Global Medical Device Warehouse And Logistics Market

Marktgröße in Milliarden USD

CAGR :

%

USD

43.03 Billion

USD

62.13 Billion

2024

2032

USD

43.03 Billion

USD

62.13 Billion

2024

2032

| 2025 –2032 | |

| USD 43.03 Billion | |

| USD 62.13 Billion | |

| % | |

|

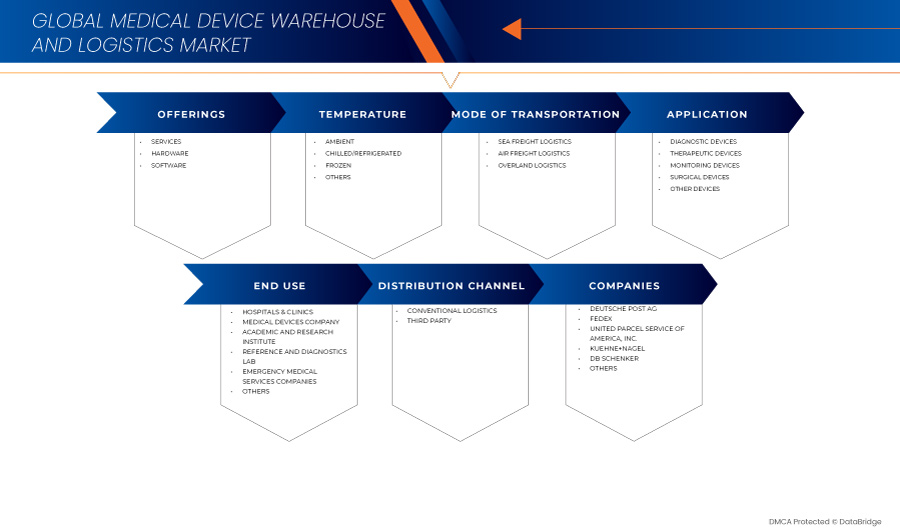

Global Medical Device Warehouse and Logistics Market Segmentation, By Offerings (Services, Hardware, and Software) Temperature (Ambient, Chilled/Refrigerated, Frozen, and Others), Mode of Transportation (Sea Freight Logistics, Air Freight Logistics, and Overland Logistics), Application (Diagnostic Devices, Therapeutic Devices, Monitoring Devices, Surgical Devices, and Other Devices), End Use (Hospitals & Clinics, Medical Devices Companies, Academic & Research Institute, Reference & Diagnostics Laboratories, Emergency Medical Services Companies, and Others), Distribution Channel (Conventional Logistics and Third Party) – Industry Trends and Forecast to 2031

Medical Device Warehouse and Logistics Market Analysis

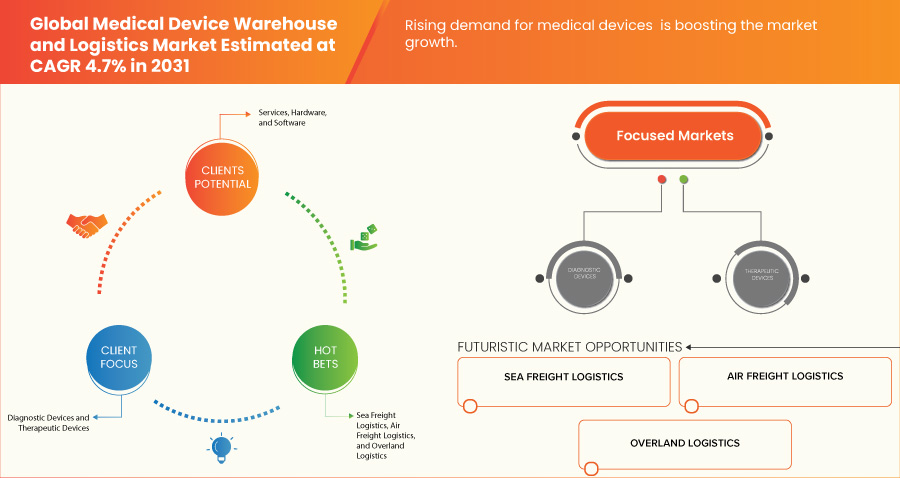

The medical device warehouse and logistics market is experiencing robust growth, driven by rising demand for medical devices. As the global healthcare industry continues to expand, the need for efficient storage, handling, and distribution of medical devices has grown exponentially. adoption of advanced technologies in logistics management and strategic partnerships and mergers between medical device manufacturers and logistics and e-commerce companies are enhancing performance and expanding their applications. Market dynamics are also influenced by fluctuations in raw material prices and geopolitical factors affecting supply chains. Overall, the market is expected to continue expanding, with a focus on innovation and sustainability to meet evolving industrial demands.

Medical Device Warehouse and Logistics Market Size

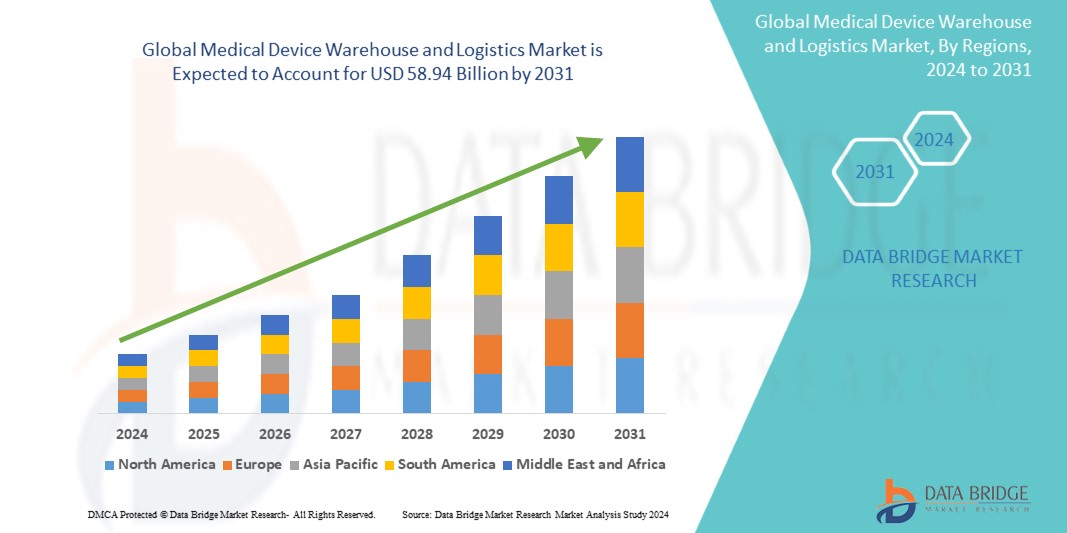

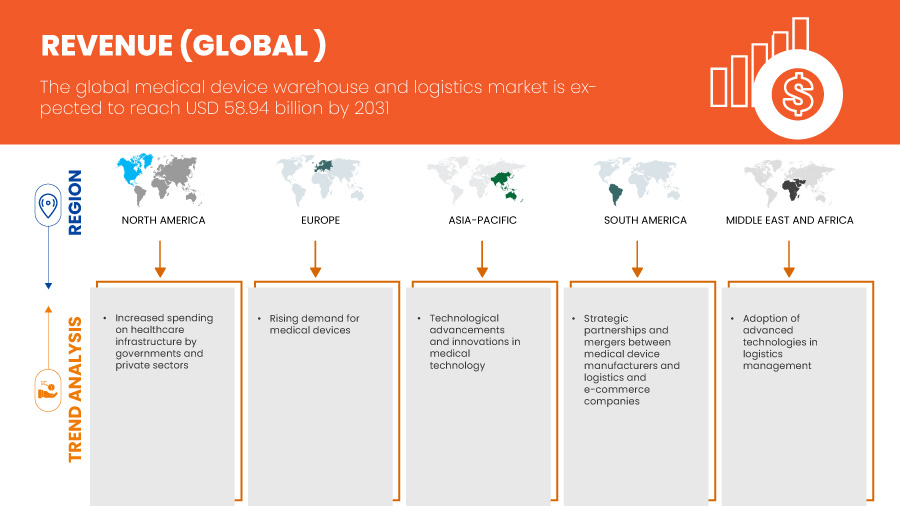

Global medical device warehouse and logistics market size was valued at USD 41.10 billion in 2023 and is projected to reach USD 58.94 billion by 2031, with a CAGR of 4.7% during the forecast period of 2024 to 2031. In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework.

Medical Device Warehouse and Logistics Market Trends

“Technological Advancements and Innovations in Medical Technology”

Technological advancements and innovations in medical technology are the key trend of the medical device warehouse and logistics market, reshaping how medical devices are stored, handled, and distributed. As medical devices become more sophisticated and require greater precision, the logistics infrastructure supporting their delivery must evolve to meet these advanced needs. The increasing complexity and sensitivity of devices, such as robotic surgical systems, implantable devices, diagnostic equipment, and wearable health tech, demand specialized warehousing solutions that ensure the safety, efficacy, and compliance of these products.

In addition, IoT integration in warehouses has enabled real-time inventory tracking, allowing logistics providers to monitor device conditions during transport and storage. 3D printing technology is also revolutionizing medical device manufacturing, leading to the production of customized implants, prosthetics, and surgical tools. These bespoke devices require efficient and rapid distribution to healthcare facilities. As a result, logistics providers are investing in agile warehousing systems that can manage the growing demand for just-in-time delivery, reducing lead times and ensuring that custom-made devices reach their destinations quickly. These advancements ensure the safe delivery of sensitive medical products, driving demand for cold storage warehouses with cutting-edge capabilities.

Report Scope and Medical Device Warehouse and Logistics Market Segmentation

|

Attributes |

Medical Device Warehouse and Logistics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, Switzerland, Netherlands, Russia, Belgium, Finland, Denmark, Poland, Norway, Sweden, Hungary, rest of Europe, China, Japan, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, New Zealand, Vietnam, Taiwan, rest of Asia-Pacific, Brazil, Argentina, rest of South America, South Africa, Saudi Arabia, U.A.E., Israel, Egypt, Kuwait, Oman, Bahrain, and rest of Middle East and Africa |

|

Key Market Players |

Deutsche Post AG (Germany), FedEx (U.S.), United Parcel Service of America, Inc. (U.S.), Kuehne+Nagel (U.K), DB SCHENKER (Germany), Alloga (U.K.), AWL India Private Limited (India), C.H. Robinson Worldwide, Inc. (U.S.), CAVALIER LOGISTICS (U.S.), CEVA (France), Crown LSP Group (U.S.), Dimerco (Taiwan), DSV (Denmark), FM Logistic (France), Hansa International (China), Hellmann Worldwide Logistics SE & Co. KG (Germany), Imperial (South Africa), Mercury Business Services (U.S.), Movianto (Netherlands), Murphy Logistics (U.S.), OIA Global (U.S.), Omni Logistics, LLC (U.S.), puracon Gmbh (Germany), Rhenus Group (Germany), SEKO (U.S.), TIBA (Spain), Toll Holdings Limited (Australia), Warehouse Anywhere (U.S.), and XPO, Inc. (U.S.) among others |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Medical Device Warehouse and Logistics Market Definition

Medical device warehouse and logistics refers to the specialized processes and systems involved in the storage, management, and distribution of medical devices within the healthcare supply chain. This includes the warehousing of various medical products—such as surgical instruments, diagnostic equipment, and implants— while ensuring compliance with stringent regulatory standards for safety and efficacy. Logistics encompasses the planning and execution of transportation, inventory management, and order fulfillment to ensure timely delivery to healthcare providers and patients. Effective warehouse and logistics operations are critical for maintaining product availability, minimizing delays, and optimizing costs, ultimately supporting better patient care and outcomes in the healthcare ecosystem.

Medical Device Warehouse and Logistics Market Dynamics

Drivers

- Rising Demand for Medical Devices

The rising demand for medical devices is a significant driver of the global medical device warehouse and logistics market. As the global healthcare industry continues to expand, the need for efficient storage, handling, and distribution of medical devices has grown exponentially. This surge is driven by several factors, including the increasing prevalence of chronic diseases, advancements in medical technology, an aging population, and the growing demand for healthcare services across both developed and developing markets. As medical devices become more sophisticated and diverse, the logistics and warehousing requirements to support their distribution become more critical.

In addition, as the medical device industry becomes more globalized, companies are outsourcing their logistics and warehousing needs to third-party logistics providers (3PLs) that specialize in handling healthcare products. These 3PLs offer value-added services such as inventory management, cold chain logistics, and last-mile delivery solutions that are tailored to the specific requirements of medical devices. By leveraging the expertise of these logistics providers, medical device companies can streamline their supply chains, reduce costs, and ensure compliance with international regulations.

For instance,

In September 2023, according to an article published by Rapid Medtech Communications Ltd, the demand for medical devices has been on the rise due to an aging global population and increasing prevalence of chronic diseases. The ongoing shift towards minimally invasive procedures and personalized medicine has also spurred the need for specialized medical devices, contributing to the expansion.

- Increased Spending on Healthcare Infrastructure by Governments and Private Sectors

Government and private sector increased spending on healthcare infrastructure is a significant driver for the medical device warehouse and logistics market. As countries invest heavily in upgrading healthcare facilities, expanding services, and integrating advanced medical technologies, the demand for medical devices and the associated logistics infrastructure is surging.

Governments worldwide are allocating substantial budgets toward building new hospitals, expanding existing facilities, and upgrading outdated equipment. Countries such as India and Brazil have announced significant investments in healthcare infrastructure to ensure better access to medical services for their populations. This push toward modernization necessitates a comprehensive supply chain strategy for medical devices, from manufacturing and storage to distribution and delivery. As healthcare facilities grow, the need for efficient warehousing and logistics solutions to manage increased inventory levels becomes paramount. Private sector investments in healthcare are equally noteworthy.

In addition, the global emphasis on preparedness for future health crises is prompting governments and organizations to stockpile essential medical devices and supplies. This proactive approach increases demand for warehouses capable of storing large quantities of medical devices, with robust logistics systems to facilitate rapid deployment in emergencies.

For instance,

In January 2024, according to an article published on the Invest India website, India’s National Health Mission saw significant funding for improving healthcare infrastructure, particularly in rural areas. The government’s investment in upgrading hospitals and healthcare centers has led to increased demand for medical devices, necessitating the expansion of warehousing and logistics operations.

Opportunities

- Adoption of Advanced Technologies in Logistics Management

The adoption of advanced technologies in logistics management is transforming the medical device warehouse and logistics market, creating significant opportunities for growth and efficiency. As the healthcare sector increasingly demands precision and speed, the integration of technologies such as IoT, AI, and blockchain is revolutionizing how medical devices are stored, tracked, and distributed.

Advanced technologies enable real-time tracking of medical devices throughout the supply chain. IoT devices can provide continuous monitoring of environmental conditions (such as temperature and humidity) critical for sensitive medical products. This visibility not only ensures compliance with regulatory standards but also enhances inventory management, reducing the risk of overstocking or stockouts. Automation in warehousing operations, through robotics and AI-driven systems, streamlines the picking, packing, and shipping processes. This leads to reduced labor costs and increased speed in order fulfillment. Automated systems can optimize storage solutions, ensuring that medical devices are readily accessible while maximizing space utilization.

For instance,

In 2021, according to an article published by Elsevier B.V., the increasing importance of logistics centers in supply chains is evident as they navigate a competitive market and rising customer expectations. This situation compels these centers to adopt various technological solutions to enhance service quality. This article aims to explore the current development stage of modern technologies in logistics centers and to identify the associated benefits and challenges. A case study of logistics centers in Poland was conducted using a questionnaire survey. Results indicate that while these centers are evolving, there remains a significant need for further technological advancement.

- Strategic Partnerships and Mergers Between Medical Device Manufacturers and Logistics and E-Commerce Companies

Strategic partnerships and mergers between medical device manufacturers and logistics and e-commerce companies present significant opportunities for the medical device warehouse and logistics market. As the demand for medical devices continues to surge, driven by technological advancements and an aging population, collaboration across sectors is crucial for improving efficiency and expanding market reach.

By partnering with logistics and e-commerce firms, medical device manufacturers can leverage established distribution networks. These partnerships enable manufacturers to access advanced logistics capabilities, including faster shipping, improved last-mile delivery, and broader geographic coverage. This is particularly important in an industry where timely delivery of products can impact patient care. Mergers between medical device companies and logistics providers can lead to streamlined operations. Shared expertise allows for better alignment of production and distribution processes, reducing lead times and costs. Integrated supply chain management can enhance inventory control and minimize wastage, which is critical in managing sensitive medical products.

Collaborating with e-commerce companies allows medical device manufacturers to adopt innovative technologies more rapidly. These partnerships can facilitate the integration of digital tools such as AI-driven demand forecasting, data analytics, and automated warehousing solutions. Such technologies improve efficiency and accuracy in inventory management and order fulfillment. Strategic alliances can also open new market segments for medical device manufacturers. E-commerce platforms provide an avenue to reach smaller healthcare providers and consumers directly, bypassing traditional distribution barriers. This democratization of access not only increases sales opportunities but also enhances patient accessibility to essential medical products.

For instance,

In January 2023, according to an article published by ResearchGate GmbH, the global supply chain is crucial for the development and distribution of medical devices used in diagnosing and treating health conditions. This paper explores how global supply chains affect the medical device industry, focusing on production centers and transportation challenges. It highlights how disruptions—stemming from trade law changes, transportation issues, and geopolitical tensions—lead to shortages and delays. The analysis includes financial impacts, cost structure variables such as raw material prices and labor costs, and the influence of supply chain consolidation on pricing and competition. Finally, it suggests strategies such as localized production and digitization to enhance resilience.

Restraints/Challenges

- Supply Chain Disruptions

Supply chain disruptions pose a significant restraint to the medical device warehouse and logistics market, undermining its efficiency, profitability, and ability to meet rising demand. As the medical device industry relies on the seamless flow of goods, any breakdown in the supply chain can have severe consequences, delaying the delivery of critical products and creating bottlenecks that are difficult to overcome. These disruptions often stem from a range of issues, including geopolitical tensions, global pandemics, natural disasters, and regulatory changes, all of which can affect the sourcing, manufacturing, and distribution of medical devices.

One of the primary challenges is the shortage of raw materials and components essential for the production of medical devices. Many medical device manufacturers source parts and materials from multiple global suppliers. However, when a supplier faces delays due to factors like port closures, transportation delays, or labor shortages, it directly impacts production timelines. This ripple effect slows down the manufacturing process, delaying deliveries to warehouses and, subsequently to healthcare facilities, further straining the logistics chain. This not only increases lead times but also creates backlogs in inventory management. Another critical factor is the complexity of global regulatory compliance. Different countries have varying regulatory frameworks governing the import and export of medical devices. Changes in trade policies, such as new tariffs or restrictions, can disrupt established supply routes and force companies to reconfigure their logistics strategies. This leads to higher operational costs and delays, further hindering market growth.

For instance,

In July 2024, according to an article published by Forbes, the global chip shortage heavily impacted technology and service companies, hindering production and delaying deliveries. The semiconductor supply chain disruptions caused by the pandemic and geopolitical tensions have forced businesses to rethink strategies, with many companies now facing challenges in meeting consumer demand. Many advanced medical devices, such as diagnostic equipment and imaging machines, rely on semiconductors. This global semiconductor shortage that began in 2020 has affected the production and delivery of these medical devices. Manufacturers were unable to meet production deadlines, leading to delays in shipments. Warehouses had to adjust their inventory management systems to cope with uncertain supply schedules, further straining the medical device logistics network.

- Complex Regulatory Requirements for Logistics Providers to Ensure Compliance

The medical device warehouse and logistics market faces significant challenges due to complex regulatory requirements. These regulations are essential for ensuring patient safety and product efficacy, but they also impose substantial burdens on logistics providers. Navigating this intricate landscape can hinder operational efficiency and increase costs.

Regulations require logistics providers to implement rigorous quality control measures. This includes monitoring environmental conditions for sensitive medical devices, such as temperature and humidity. Ensuring compliance with these quality standards adds layers of complexity to logistics operations, requiring investment in technology and training that can strain resources. To comply with regulatory standards, logistics providers must invest in ongoing training for their staff. This is essential to keep employees informed about current regulations, best practices, and compliance procedures. The need for specialized knowledge can result in higher operational costs and may lead to staffing challenges, particularly in regions with a limited pool of trained professionals.

For instance,

In February 2024, according to an article published by AltexSoft, healthcare logistics involves managing the flow of medical supplies, pharmaceuticals, and devices to ensure timely and safe delivery. With strict regulations governing handling, temperature control, and expiration management, efficient logistics is crucial for patient care. Technology plays a key role in addressing these challenges. IoT devices enable real-time monitoring of conditions, while inventory management software automates expiry tracking. Telemetry systems offer precise shipment tracking, and quality management software ensures regulatory compliance. Companies such as Pfizer, Eli Lilly, and Novartis are leveraging advanced technologies to optimize their supply chains and enhance operational efficiency.

This market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on the market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

Impact and Current Market Scenario of Raw Material Shortage and Shipping Delays

Data Bridge Market Research bietet eine umfassende Marktanalyse und liefert Informationen, indem es die Auswirkungen und das aktuelle Marktumfeld von Rohstoffknappheit und Lieferverzögerungen berücksichtigt. Dies bedeutet, dass strategische Möglichkeiten bewertet, wirksame Aktionspläne erstellt und Unternehmen bei wichtigen Entscheidungen unterstützt werden.

Neben dem Standardbericht bieten wir auch detaillierte Analysen des Beschaffungsniveaus anhand prognostizierter Lieferverzögerungen, Händlerzuordnung nach Regionen, Warenanalysen, Produktionsanalysen, Preiszuordnungstrends, Beschaffung, Kategorieleistungsanalysen, Lösungen zum Lieferkettenrisikomanagement, erweitertes Benchmarking und andere Dienste für Beschaffung und strategische Unterstützung.

Erwartete Auswirkungen der Konjunkturabschwächung auf die Preisgestaltung und Verfügbarkeit von Produkten

Wenn die Wirtschaftstätigkeit nachlässt, leiden auch die Branchen darunter. Die prognostizierten Auswirkungen des Konjunkturabschwungs auf die Preisgestaltung und Verfügbarkeit der Produkte werden in den von DBMR bereitgestellten Markteinblickberichten und Informationsdiensten berücksichtigt. Damit sind unsere Kunden ihren Konkurrenten in der Regel immer einen Schritt voraus, können ihre Umsätze und Erträge prognostizieren und ihre Gewinn- und Verlustaufwendungen abschätzen.

Marktumfang für Lager und Logistik für medizinische Geräte

Der Markt ist nach Angebot, Temperatur, Transportart, Anwendung, Endverbrauch und Vertriebskanal segmentiert. Das Wachstum dieser Segmente hilft Ihnen bei der Analyse schwacher Wachstumssegmente in den Branchen und bietet den Benutzern einen wertvollen Marktüberblick und Markteinblicke, die ihnen bei der strategischen Entscheidungsfindung zur Identifizierung der wichtigsten Marktanwendungen helfen.

Angebote

- Dienstleistungen

- Logistik

- Logistik nach Typ

- Keine Kühlkette

- Kühlkette

- Kühlkette nach Temperaturtyp

- Temperaturgesteuert

- Nicht temperaturgesteuert

- Logistik nach Typ

- Lagerung und Lagerhaltung

- Lagerung und Lagerhaltung nach Gerätetyp

- Diagnosegeräte

- Therapeutische Geräte

- Überwachungsgeräte

- Chirurgische Geräte

- Andere Geräte

- Lagerung und Lagerhaltung, nach Typ

- Vor Ort

- Außerhalb des Geländes

- Lagerung und Lagerhaltung nach Gerätetyp

- Verpackung

- Verpackung nach Gerätetyp

- Diagnosegeräte

- Therapeutische Geräte

- Überwachungsgeräte

- Chirurgische Geräte

- Andere Geräte

- Verpackung nach Gerätetyp

- Überwachungsdienste

- Sonstiges

- Logistik

- Hardware

- RFID-Geräte

- Barcodes

- IoT-Sensoren

- Sonstiges

- Software

- Integriert

- Standalone

Temperatur

- Umgebung

- Gekühlt

- Gefroren

- Sonstiges

Transportmittel

- Seefrachtlogistik

- Keine Kühlkette

- Kühlkette

- Kühlkette nach Temperaturtyp

- Temperaturgesteuert

- Nicht temperaturgesteuert

- Kühlkette nach Temperaturtyp

- Luftfrachtlogistik

- Keine Kühlkette

- Kühlkette

- Kühlkette nach Temperaturtyp

- Temperaturgesteuert

- Nicht temperaturgesteuert

- Kühlkette nach Temperaturtyp

- Überlandlogistik

- Keine Kühlkette

- Kühlkette

- Kühlkette nach Temperaturtyp

- Temperaturgesteuert

- Nicht temperaturgesteuert

- Kühlkette nach Temperaturtyp

Anwendung

- Diagnosegeräte

- Therapeutische Geräte

- Überwachungsgeräte

- Chirurgische Geräte

- Andere Geräte

Endverwendung

- Krankenhäuser und Kliniken

- Unternehmen für medizinische Geräte

- Akademisches und Forschungsinstitut

- Referenz- und Diagnostiklabor

- Unternehmen für Notfallmedizin

- Sonstiges

Vertriebskanal

- Konventionelle Logistik

- Dritte Seite

Regionale Analyse des Marktes für Lager und Logistik für medizinische Geräte

Der Markt wird analysiert und Erkenntnisse zur Marktgröße und zu Trends werden nach Angebot, Temperatur, Transportart, Anwendung, Endverbrauch und Vertriebskanal wie oben angegeben bereitgestellt.

Die vom Markt abgedeckten Länder sind die USA, Kanada, Mexiko, Deutschland, Großbritannien, Frankreich, Italien, Spanien, die Schweiz, die Niederlande, Russland, Belgien, Finnland, Dänemark, Polen, Norwegen, Schweden, Ungarn, das übrige Europa, China, Japan, Indien, Südkorea, Australien, Singapur, Malaysia, Thailand, Indonesien, die Philippinen, Neuseeland, Vietnam, Taiwan, der übrige asiatisch-pazifische Raum, Brasilien, Argentinien, das übrige Südamerika, Südafrika, Saudi-Arabien, die Vereinigten Arabischen Emirate, Israel, Ägypten, Kuwait, Oman, Bahrain sowie der übrige Nahe Osten und Afrika.

Aufgrund der steigenden Nachfrage von Krankenhäusern und Kliniken nach medizinischen Geräten und der weltweit zunehmenden Verwendung von Diagnosegeräten wird Nordamerika den Markt voraussichtlich dominieren.

Der Markt im asiatisch-pazifischen Raum wächst aufgrund des technologischen Fortschritts und der Innovationen in der Medizintechnik.

Der Länderabschnitt des Berichts enthält auch Angaben zu einzelnen marktbeeinflussenden Faktoren und Änderungen der Regulierung auf dem Inlandsmarkt, die sich auf die aktuellen und zukünftigen Trends des Marktes auswirken. Datenpunkte wie Downstream- und Upstream-Wertschöpfungskettenanalysen, technische Trends und Porters Fünf-Kräfte-Analyse sowie Fallstudien sind einige der Anhaltspunkte, die zur Prognose des Marktszenarios für einzelne Länder verwendet werden. Bei der Bereitstellung von Prognoseanalysen der Länderdaten werden auch die Präsenz und Verfügbarkeit globaler Marken und ihre Herausforderungen aufgrund großer oder geringer Konkurrenz durch lokale und inländische Marken sowie die Auswirkungen inländischer Zölle und Handelsrouten berücksichtigt.

Marktanteile im Lager- und Logistikbereich für medizinische Geräte

Die Wettbewerbslandschaft des Marktes liefert Einzelheiten zu den Wettbewerbern. Zu den enthaltenen Einzelheiten gehören Unternehmensübersicht, Unternehmensfinanzen, erzielter Umsatz, Marktpotenzial, Investitionen in Forschung und Entwicklung, neue Marktinitiativen, globale Präsenz, Produktionsstandorte und -anlagen, Produktionskapazitäten, Stärken und Schwächen des Unternehmens, Produkteinführung, Produktbreite und -umfang, Anwendungsdominanz. Die oben angegebenen Datenpunkte beziehen sich nur auf den Fokus der Unternehmen in Bezug auf den Markt.

Die auf dem Markt tätigen Marktführer im Bereich Lager und Logistik für medizinische Geräte sind:

- Deutsche Post AG (Deutschland)

- FedEx (USA)

- United Parcel Service of America, Inc. (USA)

- Kuehne+Nagel (Großbritannien)

- DB SCHENKER (Deutschland)

- Alloga (Großbritannien)

- AWL India Private Limited (Indien)

- CH Robinson Worldwide, Inc. (USA)

- CAVALIER LOGISTICS (USA)

- CEVA (Frankreich)

- Crown LSP Group (USA)

- Dimerco (Taiwan)

- DSV (Dänemark)

- FM Logistic (Frankreich)

- Hansa International (China)

- Hellmann Worldwide Logistics SE & Co. KG (Deutschland)

- Imperial (Südafrika)

- Mercury Business Services (USA)

- Movianto (Niederlande)

- Murphy Logistics (USA)

- OIA Global (USA)

- Omni Logistics, LLC (USA)

- puracon GmbH (Deutschland)

- Rhenus-Gruppe (Deutschland)

- SEKO (USA)

- TIBA (Spanien)

- Toll Holdings Limited (Australien)

- Lager überall (USA)

- XPO, Inc. (USA)

Neueste Entwicklungen im Lager- und Logistikmarkt für medizinische Geräte

- Im November 2023 eröffnete DHL Express offiziell seinen erweiterten Zentralasien-Hub in Hongkong und investierte 562 Millionen Euro, um seine Kapazitäten angesichts des wachsenden Welthandels zu erweitern. Der Hub, der für die Verbindung Asiens mit der Welt von entscheidender Bedeutung ist, steigerte seine Spitzenkapazität für die Abfertigung von Sendungen um fast 70 % und kann nun das Sechsfache des Volumens seit seiner Eröffnung im Jahr 2004 bewältigen. Diese Erweiterung unterstreicht das Engagement von DHL, das Wachstum der Kunden zu unterstützen und Hongkongs Status als wichtiger internationaler Luftverkehrsknotenpunkt zu festigen

- Im Dezember 2022 kündigte DHL Supply Chain eine Investition von 10,93 Millionen USD an, um seine Lagerkapazitäten in Nordtaiwan zu erweitern, insbesondere in den Bereichen Halbleiter, Biowissenschaften und Gesundheitswesen. Das neu eröffnete Taoyuan Distribution Center-Jian Guo erweitert die gesamte Lagerfläche von DHL in Taoyuan um 10.000 Quadratmeter auf 37.000 Quadratmeter. Diese Einrichtung verbessert die Konnektivität für effiziente Logistikabläufe und unterstützt das Ziel des Unternehmens, bis 2027 eine Gesamtfläche von 200.000 Quadratmetern in Taiwan zu erreichen.

- Im September 2024 führte FedEx die fdx-Plattform ein, eine datengesteuerte Handelslösung, die jetzt für US-Unternehmen verfügbar ist. Die Plattform nutzt das Netzwerk von FedEx, um das Kundenerlebnis durch Verbesserung des Nachfragewachstums, der Konversionsraten und der Auftragsabwicklungsoptimierung zu verbessern. Zu den bemerkenswerten Funktionen gehören vorausschauende Lieferschätzungen, Einblicke in die Nachhaltigkeit, Marken-Auftragsverfolgung und vereinfachte Rückgabeprozesse. Raj Subramaniam, CEO von FedEx, betonte während der Veranstaltung Dreamforce 2024 die Rolle der Plattform in intelligenteren Lieferketten

- Im März 2024 stellte UPS Healthcare UPS Supply Chain Symphony R vor, eine Cloud-basierte Plattform zur Integration und Verwaltung von Lieferkettendaten im Gesundheitswesen aus verschiedenen Betriebssystemen. Dieses Tool bietet Kunden im Gesundheitswesen vollständige Transparenz über ihre Logistik und ermöglicht es ihnen, fundierte Entscheidungen zu treffen, die Planung zu verbessern und genaue Prognosen zu erstellen. Durch die Verbesserung von Kontrolle, Effizienz und Transparenz unterstützt diese Plattform den dringenden Bedarf an optimierten Lieferketten im Gesundheitswesen. Kate Gutmann betonte ihr transformatives Potenzial bei der Optimierung globaler Abläufe und der Patientenversorgung

- Im September 2024 hat Kuehne+Nagel, ein führender Logistikdienstleister, ein neues temperaturgeregeltes Fulfillment-Center für Medtronic in Milton, Ontario, nur 50 km von Toronto entfernt, eröffnet. Die 25.000 Quadratmeter große Anlage wird medizinische Geräte an Krankenhäuser verteilen und beherbergt Medtronics Service-, Reparatur- und vorbeugende Wartungszentren für seine Geräte.

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.