美国自有品牌食品和饮料市场,按类别(无机和有机)、产品(自有品牌食品和自有品牌饮料)、分销渠道(基于商店的零售和非基于商店的零售)划分 - 行业趋势和预测到 2029 年。

市场定义和见解

自有品牌产品由合同或第三方制造商生产,并以零售商的品牌名称或通过许可协议销售。通常,零售商会指定自有品牌商品的所有信息,包括成分、包装和标签设计。商家还负责生产和运送产品到商店的费用。从其他公司购买其品牌的产品不属于此计划。

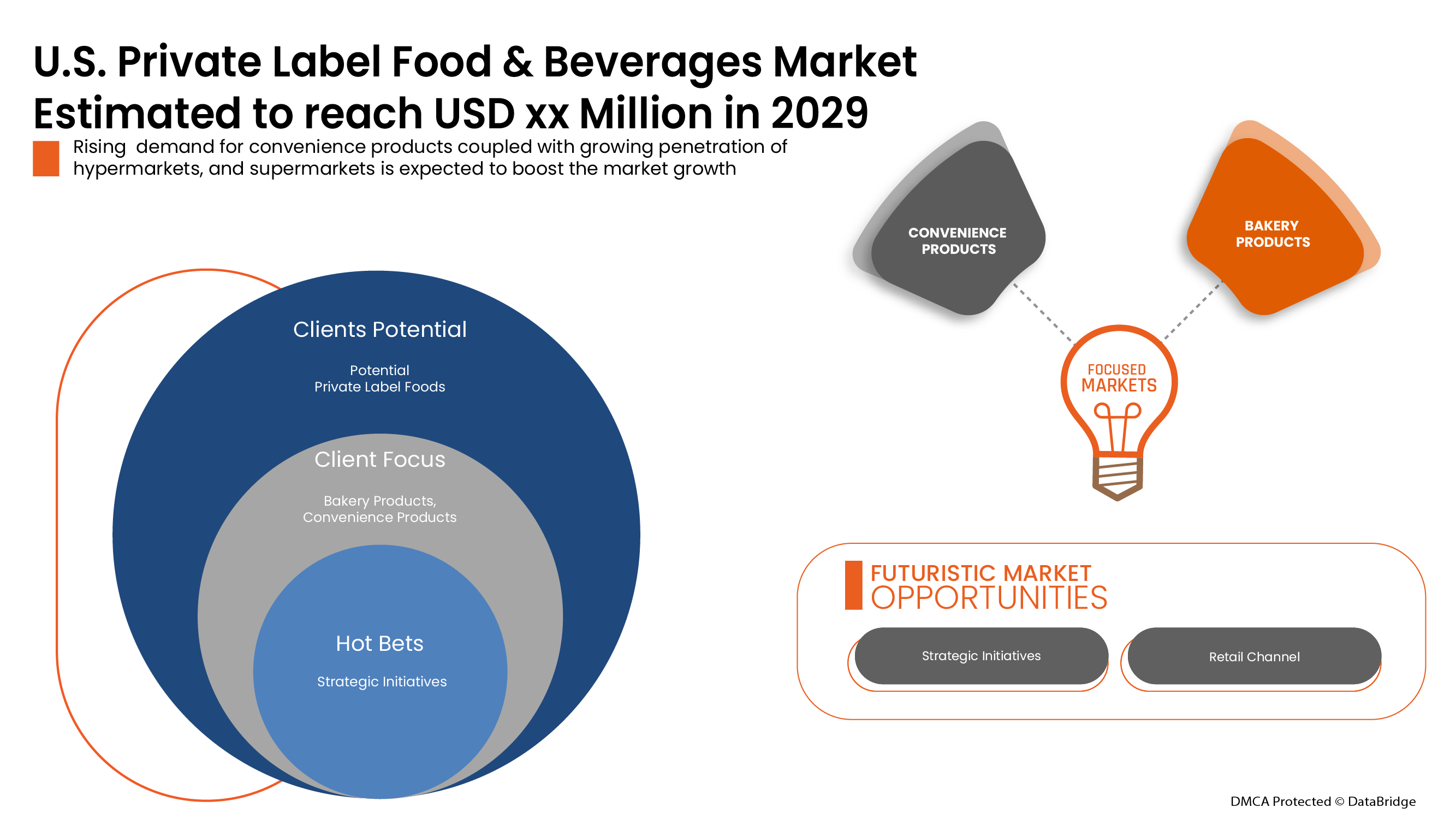

美国自有品牌食品和饮料市场预计将在 2022 年至 2029 年的预测期内实现市场增长。Data Bridge Market Research 分析称,在 2022 年至 2029 年的预测期内,该市场的复合年增长率为 5.4%,预计到 2029 年将达到 143,186.66 百万美元。

|

报告指标 |

细节 |

|

预测期 |

2022 至 2029 年 |

|

基准年 |

2020 |

|

历史岁月 |

2019(可定制为 2019 - 2014) |

|

定量单位 |

收入(百万美元),定价(美元) |

|

涵盖的领域 |

按类别(无机和有机)、产品(自有品牌食品和自有品牌饮料)、分销渠道(商店零售和非商店零售), |

|

覆盖国家 |

我们 |

|

涵盖的市场参与者 |

克罗格公司、沃尔玛、好市多批发商公司、艾伯森公司、塔吉特品牌公司、亚马逊公司等 |

自有品牌食品和饮料市场动态

驱动程序

- 便利产品需求不断增长

由于饮食习惯、生活方式和食物偏好的改变,尤其是年轻一代,对即食食品、汤和酱料、调味品和调味品、麦片和早餐麦片等方便食品的需求不断增加。即食食品包括几乎不需要或很少需要时间准备的冷冻披萨。然而,这些方便食品节省时间,但营养价值低,而且比传统食品更贵。

- 超市/大卖场渗透率不断提高

超市数量的增加是自有品牌食品和饮料市场的主要推动力之一。这是由于多种因素所致,其中许多因素与收入增加和城市化有关。随着超市数量的增加,它们倾向于推出自有品牌食品和饮料产品,以满足市场对食品和饮料产品的需求。

机会

- 罐装和冷冻肉类食品越来越受欢迎

生活方式的改变和人们繁忙的日程安排推动了罐装和冷冻肉制品的消费趋势。此外,随着 COVID-19 在全球的蔓延,消费者在封锁高峰期将冰箱里储存了保质期较长的食品,罐装和冷冻食品的需求也随之增加。

限制/挑战

- 跨国品牌在市场上占据主导地位

消费者对品牌产品至关重要。市场上成熟的品牌产品可能会阻碍自有品牌食品和饮料产品的增长。品牌产品的形象在决定选择什么消费时起着重要作用。与小型自有品牌食品和饮料制造商相比,主要参与者拥有完善的分销网络和强大的产品组合,产品经过认证的质量检查。调查显示,美国人,尤其是千禧一代,由于信任和质量问题,不愿意购买自有品牌食品和饮料。

这份美国自有品牌食品和饮料市场报告详细介绍了最新发展、贸易法规、进出口分析、生产分析、价值链优化、市场份额、国内和本地市场参与者的影响,分析了新兴收入来源、市场法规变化、战略市场增长分析、市场规模、类别市场增长、应用领域和主导地位、产品批准、产品发布、地域扩展、市场技术创新等方面的机会。如需了解有关美国自有品牌食品和饮料市场的更多信息,请联系 Data Bridge Market Research 获取分析师简报,我们的团队将帮助您做出明智的市场决策,实现市场增长。

新冠肺炎疫情对美国自有品牌食品和饮料市场的影响

COVID-19 疫情严重扰乱了食品和饮料产品原材料的供应链。COVID-19 病例不断增加,尤其是在美国各州,这引起了消费者的恐慌,因此人们不愿意出门购物;在此期间,人们只考虑购买必需的食品和饮料产品。

最新动态

- 2019 年 9 月,Kroger 推出了其 Simple Truth 自有品牌系列的植物基产品,包括无肉汉堡和植物基曲奇面团。该产品的推出帮助该公司扩大了其自有品牌在植物基类别中的份额。

- 2021 年 4 月,亚马逊公司推出了“Aplenty”旗下新的食品自有品牌。该产品的推出扩大了其在自有品牌食品领域的产品组合。

美国自有品牌食品和饮料市场范围

美国自有品牌食品和饮料市场分为类别、产品和分销渠道。这些细分市场之间的增长将帮助您分析行业中增长微弱的细分市场,并为用户提供有价值的市场概览和市场洞察,以便做出战略决策,确定核心市场应用。

类别

- 无机

- 有机的

根据类别,美国自有品牌食品和饮料市场分为无机和有机。

产品

- 自有品牌食品

- 自有品牌饮料

根据产品,美国自有品牌食品和饮料市场分为自有品牌食品和自有品牌饮料。

分销渠道

- 店铺零售

- 无店铺零售

根据分销渠道,美国自有品牌食品和饮料市场分为商店零售和非商店零售。

竞争格局和美国自有品牌食品和饮料市场份额分析

美国自有品牌食品和饮料市场竞争格局提供了竞争对手的详细信息。详细信息包括公司概况、公司财务状况、收入、市场潜力、研发投资、新市场计划、美国业务、生产基地和设施、生产能力、公司优势和劣势、产品发布、产品宽度和广度以及应用主导地位。以上提供的数据点仅与公司对市场的关注有关。

美国自有品牌食品和饮料市场的一些主要参与者包括 Loblaws Inc.、Sobey Inc.、Metro Richelieu Inc、沃尔玛、Costco Wholesale Corporation、Amazon.com, Inc. 等。

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析以及主要(行业专家)验证。除此之外,数据模型还包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、公司市场份额分析、测量标准、美国与地区以及供应商份额分析。如有进一步询问,请要求分析师致电。

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

目录

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 CATEGORY LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 SHOPPING BEHAVIOR

4.2 PERCEPTION TOWARDS PRIVATE LABEL

4.3 CONSUMER DEMOGRAPHICS

4.4 REGULATORY FRAMEWORK

4.5 COMPARATIVE ANALYSIS

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 GROWING DEMAND FOR CONVENIENCE PRODUCTS

5.1.2 RISING PENETRATION OF SUPERMARKETS/HYPERMARKETS

5.1.3 RISING DEMAND FOR BEVERAGES PRODUCTS

5.2 RESTRAINTS

5.2.1 DOMINANCE OF MULTINATIONAL BRANDS IN THE MARKET

5.2.2 DISTURBANCE IN SUPPLY CHAIN DUE TO COVID-19

5.3 OPPORTUNITIES

5.3.1 GROWING POPULARITY OF CANNED AND FROZEN MEAT FOOD

5.3.2 IMPROVED QUALITY AND DEVELOPMENT OF PREMIUM PRIVATE LABEL BRANDS

5.4 CHALLENGE

5.4.1 STRINGENT GOVERNMENT REGULATIONS

6 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY CATEGORY

6.1 OVERVIEW

6.2 INORGANIC

6.3 ORGANIC

7 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS

7.1 OVERVIEW

7.2 PRIVATE LABEL FOODS

7.2.1 CONVENIENCE PRODUCTS

7.2.1.1 MUESLI & BREAKFAST CEREALS

7.2.1.2 READY TO EAT MEALS

7.2.1.3 SOUPS & SAUCES

7.2.1.4 JAMS, PRESERVES & MARMALADE

7.2.1.5 SEASONING & DRESSING

7.2.1.6 OTHERS

7.2.2 BAKERY PRODUCTS

7.2.2.1 BREAD

7.2.2.2 DONUTS AND MUFFINS

7.2.2.3 BISCUITS AND COOKIES

7.2.2.4 CAKES & PASTRIES

7.2.2.5 OTHERS

7.2.3 MEAT & POULTRY PRODUCTS

7.2.4 DAIRY AND DAIRY ALTERNATIVE PRODUCTS

7.2.4.1 ICE-CREAM

7.2.4.2 YOGURT

7.2.4.3 FROZEN DESSERT

7.2.4.4 CHEESE

7.2.4.5 OTHERS

7.2.5 CONFECTIONERY PRODUCTS

7.2.5.1 CHOCOLATE

7.2.5.2 CANDIES

7.2.5.3 GUMMIES & MARSHMALLOWS

7.2.5.4 OTHERS

7.2.6 FRUITS AND VEGETABLES

7.2.6.1 APPLE

7.2.6.2 ORANGE

7.2.6.3 GRAPES

7.2.6.4 CAULIFLOWER

7.2.6.5 BROCCOLI

7.2.6.6 OTHERS

7.2.7 EGGS

7.2.8 NUTRITIONAL BARS

7.3 PRIVATE LABEL BEVERAGES

7.3.1 NON-ALCOHOLIC DRINKS

7.3.1.1 SOFT DRINKS

7.3.1.2 FLAVORED DRINKS

7.3.1.3 NATURAL WATER

7.3.1.4 FUNCTIONAL DRINKS

7.3.1.5 JUICES

7.3.1.6 ENERGY DRINKS

7.3.1.7 NATURAL & ORGANIC DRINKS

7.3.1.8 OTHERS

7.3.2 ALCOHOLIC DRINKS

7.3.2.1 VODKA

7.3.2.2 WHISKEY

7.3.2.3 RUM

7.3.2.4 OTHERS

8 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY DISTRIBUTION CHANNEL

8.1 OVERVIEW

8.2 STORE-BASED RETAILING

8.2.1 SUPERMARKET & HYPERMARKETS

8.2.2 FOOD & DRINKS SPECIALISTS

8.2.3 CONVENIENCE STORES

8.2.4 DEPARTMENT STORES

8.2.5 OTHERS

8.3 NON-STORE-BASED RETAILING

8.3.1 ONLINE

8.3.2 VENDING

9 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY COUNTRY

9.1 U.S.

10 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: COMPANY LANDSCAPE

10.1 COMPANY SHARE ANALYSIS: U.S.

11 SWOT ANALYSIS

12 COMPANY PROFILE

12.1 THE KROGER CO.

12.1.1 COMPANY SNAPSHOT

12.1.2 REVENUS ANALYSIS

12.1.3 PRODUCT PORTFOLIO

12.1.4 RECENT DEVELOPMENTS

12.2 WALMART

12.2.1 COMPANY SNAPSHOT

12.2.2 REVENUS ANALYSIS

12.2.3 PRODUCT PORTFOLIO

12.2.4 RECENT DEVELOPMENT

12.3 COSTCO WHOLESALE CORPORATION

12.3.1 COMPANY SNAPSHOT

12.3.2 REVENUS ANALYSIS

12.3.3 PRODUCT PORTFOLIO

12.3.4 RECENT DEVELOPMENT

12.4 ALBERTSONS COMPANIES

12.4.1 COMPANY SNAPSHOT

12.4.2 REVENUS ANALYSIS

12.4.3 PRODUCT PORTFOLIO

12.4.4 RECENT DEVELOPMENT

12.5 TARGET BRAND, INC.

12.5.1 COMPANY SNAPSHOT

12.5.2 REVENUS ANALYSIS

12.5.3 PRODUCT PORTFOLIO

12.5.4 RECENT DEVELOPMENT

12.6 AMAZON.COM, INC

12.6.1 COMPANY SNAPSHOT

12.6.2 REVENUS ANALYSIS

12.6.3 PRODUCT PORTFOLIO

12.6.4 RECENT DEVELOPMENT

12.7 JAVO BEVERAGE COMPANY, INC

12.7.1 COMPANY SNAPSHOT

12.7.2 PRODUCT PORTFOLIO

12.7.3 RECENT DEVELOPMENT

12.8 DALMAR FOODS

12.8.1 COMPANY SNAPSHOT

12.8.2 PRODUCT PORTFOLIO

12.8.3 RECENT DEVELOPMENT

12.9 GIANT EAGLE, INC.

12.9.1 COMPANY SNAPSHOT

12.9.2 PRODUCT PORTFOLIO

12.9.3 RECENT DEVELOPMENT

12.1 GRAND RIVER FOODS LTD

12.10.1 COMPANY SNAPSHOT

12.10.2 PRODUCT PORTFOLIO

12.10.3 RECENT DEVELOPMENT

12.11 LOBLAWS INC.

12.11.1 COMPANY SNAPSHOT

12.11.2 REVENUS ANALYSIS

12.11.3 PRODUCT PORTFOLIO

12.11.4 RECENT DEVELOPMENT

12.12 KARLIN FOODS

12.12.1 COMPANY SNAPSHOT

12.12.2 PRODUCT PORTFOLIO

12.12.3 RECENT UPDATE

12.13 SOBEYS INC.

12.13.1 COMPANY SNAPSHOT

12.13.2 REVENUE ANALYSIS

12.13.3 PRODUCT PORTFOLIO

12.13.4 RECENT DEVELOPMENT

12.14 KINGMAKER FOODS

12.14.1 COMPANY SNAPSHOT

12.14.2 PRODUCT PORTFOLIO

12.14.3 RECENT UPDATE

12.15 METRO RICHELIEU INC

12.15.1 COMPANY SNAPSHOT

12.15.2 REVENUE ANALYSIS

12.15.3 PRODUCT PORTFOLIO

12.15.4 RECENT DEVELOPMENT

13 QUESTIONARE:

14 RELATED REPORTS

表格列表

TABLE 1 CONSUMER DEMOGRAPHICS IN THE U.S., 2019-2020, BY HOUSEHOLDS, IN THOUSANDS

TABLE 2 CONSUMER DEMOGRAPHICS IN THE U.S., 2019-2020, BY AGE OF HOUSEHOLDER, IN THOUSANDS

TABLE 3 CONSUMER DEMOGRAPHICS IN THE U.S., 2019-2020, BY EDUCATIONAL ATTAINMENT OF HOUSEHOLDER, IN THOUSANDS

TABLE 4 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY CATEGORY, 2020-2029 (USD MILLION)

TABLE 5 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 6 U.S. PRIVATE LABEL FOODS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY-PRODUCTS, 2020-2029 (USD MILLION)

TABLE 7 U.S. CONVENIENCE PRODUCTS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 8 U.S. BAKERY PRODUCTS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 9 U.S. DAIRY AND DAIRY ALTERNATIVE PRODUCTS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 10 U.S. CONFECTIONERY PRODUCTS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 11 U.S. FRUITS & VEGETABLES IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 12 U.S. PRIVATE LABEL BEVERAGES IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 13 U.S. NON-ALCOHOLIC DRINKS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 14 U.S. ALCOHOLIC DRINKS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 15 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 16 U.S. STORE-BASED RETAILING IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 17 U.S. NON-STORE-BASED RETAILING IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 18 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY CATEGORY, 2020-2029 (USD MILLION)

TABLE 19 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 20 U.S. PRIVATE LABEL FOODS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 21 U.S. BAKERY PRODUCTS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 22 U.S. FRUIT & VEGETABLES IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS 2020-2029 (USD MILLION)

TABLE 23 U.S. CONFECTIONERY PRODUCTS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 24 U.S. DAIRY AND DAIRY ALTERNATIVES PRODUCTS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 25 U.S. CONVENIENCE PRODUCTS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 26 U.S. PRIVATE LABEL BEVERAGES IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 27 U.S. NON-ALCOHOLIC DRINK IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 28 U.S. ALCOHOLIC DRINKS IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY PRODUCTS, 2020-2029 (USD MILLION)

TABLE 29 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 30 U.S. STORE-BASED RETAILING IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 31 U.S. NON-STORE-BASED RETAILING IN PRIVATE LABEL FOOD AND BEVERAGES MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

图片列表

FIGURE 1 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: SEGMENTATION

FIGURE 2 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: DATA TRIANGULATION

FIGURE 3 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: DROC ANALYSIS

FIGURE 4 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: COUNTRY VS REGIONAL MARKET ANALYSIS

FIGURE 5 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: DBMR MARKET POSITION GRID

FIGURE 8 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: SEGMENTATION

FIGURE 9 GROWING DEMAND FOR CONVENIENCE PRODUCTS IS EXPECTED TO DRIVE THE U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 10 INORGANIC CATEGORY SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET IN 2022 & 2029

FIGURE 11 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGE OF THE U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET

FIGURE 12 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET: BY CATEGORY, 2021

FIGURE 13 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET: BY PRODUCTS, 2021

FIGURE 14 U.S. PRIVATE LABEL FOOD AND BEVERAGES MARKET: BY DISTRIBUTION CHANNEL, 2021

FIGURE 15 U.S. PRIVATE LABEL FOOD AND BEVERAGE MARKET: COMPANY SHARE 2021 (%)

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。