全球金属加工液添加剂市场,按添加剂类型(表面活性剂添加剂和乳化剂、腐蚀抑制剂、极压添加剂、稳定剂、消泡剂、醇胺、防雾剂、着色剂/染料等)、应用(可溶性油、直油、半合成液和合成液)、金属加工活动(铣削、钻孔、磨削、珩磨、攻丝等)、最终用途(汽车、航空航天、机械和设备制造、电力和能源、海洋等)划分——行业趋势和预测到 2030 年。

金属加工液添加剂市场分析与洞察

汽车、航空航天和机械行业的不断扩张是推动市场扩张的关键因素。质量标准的不断提高和行业内自动化程度的不断提高有助于促进市场增长的机会。

各行业越来越多地采用干式加工,这对市场产生了显著的限制。此外,原材料价格和供应的波动对市场增长构成了巨大挑战。转向环保添加剂似乎是一个新兴的机会,有可能推动市场增长。环境法规和可持续性因素已成为影响市场增长轨迹的重大挑战。

全球金属加工液添加剂市场报告提供了市场份额、新发展和产品线分析的详细信息,国内和本地市场参与者的影响,分析了新兴收入领域、市场法规变化、产品审批、战略决策、产品发布、地域扩张和市场技术创新方面的机会。要了解分析和市场情况,请联系我们获取分析师简报,我们的团队将帮助您创建收入影响解决方案,以实现您的预期目标。

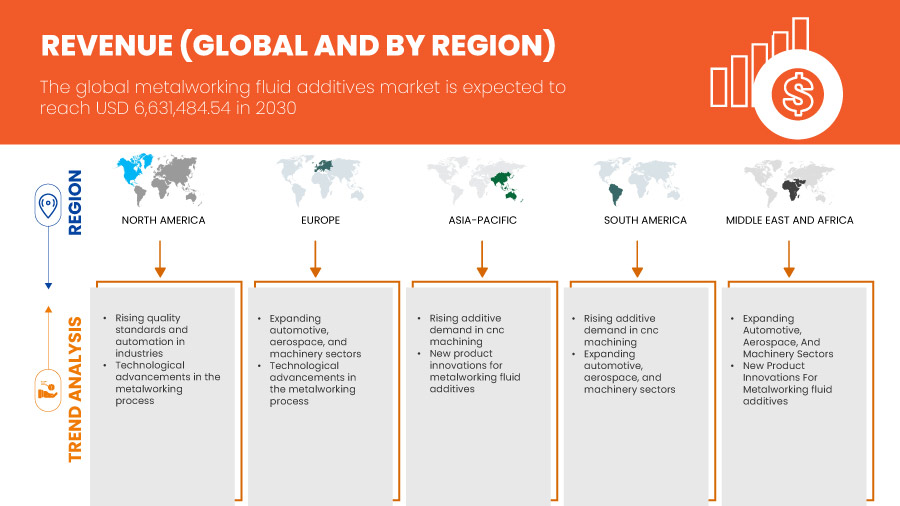

全球金属加工液添加剂市场预计将在 2023 年至 2030 年的预测期内实现市场增长。Data Bridge Market Research 分析称,在 2023 年至 2030 年的预测期内,该市场的复合年增长率为 4.3%,预计到 2030 年将达到 6,631,484.54 万美元。数控加工中添加剂需求的不断增长是预计推动市场增长的一些驱动因素。

|

报告指标 |

细节 |

|

预测期 |

2023 至 2030 年 |

|

基准年 |

2022 |

|

历史岁月 |

2021 (可定制为 2015-2020) |

|

定量单位 |

收入(千美元) |

|

涵盖的领域 |

添加剂类型(表面活性剂添加剂和乳化剂、腐蚀抑制剂、极压添加剂、稳定剂、消泡剂、醇胺、防雾剂、着色剂/染料等)、应用(可溶性油、直油、半合成流体和合成流体)、金属加工活动(铣削、钻孔、磨削、珩磨、攻丝等)、最终用途(汽车、航空航天、机械和设备制造、电力和能源、船舶等) |

|

覆盖国家 |

美国、加拿大、墨西哥、德国、法国、西班牙、英国、意大利、俄罗斯、比利时、荷兰、土耳其、瑞典、瑞士、丹麦、挪威、芬兰、欧洲其他地区、中国、印度、日本、韩国、新加坡、澳大利亚、台湾、泰国、印度尼西亚、马来西亚、香港、新西兰、菲律宾、亚太其他地区、巴西、阿根廷、南美洲其他地区、沙特阿拉伯、埃及、南非、卡塔尔、阿联酋、以色列、阿曼、科威特、巴林以及中东和非洲其他地区 |

|

涵盖的市场参与者 |

路博润公司、陶氏、赢创工业股份公司、福斯、索尔维、朗盛、英国石油公司、科莱恩、Ingevity 及其相关实体、亚什兰、意特麦琪化工公司、花王株式会社、优美科、Colonial Chemical、Biosynthetic Technologies、都佛化学公司、Emery Oleochemicals、Pilot Chemical Corp.、RT Vanderbilt Holding Company, Inc. 和 ZSCHIMMER & SCHWARZ, INC. |

市场定义

金属加工液添加剂 (PFPE) 是一种低分子量氟化合成液。金属加工液添加剂在自然状态下无毒且不易燃。它可在 80°C 至 200°C 的极端温度下使用。PFPE 的分子结构可能是线性、支链或两者的组合,具体取决于应用。耐高温、润滑性、耐磨性和流体挥发性均由 PFPE 提供。

全球金属加工液添加剂市场动态

驱动程序

- 扩大汽车、航空航天和机械行业

在全球市场,汽车、航空航天和机械等重要行业领域的快速增长和扩张推动了对金属加工液添加剂的需求。这些行业代表了整个现代制造业,不断突破创新和技术发展的界限。

汽车行业是全球经济的支柱,该行业一直在寻找提高车辆性能、安全性和效率的方法。为了生产精密部件,该活动需要复杂的加工程序。金属加工液添加剂通过提供润滑、冷却和排屑功能,在保证平稳运行和生产高质量汽车零件方面发挥着至关重要的作用。

- 工业质量标准和自动化水平不断提高

质量标准的升级和行业内自动化程度的不断提高,有助于促进市场增长的机会。这两个因素共同引发了制造业的范式转变,并正在重塑对金属加工液添加剂的需求动态。提高质量标准已成为现代制造工艺中的重中之重。行业面临着保持精度、一致性和遵守严格规范的压力,以确保产品的完整性和性能。金属加工液添加剂在实现这些目标方面发挥着关键作用。增强润滑、冷却和防腐性能的添加剂已成为优化加工工艺、提高工具寿命和实现卓越产品表面效果的必要条件。随着各个行业的行业都努力达到或超过这些质量基准,对先进金属加工液添加剂的需求将会增加,从而促进市场增长。

机会

- 金属加工工艺的技术进步

技术进步已成为市场增长的关键驱动力。这些技术发展极大地影响了金属加工液添加剂的配方、应用和性能,为市场扩张创造了大量机会。

技术进步的一个关键领域是添加剂配方的改进。制造商正在利用尖端研究和创新来开发具有卓越润滑、防腐和冷却性能的添加剂。这种精密设计的添加剂可增强加工工艺、延长刀具寿命并有助于提高成品质量。这种性能优化水平为最终用户创造了引人注目的价值主张,推动了对金属加工液添加剂的需求。此外,纳米技术的进步为提高金属加工液添加剂的效率开辟了新途径。纳米颗粒由于其独特的性能,可以为金属加工液赋予增强的润滑、传热和抗磨特性。

- 转向环保添加剂

市场正在经历一场变革,推动力是人们越来越重视环境可持续性。随着各行各业都在努力减少生态足迹,在金属加工过程中采用环保添加剂已成为影响市场发展轨迹的关键驱动力。

长期以来,传统金属加工液添加剂领域一直以含有石油基化合物和添加剂的配方为主,这些配方可能存在健康和环境风险。然而,随着人们对这些危害的认识不断提高,再加上严格的法规和消费者对可持续产品的需求不断增长,人们开始转向更环保的替代品。

限制/挑战

- 转向传统干式加工的行业

各行各业越来越多地采用干式加工,这对市场产生了显著的限制。干式加工是一种在加工过程中几乎不使用冷却剂或润滑剂的技术,由于其具有降低成本、环保和改善工作条件的潜力而受到青睐。这种转变并非没有挑战,其影响在市场上回荡。

推动转向干式加工的主要因素之一是潜在的成本节约。传统的金属加工液以及相关添加剂需要采购、维护和处理。干式加工可消除这些成本,使其成为注重成本的行业的理想选择。此外,干式加工可减少废物产生,简化废物处理并有助于实现更精简的制造流程。

- 原材料价格波动

这一因素与经济、地缘政治和供应链动态密切相关,直接影响生产成本、定价和市场的整体稳定性。金属加工液添加剂采用多种关键原材料组合配制而成,包括基础油、添加剂包(包括极压剂、抗磨化合物、消泡剂、腐蚀抑制剂)以及乳化剂、杀菌剂和溶剂等特种化学品。

这些成分共同增强了金属加工液的润滑、冷却、耐腐蚀和整体性能,对加工过程产生至关重要的影响。该配方的组成适用于特定的应用和加工要求,使其成为适用于一系列金属加工操作的多功能解决方案。由此,我们可以推断,基础油、添加剂和特种化学品等原材料构成了金属加工液添加剂成本结构的很大一部分。市场对这些原材料价格波动的敏感性是地缘政治紧张局势、供需动态变化和全球贸易路线中断等因素的结果。价格的快速变化可能导致制造商成本不可预测地上涨,从而对利润率造成压力。这种波动不仅增加了运营的不确定性,而且还妨碍了向最终用户提供有竞争力的价格的能力。

- 涉及的环境法规和可持续性因素

环境法规和可持续性因素已成为影响市场增长轨迹的重大挑战。这些因素源于全球越来越关注减少工业流程对环境的影响并遵循可持续做法。

这种法规合规性挑战可能会提高进入门槛并增加运营复杂性,从而阻碍市场增长。此外,可持续发展的必要性正在推动各行各业采用更环保的做法,影响金属加工液添加剂的选择。最终用户现在要求符合其可持续发展目标的环保添加剂。生物降解性、低毒性和可再生来源正成为添加剂选择的关键标准。这种转变对制造商重新配制产品提出了挑战,通常需要在研发方面投入大量资金。在性能和可持续性之间取得平衡进一步增加了复杂性,可能会减缓市场扩张,因为制造商正在努力满足这些新需求。

总之,环境法规和可持续性因素给市场带来了错综复杂的挑战。不断变化的监管环境、与可持续性目标保持一致的需要、对环保包装的需求以及循环经济概念的出现,共同对制造商在合规性、配方、成本和创新方面提出了挑战。成功应对这些挑战需要战略调整并专注于对环境负责的解决方案,这预计将对市场增长构成挑战。

最新动态

- 2023 年 8 月,Boecore 选择科罗拉多斯普林斯进行扩张,其动力来自网络安全专业知识。在阿拉巴马州亨茨维尔和犹他州韦伯县的考虑中,增长激励和航空航天生态系统增强了科罗拉多州的吸引力

- 2023 年 7 月,Godrej Aerospace 在印度的太空任务中发挥了至关重要的作用,为 Chandrayaan-3 提供零部件。该公司的专业知识展示了其对航空航天进步和创新的承诺,支持太空探索和商业航空业

- 2023 年 6 月,据 BBC 报道,OPEC 控制着全球近 40% 的石油储备供应。除了 2003 年 4 月的减产外,沙特阿拉伯和其他 OPEC+ 产油国还宣布进一步削减石油产量约 116 万桶/日。OPEC 可以影响全球石油供应,从而影响全球石油和天然气价格,最终影响以原油为原料的产品成本

- 2023 年 7 月,根据 LNG 发表的一篇文章,欧洲化学品管理局提议对中链氯化石蜡和其他含有碳链长度为 C14 至 C17 的氯烷的物质实行为期七年的过渡期。该限制旨在评估这些物质的制造、使用或贸易对人类健康或环境的潜在风险。中链氯化石蜡用于金属加工液中,作为高难度操作的极压剂,保护工具和部件免受高速和高压下的摩擦、磨损和过热

全球金属加工液添加剂市场范围

根据添加剂类型、应用、金属加工活动和最终用途,全球金属加工液添加剂市场可分为四个显著的细分市场。细分市场之间的增长有助于您分析利基增长领域和进入市场的策略,并确定您的核心应用领域和目标市场的差异。

添加剂类型

- 表面活性剂添加剂和乳化剂

- 腐蚀抑制剂

- 极压添加剂

- 稳定剂

- 消泡剂

- 醇胺

- 防雾剂

- 着色剂/染料

- 其他的

根据添加剂类型,市场分为表面活性剂添加剂和乳化剂、腐蚀抑制剂、极压添加剂、稳定剂、消泡剂、醇胺、防雾剂、着色剂/染料等。

应用

- 可溶性油

- 纯油

- 半合成流体

- 合成液体

根据应用,市场分为可溶性油、直馏油、半合成流体和合成流体。

金属加工活动

- 铣削

- 钻孔

- 研磨

- 珩磨

- 窃听

- 其他的

根据金属加工活动,市场分为铣削、钻孔、磨削、珩磨、攻丝等。

最终用途

- 汽车

- 航天

- 机械设备制造业

- 电力和能源

- 海洋

- 其他的

根据最终用途,市场细分为汽车、航空航天、机械和设备制造、电力和能源、海洋和其他。

全球金属加工液添加剂市场区域分析

对全球金属加工液添加剂市场进行了分析,并提供了上述添加剂类型、应用、金属加工活动和最终用途的市场规模信息。

本市场报告涵盖的国家包括美国、加拿大、墨西哥、德国、法国、西班牙、英国、意大利、俄罗斯、比利时、荷兰、土耳其、瑞典、瑞士、丹麦、挪威、芬兰、欧洲其他地区、中国、印度、日本、韩国、新加坡、澳大利亚、台湾、泰国、印度尼西亚、马来西亚、香港、新西兰、菲律宾、亚太其他地区、巴西、阿根廷、南美洲其他地区、沙特阿拉伯、埃及、南非、卡塔尔、阿联酋、以色列、阿曼、科威特、巴林以及中东和非洲其他地区

由于亚太地区工业化进程迅速,制造业需求旺盛,预计该地区将占据市场主导地位。中国是该地区增长最快的国家,拥有强大的工业基础、强劲的制造业和对金属加工液的高需求。北美的美国是该地区增长最快的国家,因为其制造业发展迅速、汽车行业不断扩张,金属加工活动不断增加。欧洲的德国凭借完善的制造业基础设施和先进的技术,占据了市场主导地位。

报告的国家部分还提供了影响市场当前和未来趋势的各个市场影响因素和国内市场监管变化。新销售、替代销售、国家人口统计、监管法案和进出口关税等数据点是用于预测各个国家市场情景的一些主要指标。此外,在对国家数据进行预测分析时,还考虑了全球品牌的存在和可用性以及它们因来自本地和国内品牌的激烈或稀缺竞争而面临的挑战,以及销售渠道的影响。

竞争格局和全球金属加工液添加剂市场份额分析

全球金属加工液添加剂市场竞争格局提供了竞争对手的详细信息。详细信息包括公司概况、公司财务状况、产生的收入、市场潜力、研发投资、新市场计划、全球影响力、生产基地和设施、公司优势和劣势、产品发布、临床试验渠道、品牌分析、产品批准、专利、产品宽度和广度、应用优势、技术生命线曲线。以上提供的数据点仅与公司对市场的关注有关。

本报告涉及的主要参与者包括路博润公司、陶氏化学、赢创工业股份公司、福斯、索尔维、朗盛、英国石油公司、科莱恩、Ingevity 及其相关实体、亚什兰、意特麦琪化工公司、花王公司、优美科、Colonial Chemical、Biosynthetic Technologies、都佛化学公司、Emery Oleochemicals、Pilot Chemical Corp.、RT Vanderbilt Holding Company, Inc. 和 ZSCHIMMER & SCHWARZ, INC. 等。

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

目录

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE GLOBAL METALWORKING FLUID ADDITIVES MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 MARKET END USE COVERAGE GRID

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 EXPANDING AUTOMOTIVE, AEROSPACE, AND MACHINERY SECTORS

5.1.2 RISING QUALITY STANDARDS AND AUTOMATION IN INDUSTRIES

5.1.3 RISING ADDITIVE DEMAND IN CNC MACHINING

5.2 RESTRAINTS

5.2.1 SUPPLY CHAIN DISRUPTIONS IN THE METALWORKING FLUID ADDITIVES MARKET

5.2.2 INDUSTRIES SHIFTING TO TRADITIONAL DRY MACHINING

5.2.3 FLUCTUATION IN RAW MATERIAL PRICES

5.3 OPPORTUNITIES

5.3.1 TECHNOLOGICAL ADVANCEMENTS IN THE METALWORKING PROCESS

5.3.2 SHIFT TOWARD ECO-FRIENDLY ADDITIVES

5.3.3 NEW PRODUCT INNOVATIONS FOR METALWORKING FLUID ADDITIVES

5.4 CHALLENGES

5.4.1 ENVIRONMENTAL REGULATIONS AND SUSTAINABILITY FACTORS INVOLVED

5.4.2 STABILITY ASSOCIATED WITH METALFORMING FLUID ADDITIVES

6 GEOGRAPHICAL ANALYSIS

6.1 GLOBAL

6.2 EUROPE

6.3 ASIA PACIFIC

6.4 NORTH AMERICA

6.5 MIDDLE EAST AND AFRICA

6.6 SOUTH AMERICA

7 GLOBAL METALWORKING FLUID ADDITIVES MARKET: COMPANY LANDSCAPE

7.1 COMPANY SHARE ANALYSIS: GLOBAL

7.2 COMPANY SHARE ANALYSIS: EUROPE

7.3 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

7.4 COMPANY SHARE ANALYSIS: NORTH AMERICA

7.5 PARTNERSHIPS & CONTRACTS

7.6 EVENT

7.7 AWARD

8 SWOT ANALYSIS

9 COMPANY PROFILES

9.1 THE LUBRIZOL CORPORATION

9.1.1 COMPANY SNAPSHOT

9.1.2 COMPANY SHARE ANALYSIS

9.1.3 PRODUCT PORTFOLIO

9.1.4 RECENT DEVELOPMENT

9.2 EVONIK INDUSTRIES AG

9.2.1 COMPANY SNAPSHOT

9.2.2 REVENUE ANALYSIS

9.2.3 COMPANY SHARE ANALYSIS

9.2.4 PRODUCT PORTFOLIO

9.2.5 RECENT DEVELOPMENT

9.3 DOW

9.3.1 COMPANY SNAPSHOT

9.3.2 REVENUE ANALYSIS

9.3.3 COMPANY SHARE ANALYSIS

9.3.4 PRODUCT PORTFOLIO

9.3.5 RECENT DEVELOPMENT

9.4 FUCHS

9.4.1 COMPANY SNAPSHOT

9.4.2 REVENUE ANALYSIS

9.4.3 COMPANY SHARE ANALYSIS

9.4.4 PRODUCT PORTFOLIO

9.4.5 RECENT DEVELOPMENT

9.5 SOLVAY

9.5.1 COMPANY SNAPSHOT

9.5.2 REVENUE ANALYSIS

9.5.3 COMPANY SHARE ANALYSIS

9.5.4 PRODUCT PORTFOLIO

9.5.5 RECENT DEVELOPMENT

9.6 ASHLAND

9.6.1 COMPANY SNAPSHOT

9.6.2 REVENUE ANALYSIS

9.6.3 PRODUCT PORTFOLIO

9.6.4 RECENT DEVELOPMENT

9.7 BIOSYNTHETIC TECHNOLOGIES

9.7.1 COMPANY SNAPSHOT

9.7.2 PRODUCT PORTFOLIO

9.7.3 RECENT DEVELOPMENTS

9.8 BP P.L.C.

9.8.1 COMPANY SNAPSHOT

9.8.2 REVENUE ANALYSIS

9.8.3 PRODUCT PORTFOLIO

9.8.4 RECENT DEVELOPMENT

9.9 CLARIANT

9.9.1 COMPANY SNAPSHOT

9.9.2 REVENUE ANALYSIS

9.9.3 PRODUCT PORTFOLIO

9.9.4 RECENT DEVELOPMENTS

9.1 COLONIAL CHEMICAL

9.10.1 COMPANY SNAPSHOT

9.10.2 PRODUCT PORTFOLIO

9.10.3 RECENT DEVELOPMENT

9.11 DOVER CHEMICAL CORPORATION

9.11.1 COMPANY SNAPSHOT

9.11.2 PRODUCT PORTFOLIO

9.11.3 RECENT DEVELOPMENT

9.12 EMERY OLEOCHEMICALS

9.12.1 COMPANY SNAPSHOT

9.12.2 PRODUCT PORTFOLIO

9.12.3 RECENT DEVELOPMENT

9.13 INGEVITY AND ITS RELATED ENTITIES

9.13.1 COMPANY SNAPSHOT

9.13.2 REVENUE ANALYSIS

9.13.3 PRODUCT PORTFOLIO

9.13.4 RECENT DEVELOPMENT

9.14 ITALMATCH CHEMICALS S.P.A

9.14.1 COMPANY SNAPSHOT

9.14.2 REVENUE ANALYSIS

9.14.3 PRODUCT PORTFOLIO

9.14.4 RECENT DEVELOPMENT

9.15 KAO CORPORATION

9.15.1 COMPANY SNAPSHOT

9.15.2 REVENUE ANALYSIS

9.15.3 PRODUCT PORTFOLIO

9.15.4 RECENT DEVELOPMENT

9.16 LANXESS

9.16.1 COMPANY SNAPSHOT

9.16.2 REVENUE ANALYSIS

9.16.3 PRODUCT PORTFOLIO

9.16.4 RECENT DEVELOPMENT

9.17 PILOT CHEMICAL

9.17.1 COMPANY SNAPSHOT

9.17.2 PRODUCT PORTFOLIO

9.17.3 RECENT DEVELOPMENT

9.18 R.T. VANDERBILT HOLDING COMPANY, INC.

9.18.1 COMPANY SNAPSHOT

9.18.2 PRODUCT PORTFOLIO

9.18.3 RECENT DEVELOPMENT

9.19 UMICORE

9.19.1 COMPANY SNAPSHOT

9.19.2 REVENUE ANALYSIS

9.19.3 PRODUCT PORTFOLIO

9.19.4 RECENT DEVELOPMENT

9.2 ZSCHIMM ER & SCHWARZ, INC.

9.20.1 COMPANY SNAPSHOT

9.20.2 PRODUCT PORTFOLIO

9.20.3 RECENT DEVELOPMENT

10 QUESTIONNAIRE

11 RELATED REPORTS

图片列表

FIGURE 1 GLOBAL METALWORKING FLUID ADDITIVES MARKET: SEGMENTATION

FIGURE 2 GLOBAL METALWORKING FLUID ADDITIVES MARKET: DATA TRIANGULATION

FIGURE 3 GLOBAL METALWORKING FLUID ADDITIVES MARKET: DROC ANALYSIS

FIGURE 4 GLOBAL METALWORKING FLUID ADDITIVES MARKET: GLOBAL VS REGIONAL MARKET ANALYSIS

FIGURE 5 GLOBAL METALWORKING FLUID ADDITIVES MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 GLOBAL METALWORKING FLUID ADDITIVES MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 GLOBAL METALWORKING FLUID ADDITIVES MARKET: DBMR MARKET POSITION GRID

FIGURE 8 GLOBAL METALWORKING FLUID ADDITIVES MARKET: MARKET END USE COVERAGE GRID

FIGURE 9 GLOBAL METALWORKING FLUID ADDITIVES MARKET: SEGMENTATION

FIGURE 10 STRONG SPENDING TOWARDS PHARMA INDUSTRY IS DRIVING THE GROWTH OF THE GLOBAL METALWORKING FLUID ADDITIVES MARKET IN THE FORECAST PERIOD

FIGURE 11 THE SURFACTANT ADDITIVES AND EMULSIFIERS SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE GLOBAL METALWORKING FLUID ADDITIVES MARKET IN 2023 AND 2030

FIGURE 12 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE GLOBAL METALWORKING FLUID ADDITIVES MARKET

FIGURE 13 GLOBAL METALWORKING FLUID ADDITIVES MARKET: SNAPSHOT (2022)

FIGURE 14 EUROPA METALWORKING FLUID ADDITIVES MARKET: SNAPSHOT (2022)

FIGURE 15 ASIA PACIFIC METALWORKING FLUID ADDITIVES MARKET: SNAPSHOT (2022)

FIGURE 16 NORTH AMERICA METALWORKING FLUID ADDITIVES MARKET: SNAPSHOT (2022)

FIGURE 17 MIDDLE EAST AND AFRICA METALWORKING FLUID ADDITIVES MARKET: SNAPSHOT (2022)

FIGURE 18 SOUTH AMERICA METALWORKING FLUID ADDITIVES MARKET: SNAPSHOT (2022)

FIGURE 19 GLOBAL METALWORKING FLUID ADDITIVES MARKET: COMPANY SHARE 2022 (%)

FIGURE 20 EUROPE METALWORKING FLUID ADDITIVES MARKET: COMPANY SHARE 2022 (%)

FIGURE 21 ASIA-PACIFC METALWORKING FLUID ADDITIVES MARKET: COMPANY SHARE 2022 (%)

FIGURE 22 NORTH AMERICA METALWORKING FLUID ADDITIVES MARKET: COMPANY SHARE 2022 (%)

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。