernes deviennent de plus en plus complexes et intègrent des technologies avancées telles que l’IA, l’IoT et la robotique pour améliorer la précision du diagnostic, l’efficacité du traitement et les résultats pour les patients. Par conséquent, ces appareils sophistiqués nécessitent des services de maintenance spécialisés pour garantir leur fonctionnement à des niveaux de performance optimaux. La complexité des équipements tels que les systèmes de chirurgie robotique, les dispositifs de surveillance intelligents et les outils de diagnostic basés sur l’IA exige des techniciens hautement qualifiés et des protocoles de service spécialisés pour gérer les problèmes potentiels, l’étalonnage et les réparations. Le fait de ne pas entretenir correctement ces appareils peut entraîner des résultats inexacts ou des dysfonctionnements, ce qui a un impact direct sur la sécurité des patients et l’efficacité des soins de santé. Cette complexité croissante entraîne le besoin de services de maintenance spécialisés, contribuant de manière significative à la croissance du marché de la maintenance des équipements médicaux, car les prestataires de soins de santé investissent pour garantir la fiabilité des appareils et leur conformité aux normes réglementaires.

Opportunités

- Demande croissante de services contractuels

La demande croissante de contrats à long terme basés sur des accords de niveau de service (SLA) dans les établissements de santé représente une opportunité de croissance significative pour le marché de la maintenance des équipements médicaux. Les SLA impliquent généralement des conditions prédéfinies pour la maintenance de routine, les réparations d'urgence et l'étalonnage périodique des équipements, garantissant des performances optimales et la conformité aux normes réglementaires. Les prestataires de soins de santé préfèrent ces contrats car ils offrent des coûts prévisibles, réduisent le risque de pannes d'équipement inattendues et garantissent le fonctionnement continu des appareils critiques. Pour les prestataires de services, les SLA créent des flux de revenus stables et récurrents et renforcent les partenariats à long terme avec les organisations de soins de santé. Alors que les hôpitaux et les cliniques privilégient de plus en plus des solutions de maintenance rentables et fiables, le passage à des contrats basés sur des SLA améliore la croissance des entreprises, offrant aux prestataires de services la possibilité d'élargir leur clientèle et leur part de marché.

- Demande croissante d'établissements de soins de santé de pointe

Les hôpitaux et les cliniques adoptent de plus en plus d’appareils médicaux sophistiqués tels que les systèmes d’imagerie, les robots chirurgicaux et les équipements de surveillance des patients. La demande de maintenance régulière a donc considérablement augmenté. Ces appareils avancés sont essentiels pour des diagnostics, des traitements et des soins précis aux patients, ce qui rend leur fonctionnement optimal essentiel. Une maintenance régulière garantit la sécurité, minimise les temps d’arrêt et prolonge la durée de vie de l’équipement, évitant ainsi des réparations ou des remplacements coûteux. De plus, l’intégration de technologies numériques telles que l’IoT et l’IA dans les appareils médicaux nécessite une maintenance spécialisée pour assurer un flux de données fluide et l’interopérabilité des appareils. Cette dépendance croissante à l’égard des appareils de haute technologie dans les établissements de santé crée une opportunité de marché substantielle pour les prestataires de services proposant des solutions de maintenance, d’autant plus que les organismes de réglementation imposent un strict respect des normes de sécurité et de performance.

Contraintes/Défis

- Pénurie de techniciens qualifiés

La complexité croissante des dispositifs médicaux modernes représente un défi de taille pour le marché de la maintenance des équipements médicaux, car elle nécessite des techniciens hautement spécialisés pour assurer le bon fonctionnement et le respect des normes de sécurité. Des appareils tels que les systèmes chirurgicaux robotisés, les équipements d'imagerie avancés et les systèmes de surveillance des patients intègrent des technologies sophistiquées qui nécessitent des connaissances et des compétences approfondies en matière de maintenance et de réparation. Cependant, il existe une pénurie notable de professionnels qualifiés équipés pour gérer cette complexité, ce qui entraîne une concurrence accrue entre les établissements de santé pour recruter et retenir des techniciens qualifiés. Ce manque de talents peut entraîner des temps d'arrêt des équipements plus longs, des coûts d'exploitation plus élevés et des risques potentiels pour la sécurité des patients. Alors que la demande en dispositifs médicaux avancés continue d'augmenter, il devient crucial de remédier à cette pénurie de personnel qualifié pour soutenir la croissance du marché et garantir une prestation de soins de santé de haute qualité.

- Coût élevé des équipements médicaux de pointe

Les équipements médicaux de pointe nécessitent souvent des opérations de maintenance et de réparation coûteuses, ce qui constitue un frein important pour le marché de la maintenance des équipements médicaux. La nature complexe de ces appareils signifie que les entretiens de routine et les réparations imprévues peuvent entraîner des dépenses importantes. Pour de nombreux établissements de santé, en particulier les petits hôpitaux et cliniques, ces coûts peuvent grever des budgets limités et détourner des fonds d'autres domaines critiques, tels que les soins aux patients ou les investissements dans de nouvelles technologies. En outre, alors que les prestataires de soins de santé s'efforcent d'améliorer la qualité de leurs services tout en gérant les coûts opérationnels, la charge financière associée à la maintenance d'équipements médicaux complexes peut limiter leur capacité à mettre en œuvre les programmes de maintenance nécessaires. Par conséquent, cela peut entraîner une augmentation des temps d'arrêt des équipements et une baisse potentielle de la sécurité des patients et de la qualité des services, soulignant la nécessité de solutions de maintenance plus rentables dans le secteur.

Ce rapport de marché fournit des détails sur les nouveaux développements récents, les réglementations commerciales, l'analyse des importations et des exportations, l'analyse de la production, l'optimisation de la chaîne de valeur, la part de marché, l'impact des acteurs du marché national et local, les opportunités d'analyse en termes de poches de revenus émergentes, les changements dans la réglementation du marché, l'analyse stratégique de la croissance du marché, la taille du marché, la croissance des catégories de marché, les niches d'application et la domination, les approbations de produits, les lancements de produits, les expansions géographiques, les innovations technologiques sur le marché. Pour obtenir plus d'informations sur le marché, contactez Data Bridge Market Research pour un briefing d'analyste, notre équipe vous aidera à prendre une décision de marché éclairée pour atteindre la croissance du marché.

Portée du marché de la maintenance des équipements médicaux

Le marché est segmenté en fonction du type de service, des fournisseurs de services, du type d'appareil, du niveau de maintenance, de la technologie et des utilisateurs finaux. La croissance parmi ces segments vous aidera à analyser les segments de faible croissance dans les industries et à fournir aux utilisateurs un aperçu précieux du marché et des informations sur le marché pour les aider à prendre des décisions stratégiques pour identifier les principales applications du marché.

Type de service

- Préventif

- Correctif

- Performance/Opérationnel

Fournisseurs de services

- Prestataires de services internes

- Prestataires de services externes

Type d'appareil

- Équipement d'imagerie

- Dispositifs endoscopiques

- Equipement électromédical

- Instruments chirurgicaux

- Dispositifs de surveillance et de maintien des fonctions vitales des patients

- Équipement dentaire

- Autres équipements médicaux

Niveau de maintenance

- Niveau 1

- Niveau 2

- Niveau 3

- Utilisateur (ou première ligne)

- Spécialisé

- Technicien

Technologie

- Fabricants OEM multi-fournisseurs

- Fabricants OEM à fournisseur unique

- Organismes de services indépendants

- Maintenance interne

Utilisateur final

- Hôpitaux

- Cliniques

- Laboratoires

- Autres centres de santé

Analyse régionale du marché de la maintenance des équipements médicaux

Le marché est analysé et des informations sur la taille du marché et les tendances sont fournies par pays, type de service, fournisseurs de services, type d'appareil, niveau de maintenance, technologie et utilisateurs finaux, comme indiqué ci-dessus.

Les pays couverts dans le rapport de marché sont les États-Unis, le Canada et le Mexique en Amérique du Nord, l'Allemagne, la France, le Royaume-Uni, les Pays-Bas, la Suisse, la Belgique, la Russie, l'Italie, l'Espagne, la Turquie, le reste de l'Europe en Europe, la Chine, le Japon, l'Inde, la Corée du Sud, Singapour, la Malaisie, l'Australie, la Thaïlande, l'Indonésie, les Philippines, le reste de l'Asie-Pacifique (APAC) en Asie-Pacifique (APAC), l'Arabie saoudite, les Émirats arabes unis, l'Afrique du Sud, l'Égypte, Israël, le reste du Moyen-Orient et de l'Afrique (MEA) en tant que partie du Moyen-Orient et de l'Afrique (MEA), le Brésil, l'Argentine et le reste de l'Amérique du Sud en tant que partie de l'Amérique du Sud.

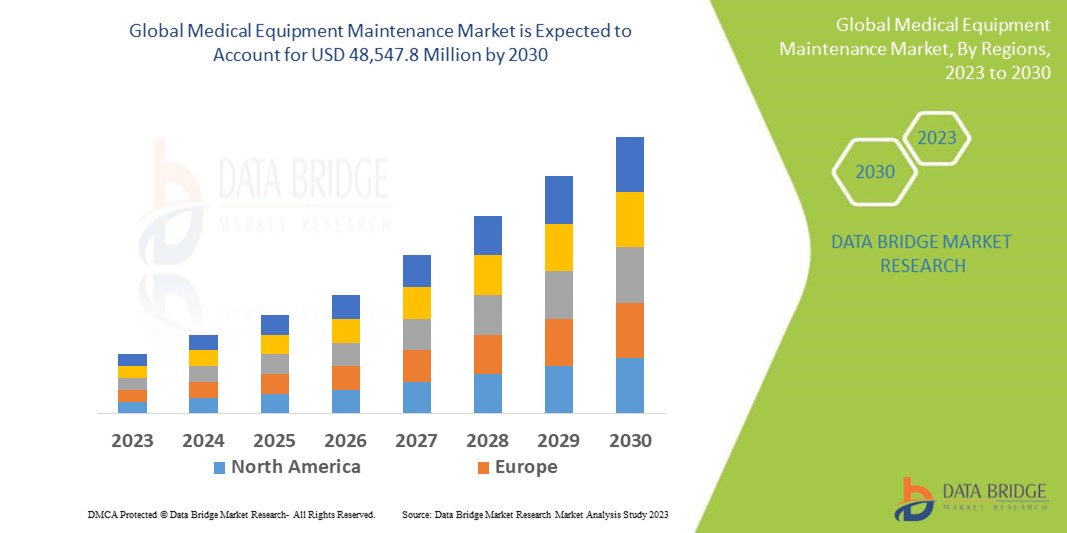

L'Amérique du Nord domine le marché de la maintenance des équipements médicaux, en raison de la prévalence croissante des maladies chroniques et de l'augmentation des dépenses de santé. La forte demande de la région en dispositifs médicaux de pointe devrait également alimenter la croissance du marché. Ensemble, ces facteurs positionnent l'Amérique du Nord comme une force dominante dans le secteur de la maintenance des équipements médicaux.

La région Asie-Pacifique est sur le point de connaître une croissance substantielle, portée par les initiatives gouvernementales visant à améliorer les services de santé. Le programme indien Ayushman Bharat Yojana, lancé en 2018, vise à fournir un accès gratuit aux soins de santé à près de 40 % de la population. De telles initiatives devraient accroître considérablement la demande de services de maintenance d'équipements médicaux dans la région.

La section pays du rapport fournit également des facteurs d'impact sur les marchés individuels et des changements de réglementation sur le marché national qui ont un impact sur les tendances actuelles et futures du marché. Des points de données tels que l'analyse de la chaîne de valeur en aval et en amont, les tendances techniques et l'analyse des cinq forces de Porter, les études de cas sont quelques-uns des indicateurs utilisés pour prévoir le scénario de marché pour les différents pays. En outre, la présence et la disponibilité des marques mondiales et les défis auxquels elles sont confrontées en raison de la concurrence importante ou rare des marques locales et nationales, l'impact des tarifs nationaux et les routes commerciales sont pris en compte tout en fournissant une analyse prévisionnelle des données nationales.

Part de marché de la maintenance des équipements médicaux

Le paysage concurrentiel du marché fournit des détails par concurrent. Les détails inclus sont la présentation de l'entreprise, les finances de l'entreprise, les revenus générés, le potentiel du marché, les investissements dans la recherche et le développement, les nouvelles initiatives du marché, la présence mondiale, les sites et installations de production, les capacités de production, les forces et les faiblesses de l'entreprise, le lancement du produit, la largeur et l'étendue du produit, la domination des applications. Les points de données ci-dessus fournis ne concernent que l'orientation des entreprises par rapport au marché.

Les leaders du marché de la maintenance des équipements médicaux opérant sur le marché sont :

- Koninklijke Philips NV (Pays-Bas)

- (Siemens Healthineers AG Allemagne)

- General Electric Company (États-Unis)

- Medtronic (Irlande)

- TeraRecon (États-Unis)

- Carestream Health (États-Unis)

- Société Shimadzu (Japon)

- Olympus Corporation (Japon)

- Boston Scientific Corporation (États-Unis)

- Cuisinier (États-Unis)

- Hoya Corporation (Japon)

- Richard Wolf GmbH (Allemagne)

- KARL STORZ (Allemagne)

- Smith+Nephew (Royaume-Uni)

- Zimmer Biomet (États-Unis)

Dernières évolutions sur le marché de la maintenance des équipements médicaux

- En mars 2023, Advantus Health Partners et GE HealthCare ont annoncé un accord stratégique d'une valeur pouvant atteindre 760 millions USD au cours de la prochaine décennie. Ce partenariat vise à fournir les services de gestion des technologies de santé (HTM) de GE aux clients d'Advantus Health Partners. Cette collaboration devrait améliorer la qualité et l'efficacité de la gestion des technologies de santé dans les établissements associés

- En mars 2023, Medipass Healthcare et Althea UK ont annoncé leur fusion, donnant naissance à un nouveau nom : Ergéa. La société nouvellement créée est spécialisée dans un large éventail de domaines médicaux, notamment l'endoscopie, la radiologie, la cardiologie, la radiothérapie et les blocs opératoires. En outre, Ergéa fournit des services de maintenance indépendants des fournisseurs pour les équipements de radiologie, d'endoscopie et biomédicaux dans tout le Royaume-Uni, améliorant ainsi le soutien aux établissements de santé.

- En juillet 2022, B. Braun a créé un centre de service technique visant à fournir des services de réparation et de maintenance d'équipements médicaux de haute qualité. Cette initiative vise à renforcer le système de santé publique en Thaïlande en garantissant que les établissements de santé ont accès à une assistance fiable pour leurs dispositifs médicaux. En renforçant les capacités de maintenance, B. Braun cherche à améliorer les résultats globaux des soins de santé et l'efficacité opérationnelle dans la région

- En mai 2022, Fresenius Kabi a finalisé l'acquisition d'Ivenix Inc., une société spécialisée dans la thérapie par perfusion. Cette opération stratégique permettra d'intégrer le matériel et les logiciels d'Ivenix pour créer une gamme complète de dispositifs médicaux avancés adaptés au marché américain. Cette collaboration vise à améliorer l'efficacité et l'efficience des solutions de thérapie par perfusion, renforçant ainsi la position de Fresenius Kabi dans le secteur de la santé.

- En mars 2022, Source Bioscience International plc a acquis LDPath Ltd., un fournisseur londonien de services de tests de pathologie numérique. LDPath a créé une plateforme de pathologie numérique innovante qui est de plus en plus adoptée dans le secteur. La nouvelle entité, Source LDP, vise à offrir un parcours complet aux patients, englobant tout, de la consultation initiale au diagnostic, améliorant ainsi l'expérience globale des soins de santé.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.