Global Intravenous Access Devices Market

Taille du marché en milliards USD

TCAC :

%

USD

7.28 Billion

USD

11.42 Billion

2024

2032

USD

7.28 Billion

USD

11.42 Billion

2024

2032

| 2025 –2032 | |

| USD 7.28 Billion | |

| USD 11.42 Billion | |

| % | |

|

Global Intravenous Access Devices Market Segmentation, By Product (Intravenous Catheters, Intravenous Infusion Pumps, and Intravenous Needles), End User (Hospitals and Clinics, Ambulatory Surgery Centers, Dialysis Centers, Home Care, and Others), Application (Medication Administration, Administration of Fluid and Nutrition, Transfusion of Blood Products, and Diagnostic Testing) – Industry Trends and Forecast to 2032

Intravenous Access Devices Market Analysis

The intravenous access devices market is expanding due to the increasing demand for efficient and safe intravenous (IV) therapies across various healthcare settings. Intravenous devices are essential for administering fluids, medications, blood products, and nutrition, especially for patients in critical care, hospitals, and ambulatory surgery centers. The market is driven by the rising prevalence of chronic diseases, an aging population, and a surge in the need for surgical procedures requiring IV access. In addition, advancements in technology are significantly improving the design and safety features of IV devices. For instance, the development of needle-free blood collection systems such as BD's PIVO Pro and innovations in safety IV catheters, such as B. Braun's Introcan Safety 2, help minimize the risk of needle-stick injuries and prevent exposure to bloodborne pathogens. Furthermore, companies are focusing on improving the functionality of IV catheters, with features such as multi-access blood control and dual-lumen catheters. The integration of smart technologies, such as connected infusion pumps, is enhancing patient safety and reducing medical errors. As healthcare infrastructure improves globally, especially in emerging regions, the intravenous access devices market is expected to see substantial growth in the coming years.

Intravenous Access Devices Market Size

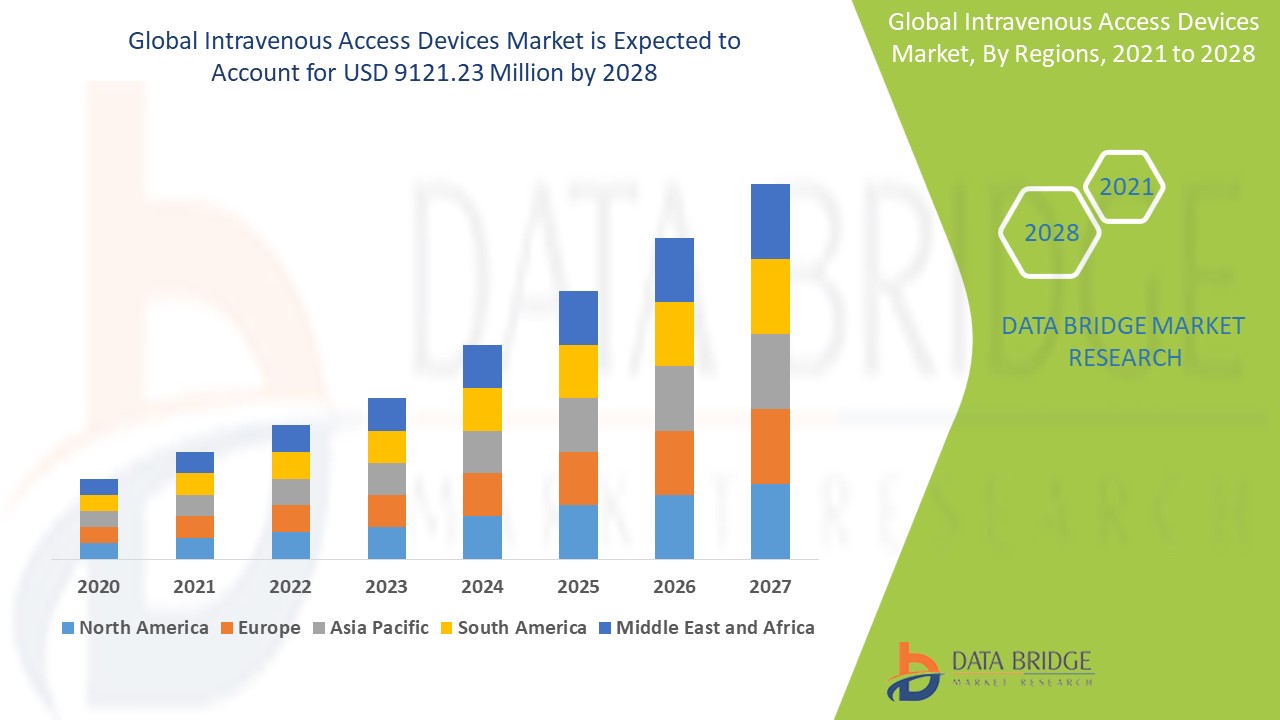

The global intravenous access devices market size was valued at USD 7.28 billion in 2024 and is projected to reach USD 11.42 billion by 2032, with a CAGR of 5.78% during the forecast period of 2025 to 2032. In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework.

Intravenous Access Devices Market Trends

“Increasing Adoption of Safety Features”

One prominent trend in the intravenous access devices market is the increasing adoption of safety features aimed at reducing the risk of needlestick injuries and improving patient outcomes. Devices such as the BD PIVO Pro, a needle-free blood collection device, and B. Braun’s Introcan Safety 2 IV catheter are gaining significant traction due to their enhanced safety features. These innovations help protect healthcare workers from potential exposure to bloodborne pathogens and reduce the risk of complications such as infections. In addition, advancements in smart infusion pumps, which offer real-time monitoring and automated drug delivery, are contributing to better management of intravenous therapies, especially in critical care settings. For instance, companies such as Medtronic and Teleflex are integrating digital solutions into their infusion devices, allowing for more accurate and efficient treatments. As healthcare systems focus on improving patient and provider safety, the market for intravenous access devices continues to expand, driven by these technological innovations.

Report Scope and Intravenous Access Devices Market Segmentation

|

Attributes |

Intravenous Access Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

U.S., Canada and Mexico in North America, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Rest of Europe in Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E., South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA), Brazil, Argentina and Rest of South America as part of South America |

|

Key Market Players |

BD (U.S.), B. Braun SE (Germany), Teleflex Incorporated (U.S.), Medtronic (Ireland), Smiths Group plc (U.K.), Pfizer Inc. (U.S.), Fresenius Medical Care AG (Germany), Baxter (U.S.), Siemens Healthineers AG (Germany), Terumo Corporation (Japan), Nipro Europe Group Companies (Belgium), Edwards Lifesciences Corporation (U.S.), General Electric Company (U.S.), AngioDynamics (U.S.), Cook (U.S.), Deltamed (Belgium), Galt Medical Corp. (U.S.), ICU Medical, Inc. (U.S.), and Retractable Technologies, Inc (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Intravenous Access Devices Market Definition

Intravenous access devices are medical instruments used to provide direct access to a patient's bloodstream through a vein. These devices facilitate the administration of fluids, medications, blood products, and nutrients, and they are essential in various medical settings, including hospitals, clinics, and home healthcare.

Intravenous Access Devices Market Dynamics

Drivers

- Increasing Prevalence of Chronic Diseases

The increasing prevalence of chronic diseases, such as diabetes, cancer, and cardiovascular conditions, is significantly driving the demand for intravenous access devices. According to the World Health Organization (WHO), chronic diseases account for approximately 70% of all deaths worldwide, with cardiovascular diseases being the leading cause, followed by cancer and diabetes. These conditions often require long-term intravenous therapies, including chemotherapy, insulin infusions, and pain management treatments. For instance, cancer patients undergoing chemotherapy rely on intravenous access for the administration of treatment drugs, and diabetic patients may require intravenous insulin in hospital settings during acute episodes. As the number of individuals diagnosed with these conditions continues to rise, particularly in aging populations, the need for reliable and efficient intravenous access devices is growing rapidly. This trend underscores the importance of intravenous devices in chronic disease management and contributes to the expansion of the intravenous access devices market.

- Rising Number of Surgical Procedures Worldwide

The rising number of surgical procedures worldwide is driving the demand for intravenous access devices, as they are essential for delivering anesthesia, medications, and fluids during and after operations. According to the World Health Organization (WHO), over 230 million surgeries are performed globally each year, and this number continues to rise as populations age and medical technologies advance. Intravenous access devices, such as catheters and infusion pumps, are crucial in these settings for the safe administration of anesthesia and post-operative care. For instance, intravenous catheters are used to administer anesthesia during surgeries and are essential for fluid management, pain relief, and administering antibiotics post-operation. As the number of elective and emergency surgeries grows, particularly in regions such as North America and Europe, the demand for efficient intravenous access devices is expected to increase, further fueling the growth of the market. This rise in surgical procedures is a key market driver, contributing to the global demand for advanced intravenous access devices.

Opportunities

- Increasing Advancements in Technology

Advancements in technology are significantly driving the intravenous access devices market, with innovations such as needle-free systems, smart infusion pumps, and safer IV catheters offering improved patient safety and better treatment outcomes. For instance, needle-free systems, such as BD’s PIVO Pro, allow for blood collection without the need for traditional needles, reducing the risk of needlestick injuries, which is a major concern in healthcare. In addition, smart infusion pumps, such as those developed by companies such as Medtronic, provide automated medication delivery with precise dosing and continuous monitoring, reducing human error and enhancing treatment effectiveness. The development of IV catheters with integrated safety mechanisms, such as B. Braun’s Introcan Safety 2, is helping prevent needlestick injuries and minimizing exposure to bloodborne pathogens. These innovations make intravenous access devices safer and more efficient, opening up new market opportunities, particularly in settings that require high standards of care, such as hospitals and surgical centers. As these technologies become more accessible, they are poised to further expand the global intravenous access devices market.

- Expanding Healthcare Facilities in Developing Regions

Expanding healthcare facilities in developing regions, combined with advancements in medical technologies, is creating significant opportunities for growth in the intravenous access devices market. For instance, countries in Asia-Pacific and Africa are increasingly investing in healthcare infrastructure, building new hospitals, clinics, and surgical centers to accommodate their growing populations and rising healthcare demands. This is being paired with the adoption of advanced medical technologies such as smart infusion pumps and safer, more efficient IV catheters. In countries such as India and China, where healthcare access is improving rapidly, the demand for reliable intravenous access device is increasing as more surgeries, cancer treatments, and long-term therapies are performed. For instance, Medtronic’s infusion systems, which offer greater precision and safety, are becoming integral in these regions to enhance patient care. As healthcare systems modernize and expand, these innovations are driving the demand for advanced intravenous access solutions, making it a significant market opportunity in developing economies.

Restraints/Challenges

- Complications and The Risk of Infection

Complications and the risk of infection remain significant challenges in the intravenous (IV) access devices market, as these devices are susceptible to causing serious health issues, including catheter-associated bloodstream infections (CABSI). For instance, when IV catheters are not properly maintained or when they are left in place for extended periods, bacteria can enter the bloodstream, leading to potentially life-threatening infections. This risk is particularly high in critically ill patients or those requiring long-term IV therapy, such as cancer patients undergoing chemotherapy or patients in intensive care units. Infections can result in longer hospital stays, increased medical costs, and higher mortality rates. Furthermore, managing these infections often requires the use of stronger, more expensive antibiotics and additional medical procedures, thus escalating the financial burden. The presence of infections affects patient outcomes and poses significant operational challenges for healthcare providers, as they must invest in better infection-control practices, sterilization techniques, and monitoring systems to reduce these risks. As a result, the high risk of infection linked to IV access devices limits their widespread adoption and effectiveness, making it a key challenge in the growth of the market.

- High Costs and Reimbursement Issues

High costs and reimbursement issues present a significant challenge in the intravenous (IV) access devices market, as advanced IV technologies often come with substantial financial burdens that can limit their accessibility and widespread adoption. For instance, devices with antimicrobial coatings or those designed for long-term use, such as peripherally inserted central catheters (PICC), are often more expensive than traditional devices due to their advanced materials and design. These higher costs are particularly burdensome for hospitals, especially in regions with limited healthcare budgets or where reimbursement rates are low. In many cases, insurance companies may not fully cover the cost of these advanced IV devices, forcing healthcare providers and patients to bear the financial burden. As a result, hospitals may opt for cheaper, less effective alternatives, despite the potential for better patient outcomes with more advanced options. The lack of adequate reimbursement further compounds the financial challenges faced by healthcare providers, particularly in regions with high out-of-pocket costs for patients. These financial barriers, alongside reimbursement complexities, hinder the adoption of innovative IV access devices, restricting the market's growth and limiting the ability of patients to benefit from improved treatment options.

This market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on the market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

Intravenous Access Devices Market Scope

The market is segmented on the basis of product, end user, and application. The growth amongst these segments will help you analyse meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Product

- Intravenous Catheters

- Intravenous Infusion Pumps

- Intravenous Needles

End User

- Hospitals and Clinics

- Ambulatory Surgery Centers

- Dialysis Centers

- Home Care

- Others

Application

- Medication Administration

- Administration of Fluid and Nutrition

- Transfusion of Blood Products

- Diagnostic Testing

Intravenous Access Devices Market Regional Analysis

The market is analysed and market size insights and trends are provided by country, product, end user, and application as referenced above.

The countries covered in the market report are U.S., Canada and Mexico in North America, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Rest of Europe in Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E., South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA), Brazil, Argentina and Rest of South America as part of South America.

North America dominates the intravenous access devices market, driven by the growing elderly population and the rising incidence of chronic diseases. The region's well-established healthcare infrastructure and advanced medical technology contribute to the demand for intravenous devices. In addition, a higher number of hospital admissions and treatments in North America further fuels market growth. These factors, coupled with an increasing need for effective and reliable intravenous access, support the market's dominance in the region.

Asia-Pacific is anticipated to experience the highest growth in the intravenous access devices market from 2025 to 2032, driven by the rising incidence of target diseases and a growing elderly population. The region's improving healthcare infrastructure and expanding access to advanced medical technologies are further accelerating market expansion. Increasing healthcare investments and rising awareness about disease management also play a key role in boosting market growth. As healthcare systems evolve and demand for better treatment options rises, Asia-Pacific's market is set to witness significant development during this period.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points such as down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

Intravenous Access Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

Intravenous Access Devices Market Leaders Operating in the Market Are:

- BD (U.S.)

- B. Braun SE (Germany)

- Teleflex Incorporated (U.S.)

- Medtronic (Ireland)

- Smiths Group plc (U.K.)

- Pfizer Inc. (U.S.)

- Fresenius Medical Care AG (Germany)

- Baxter (U.S.)

- Siemens Healthineers AG (Germany)

- Terumo Corporation (Japan)

- Nipro Europe Group Companies (Belgium)

- Edwards Lifesciences Corporation (U.S.)

- General Electric Company (U.S.)

- AngioDynamics (U.S.)

- Cook (U.S.)

- Deltamed (Belgium)

- Galt Medical Corp. (U.S.)

- ICU Medical, Inc. (U.S.)

- Retractable Technologies, Inc (U.S.)

Latest Developments in Intravenous Access Devices Market

- In November 2023, BD introduced the PIVO Pro, a groundbreaking needle-free blood collection device. It is the first to integrate seamlessly with both long-term and integrated peripheral IV catheters, including the Nexiva system, which now features the FDA-approved NearPort IV Access

- In October 2023, B. Braun Medical Inc. launched the Introcan Safety 2 IV Catheter, incorporating Multi-Access Blood Control to enhance passive needlestick prevention. The design is aimed at reducing clinicians' exposure to blood, minimizing the risk of bloodborne pathogen transmission during intravenous procedures

- In June 2023, Teleflex Incorporated secured two group purchasing agreements with Premier, Inc., enabling Premier members to access exclusive pricing and terms on Teleflex’s Central Venous and Arterial Vascular Access products

- In July 2022, B. Braun Medical Inc. unveiled its new Introcan Safety 2 IV Catheter featuring one-time blood control. This innovation is designed to improve IV access safety for clinicians by reducing the risk of needlestick injuries and blood exposure

- In May 2022, Access Vascular, Inc. (AVI) received FDA 510(k) clearance for its HydroPICC Dual-Lumen catheter. Built with the same proprietary hydrophilic biomaterial as AVI’s single-lumen HydroPICC and HydroMID® catheters, it demonstrated significant reductions in complications such as occlusions, Deep Vein Thrombosis, phlebitis, and catheter replacements in recent studies

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.