欧洲可持续航空燃料市场,按燃料类型(生物燃料、氢燃料和动力转液体燃料)、制造技术(加氢脂肪酸酯和脂肪酸 - 合成石蜡煤油(HEFA-SPK)、费托合成石蜡煤油(FT-SPK)、发酵加氢糖合成异石蜡(HFS-SIP)、含芳烃的费托(FT)合成石蜡煤油(FT-SPK/A)、酒精转喷射 SPK(ATJ-SPK)和催化水热解喷射(CHJ))、混合能力(低于 30%、30% 至 50% 和高于 50%)、混合平台(商用航空、军用航空、商务和通用航空以及无人机)行业趋势和预测到 2029 年。

欧洲可持续航空燃料市场分析和规模

航空业热衷于减少碳足迹,以实现可持续的环境并满足严格的排放监管标准。航空业的各利益相关者正在采用替代解决方案,例如通过设计修改提高航空发动机效率、混合动力和全电动飞机、可再生喷气燃料等。然而,在这些解决方案中,与其他解决方案相比,采用可持续航空燃料(如电子燃料、合成燃料、绿色喷气燃料、生物喷气燃料、氢燃料)是社会和经济效益最可行的替代解决方案之一,它对减轻航空业当前和未来预期的环境影响做出了重大贡献。

可持续航空燃料是履行航空业承诺将碳排放增长与交通增长脱钩的关键要素。航空乘客数量增加、可支配收入增加、航空运输量增加以及合成润滑油消费量增加等因素促进了欧洲可持续航空燃料市场的增长。然而,基础设施的缺乏是市场发展的制约因素。

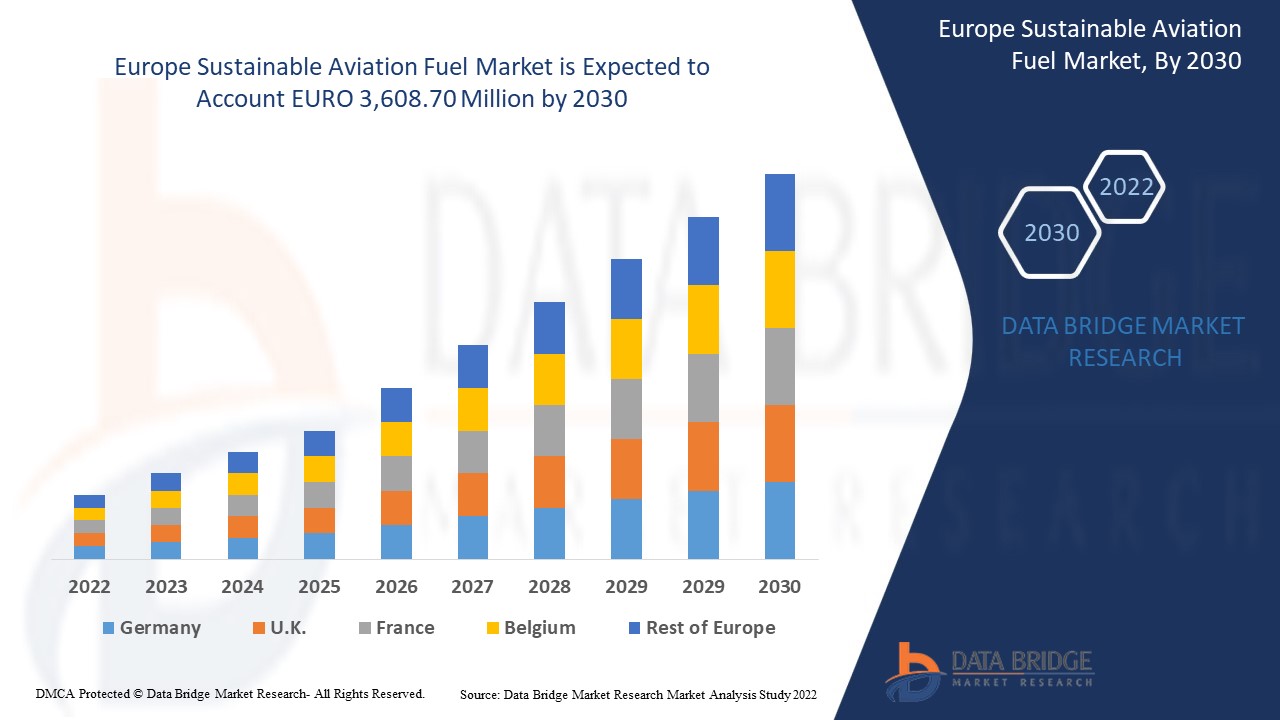

Data Bridge Market Research 分析,可持续航空燃料市场预计到 2029 年将达到 36.087 亿欧元的价值,预测期内的复合年增长率为 47.7%。由于欧洲强调推动替代燃料发展的重要性,“生物燃料”占据了可持续航空燃料市场中最大的技术领域。可持续航空燃料市场报告还深入介绍了定价分析、专利分析和技术进步。

|

报告指标 |

细节 |

|

预测期 |

2022 至 2029 年 |

|

基准年 |

2021 |

|

历史岁月 |

2020 |

|

定量单位 |

收入(百万欧元)、销量(单位)、定价(欧元) |

|

涵盖的领域 |

按燃料类型(生物燃料、氢燃料和动力至液体燃料)、按制造技术(加氢脂肪酸酯和脂肪酸 - 合成石蜡煤油 (Hefa-Spk)、费托合成石蜡煤油 (FT-SPK)、发酵加氢糖合成异构烷烃 (Hfs-Sip)、含芳烃的费托 (Ft) 合成石蜡煤油 (FT-SPK/A)、酒精至喷气燃料 Spk (ATJ-SPK) 和催化水热解喷气燃料 (CHJ))、按混合能力(30% 以下、30% 至 50% 和 50% 以上)、按混合平台(商用航空、军用航空、商务及通用航空和无人机) |

|

覆盖国家 |

欧洲的德国、英国、法国、西班牙、意大利、俄罗斯、荷兰、瑞士、土耳其、比利时及欧洲其他地区 |

|

涵盖的市场参与者 |

Neste、VELOCYS、SkyNRG、Preem AB、Eni BP plc、Cepsa、TotalEnergies、ZeroAvia, Inc. 等。 |

市场定义

可持续航空燃料是一种专为飞机使用而设计的独特燃料,同时还能提高飞机的性能。可持续航空燃料来自可持续原料,其化学性质与标准化石航空燃料非常相似。与传统航空燃料相比,可持续航空燃料的利用率提高可减少碳排放,因为它取代了燃料的生命周期。

航空业致力于减少碳足迹,以实现可持续的环境并满足严格的排放监管要求。此外,通过布局修改、混合动力和全电动飞机、可再生喷气燃料来提高航空发动机性能,这些都被航空业的众多利益相关者所采用,但与其他燃料相比,采用可持续航空燃料被认为是社会和经济效益方面最可靠和可行的机会解决方案,它有助于减轻航空业当前和预期的未来环境影响。

可持续航空燃料市场动态

本节旨在了解市场驱动因素、优势、机遇、限制和挑战。以下内容将详细讨论所有这些内容:

- 航空业减少温室气体排放的需求日益增加

人类活动产生的温室气体 (GHG) 排放加剧了温室效应,导致气候变化。二氧化碳主要通过燃烧煤炭、石油和天然气等化石燃料排放。欧洲最大的污染国包括中国和俄罗斯。这些污染主要是由石油输出国组织 (OPEC) 拥有的煤炭、石油和天然气公司造成的。由于人类活动产生的排放,大气中的二氧化碳水平比工业化前时期增长了约 50%。

飞机发动机排放的污染物与化石燃料燃烧产生的污染物相当。在高海拔地区,飞机排放的污染物浓度更高。这些排放物造成了严重的环境问题,无论是对欧洲的影响,还是对当地空气质量的影响

- 航空运输增加,合成润滑油消耗增加

航空旅行是实现经济增长和发展的关键要素。在国家、地区和全球范围内,航空旅行促进了欧洲经济的一体化并提供重要的联系。它有助于贸易、旅游业和就业机会的增长。航空系统正在不断发展,并将继续发展。然而,从长远来看,航空运输系统很难迅速适应不断变化的需求,包括容量、环境影响、消费者满意度、安全和保障,同时保持服务提供商的经济可行性。

新冠疫情、政府支持和技术进步(尤其是在燃料技术领域)加速了航空业向可持续航空燃料 (SAF) 的转型。虽然可持续航空燃料 (SAF) 的使用正在增加,但非合成润滑油的使用却在减少。合成和半合成润滑油预计将从这一转型中受益,因为大多数飞机都使用高级润滑油。预计全球可持续航空燃料 (SAF) 市场将受此因素推动。

- 航空公司对可持续航空燃料的需求增加

航空业正在采取“紧急行动”以实现世界气候目标,其中包括减少航空旅行增长和迅速扩大可持续航空燃料 (SAF) 的使用。SAF 的目的是将现有可持续生物质或气体中的碳回收成喷气燃料,以替代从石油原油中提炼的化石喷气燃料。SAF 的目的是将现有可持续生物质或气体中的碳回收成喷气燃料,以替代从石油原油中提炼的化石喷气燃料。整个航空业以及国际航空运输协会成员航空公司都致力于实现积极的减排目标。SAF(可持续航空燃料)已被强调为实现这些目标的关键组成部分。使用可持续航空燃料来实现该行业的气候目标需要政府的支持

由于主要行业参与者认识到可持续航空燃料(SAF)的必要性,因此服务提供商已开始在各家航空公司采用各种可持续航空燃料(SAF)替代品,这有望进一步推动可持续航空燃料(SAF)的增长。

- 原料和炼油厂供应不足,无法满足可持续航空燃料生产需求

可持续航空燃料 (SAF) 由生物基原料制成,是减少航空碳足迹计划的重要组成部分。从技术上讲,用 SAF 替代和混合喷气燃料是可行的;事实上,航空业已经使用 SAF 十多年了。然而,由于供需限制,消费水平仍然非常低。

油料作物、糖料作物、藻类、废油以及其他生物和非生物资源是合成燃料、电子燃料和生物喷气燃料等替代航空燃料整个生产链中必不可少的原材料。由于制造所需原材料的匮乏,对可持续航空燃料的需求可能会陷入停滞。由于制造可持续航空燃料所需的原材料稀缺,对可持续航空燃料的需求可能会停滞。此外,炼油厂的限制对这些原料的最佳利用起着关键作用,也增加了 SAF 制造的整个过程。燃料供应不足也会对燃料的混合能力造成压力,导致效率降低。

当道路汽油行业对符合可持续性标准的原料的竞争加剧时,原料供应就成为瓶颈。原料成本是 SAF 成本的重要组成部分,价格波动可能导致燃料生产商的供应问题。因此,承运商提高燃油附加费在一定程度上进一步阻碍了市场的增长。

- 原油价格波动与润滑油污染

日益激烈的欧洲竞争和成本压力迫使企业和供应链发掘未被发现的成本节约潜力。特别是,与原油市场的接口是一个有希望改进的领域。在当今的商业环境中,每个组织都面临着原油和润滑油商品价格波动的风险。在生产中,制造商可能依赖大量石油商品,因此,他们直接或间接通过零部件和子组件采购的石油产品价格波动尤其会对其产生影响。动荡不安的欧洲市场对制造组织有着广泛的影响。从能源成本上涨到原油制造成本的意外波动,不可预见的障碍正在破坏供应链的稳定性,使制造商难以保持盈利。随着许多原材料的供应越来越难以保证,商品价格波动可能不仅仅是暂时现象,制造商要么承担额外的成本,要么找到新的方法来降低费用,要么将价格上涨转嫁给那些已经不愿意消费的客户。由于定价受到供应市场紧缩的影响,这一趋势没有迹象表明会很快改变。因此,原油和其他润滑油成本的波动成为欧洲可持续航空燃料(SAF)市场的主要制约因素。

碳碎片通常不够硬或不够大,不足以导致泵故障。但它们可能大到足以堵塞微小的过滤器或喷嘴。造成操作污染的另一个原因是润滑系统中存在沙子、砂砾和金属颗粒。这对欧洲可持续航空燃料 (SAF) 市场来说是一个制约因素。

- 由于可持续航空燃料的低效性导致碳足迹减少

与其所替代的传统航空燃料相比,可持续航空燃料 (SAF) 在整个燃料使用寿命期间可减少碳排放。食用油和其他来自动物或植物的非棕榈废油是常见的原料,家庭和公司的固体废物也是如此,例如包装、纸张、纺织品和食物残渣,这些废物原本会被填埋或焚烧。森林碎屑(例如废木材)和能源作物(例如速生植物和藻类)也是可能的来源。

根据所使用的可持续原料、生产流程和机场供应链,与其取代的传统航空燃料相比,SAF 可以在燃料的使用寿命内减少高达 80% 的碳排放。

SAF 可以与标准喷气燃料混合,最高比例可达 50%,并经过与传统喷气燃料相同的质量测试。之后,该混合物将被重新认证为 Jet A 或 Jet A-1。它可以以与标准喷气燃料相同的方式处理,因此无需对加油基础设施或希望使用 SAF 的飞机进行任何更改,这为欧洲可持续航空燃料市场的增长创造了机会。

- 环保安全的航空润滑油的开发

当今世界,航空业蓬勃发展,导致各领域的航空燃料生产商之间的竞争加剧。长期航空燃料生产的替代环保来源预计将对航空燃料行业产生未来影响。由于全球范围内飞机使用先进燃料的趋势日益增长,可持续航空燃料市场多年来大幅增长。

种植用于可持续航空燃料生产的生物质作物还可以让农民在淡季通过为这一新兴行业提供原料来赚取更多收入,同时确保减少营养流失和改善土壤质量等农业优势。从而为欧洲可持续航空燃料 (SAF) 市场的增长创造了机会。

- 可持续航空燃料成本高增加航空公司运营成本

劳动力和燃料支出是航空公司面临的两项最大支出。短期内,劳动力支出通常比较稳定,但燃料价格会根据油价大幅波动。燃料是航空公司运营成本的重要组成部分,占总支出的 20-30%。油价飙升一直是航空公司最艰难的时刻之一。航空公司可以通过提高机票价格或减少航班数量来应对逐渐上涨的价格,但意外的价格上涨会导致许多航空公司亏损。

今年,可持续航空燃料 (SAF) 的使用目标将开始增加燃料成本,这让航空公司的处境更加艰难。根据国际航空运输协会 (IATA) 的数据,欧洲 SAF 产量每年仅为约 1 亿升,占所有航空燃料使用的 0.1%。另一方面,各家航空公司已承诺到 2030 年将这一比例提高到 10%,这是一个真正崇高的目标。

不幸的是,由于产量有限,SAF 的成本同样昂贵。国际航空运输协会 (IATA) 估计 SAF 的成本是化石燃料的 2 至 4 倍,而法航荷航集团 (Air France-KLM) 最近披露的一项数据表明,SAF 的成本差距可能接近煤油的 4 至 8 倍。

国际航空运输协会 (IATA) 和其他组织敦促各国政府鼓励可持续航空燃料的发展,但要以经济刺激的形式。这为可持续航空燃料 (SAF) 价格上涨铺平了道路,从而对欧洲可持续航空燃料 (市场) 构成了挑战。

新冠肺炎疫情对可持续航空燃料市场的影响

COVID-19 对可持续航空燃料市场产生了重大影响,因为几乎每个国家都选择关闭除生产必需品的工厂以外的所有生产设施。政府采取了一些严格的措施,例如停止非必需品的生产和销售、封锁国际贸易等,以防止 COVID-19 的传播。在这种大流行情况下,唯一能开展业务的是获准开放和运行流程的基本服务。

由于航空业需要减少温室气体排放,可持续航空燃料市场的增长正在增加。然而,原料和炼油厂供应不足,无法满足可持续航空燃料的生产需求等因素正在制约市场的增长。疫情期间生产设施的关闭对市场产生了重大影响。

制造商正在制定各种战略决策,以在新冠疫情后实现复苏。参与者正在进行多项研发活动,以改进可持续航空燃料所涉及的技术。借助此,这些公司将向市场推出先进而准确的控制器。此外,政府部门在航空货运中使用可持续航空燃料也推动了市场的增长。

近期发展

- 2022 年 3 月,Neste 与 DHL Express 合作宣布了有史以来最大的可持续航空燃料交易之一。该协议是 Neste 迄今为止最大的可持续航空燃料 (SAF) 协议,也是航空业最大的 SAF 协议之一。此次合作将通过在全球范围内提供无缝连接来增强 Neste 当前的网络

- 2022 年 3 月,BP 风险投资公司对 Flylogix 进行了 300 万英镑的股权投资,Flylogix 是一家开创性的无人机 (UAV) 企业,使用无人机辅助甲烷检测。这些 BP 风险投资公司专注于通过在全球范围内提供无缝连接来连接和发展新能源业务和现有网络

欧洲可持续航空燃料市场范围

可持续航空燃料市场根据燃料类型、制造技术、混合能力和混合平台进行细分。这些细分市场之间的增长将帮助您分析行业中增长微弱的细分市场,并为用户提供有价值的市场概览和市场洞察,帮助他们做出战略决策,确定核心市场应用。

燃料类型

- 生物燃料

- 氢燃料

- 电力转液体燃料

On the basis of fuel type, the Europe sustainable aviation fuel market is segmented into bio fuel, hydrogen fuel and power to liquid fuel

Manufacturing Technology

- Hydroprocessed Fatty Acid Esters and Fatty Acids - Synthetic Paraffinic Kerosene (HEFA-SPK)

- Fischer Tropsch Synthetic Paraffinic Kerosene (FT-SPK)

- Synthetic Iso-Paraffin from Fermented Hydroprocessed Sugar (HFS-SIP)

- Fischer Tropsch (FT) Synthetic Paraffinic Kerosene with Aromatics (FT-SPK/A)

- Alcohol to Jet Spk (ATJ-SPK)

- Catalytic Hydrothermolysis Jet (CHJ)

On the basis of manufacturing technology, the Europe sustainable aviation fuel market has been segmented into hydroprocessed fatty acid esters and fatty acids - synthetic paraffinic kerosene (HEFA-SPK), fischer tropsch synthetic paraffinic kerosene (FT-SPK), synthetic Iso-paraffin from fermented hydroprocessed sugar (HFS-SIP), fischer tropsch (FT) synthetic paraffinic kerosene with aromatics (FT-SPK/A), alcohol to jet SPK (ATJ-SPK) and catalytic hydrothermolysis jet (CHJ).

Blending Capacity

- Below 30 %

- 30 % To 50 %

- Above 50%

On the basis of blending capacity, the Europe sustainable aviation fuel market has been segmented into below 30 %, 30 % to 50 % and above 50%.

Blending Platform

- Commercial Aviation

- Military Aviation

- Business & General Aviation

- Unmanned Aerial Vehicle

On the basis of blending platform, the Europe sustainable aviation fuel market has been segmented into commercial aviation, military aviation, business & general aviation, and unmanned aerial vehicle

Sustainable Aviation Fuel Market Regional Analysis/Insights

The sustainable aviation fuel market is analysed and market size insights and trends are provided by country, fuel type, manufacturing technology, blending capacity, and blending platform industry as referenced above.

The countries covered in the sustainable aviation fuel market report are U.K., Germany, France, Spain, Italy, Netherlands, Switzerland, Russia, Belgium, Turkey, and the rest of Europe in Europe.

U.K. dominates the Europe sustainable aviation fuel market; this is attributable to the benefits offered by sustainable aviation fuel. In addition, increased demand for reduction in carbon footprints is propelling the European sustainable aviation fuel market ahead in Germany. The demand in this region is projected to be driven by the highlights the importance of boosting the development of alternative fuels.

报告的国家部分还提供了影响市场当前和未来趋势的各个市场影响因素和市场监管变化。下游和上游价值链分析、技术趋势和波特五力分析、案例研究等数据点是用于预测各个国家市场情景的一些指标。此外,在提供国家数据的预测分析时,还考虑了欧洲品牌的存在和可用性以及它们因来自本地和国内品牌的大量或稀缺竞争而面临的挑战、国内关税和贸易路线的影响。

竞争格局和可持续航空燃料市场份额分析

可持续航空燃料市场竞争格局提供了竞争对手的详细信息。详细信息包括公司概况、公司财务状况、收入、市场潜力、研发投资、新市场计划、欧洲业务、生产基地和设施、生产能力、公司优势和劣势、产品发布、产品宽度和广度、应用主导地位。以上提供的数据点仅与公司对可持续航空燃料市场的关注有关。

可持续航空燃料市场的一些主要参与者包括 Neste、VELOCYS、SkyNRG、Preem AB、Eni BP plc、Cepsa、TotalEnergies、ZeroAvia, Inc. 等。

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

目录

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE EUROPE SUSTAINABLE AVIATION FUEL MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELING

2.9 FUEL TYPE TIMELINE CURVE

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ANALYSIS OF FUTURE APPLICATIONS

4.2 ADVANCING SUSTAINABILITY WITHIN AVIATION

4.3 ORGANIZATIONS INVOLVED IN SUSTAINABLE AVIATION FUEL PROGRAMS

4.4 RESEARCH & INNOVATION ROADMAP FOR AVIATION HYDROGEN TECHNOLOGY

4.5 RECENT SUPPLY CONTRACTS BY SHELL

4.6 STANDARDS

4.6.1 OVERVIEW

4.6.2 INTERNATIONAL CIVIL AVIATION ORGANIZATION (ICAO)

4.6.3 INTERNATIONAL AIR TRANSPORT ASSOCIATION (IATA)

4.6.4 BUREAU OF CIVIL AVIATION SECURITY

4.6.5 FEDERAL AVIATION ADMINISTRATION

4.6.6 EUROPEAN UNION AVIATION SAFETY AGENCY (EASA)

4.6.7 CIVIL AVIATION ADMINISTRATION OF CHINA (CAAC)

4.6.8 UAE GENERAL CIVIL AVIATION AUTHORITY (GCAA)

4.7 VALUE CHAIN ANALYSIS

4.7.1 OVERVIEW OF VALUE CHAIN ANALYSIS OF SUSTAINABLE AVIATION FUEL MARKET

4.8 TECHNOLOGY TRENDS

4.8.1 OVERVIEW

4.8.2 HYDROTHERMAL LIQUEFACTION (HTL)

4.8.3 PYROLYSIS PATHWAYS OR PYROLYSIS-TO-JET (PTJ)

4.8.4 TECHNOLOGICAL MATURITY - FUEL READINESS LEVEL AND FEEDSTOCK READINESS LEVEL

4.9 IMPACT OF MEGATREND

4.1 INNOVATION AND PATENT ANALYSIS

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 INCREASING NEED FOR REDUCTION IN GHG EMISSIONS IN THE AVIATION INDUSTRY

5.1.2 INCREASE IN AIR TRANSPORTATION CONSUMPTION OF SYNTHETIC LUBRICANTS

5.1.3 INCREASE IN DEMAND FOR SUSTAINABLE AVIATION FUEL BY AIRLINES

5.1.4 INCREASE IN INVESTMENTS FOR THE GROWTH OF COMMERCIAL AIRCRAFTS

5.2 RESTRAINTS

5.2.1 INADEQUATE AVAILABILITY OF FEEDSTOCK AND REFINERIES TO MEET SUSTAINABLE AVIATION FUEL PRODUCTION DEMAND

5.2.2 FLUCTUATIONS IN CRUDE OIL PRICES AND CONTAMINATION OF LUBRICANTS

5.3 OPPORTUNITIES

5.3.1 REDUCTION IN CARBON FOOTPRINT DUE TO LOW CAPABILITY OF SUSTAINABLE AVIATION FUEL

5.3.2 DEVELOPMENT OF ECO-FRIENDLY AND SAFE AVIATION LUBRICANTS

5.3.3 RISE IN DEMAND FOR LOW-DENSITY LUBRICANTS FOR REDUCED WEIGHT

5.3.4 RISE IN SAFETY REGULATIONS FOR AIRCRAFTS

5.4 CHALLENGE

5.4.1 THE HIGH COST OF SUSTAINABLE AVIATION FUEL INCREASES THE OPERATING COST OF AIRLINES

6 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE

6.1 OVERVIEW

6.2 BIOFUEL

6.3 HYDROGEN FUEL

6.4 POWER TO LIQUID FUEL

7 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY

7.1 OVERVIEW

7.2 HYDROPROCESSED FATTY ACID EASTERS AND FATTY ACIDS - SYNTHETIC PARAFFINIC KEROSENE (HEFA-SPK)

7.3 FISCHER TROPSCH SYNTHETIC PARAFFINIC KEROSENE (FT-SPK)

7.4 SYNTHETIC ISO-PARAFFIN FROM FERMENTED HYDROPROCESSED SUGAR (HFS-SIP)

7.5 FISCHER TROPSCH (FT) SYNTHETIC PARAFFINIC KEROSENE WITH AROMATICS (FT-SPK/A)

7.6 ALCOHOL TO JET SPK (ATJ-SPK)

7.7 CATALYTIC HYDROTHERMOLYSIS JET (CHJ)

8 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY

8.1 OVERVIEW

8.2 BELOW 30%

8.3 30% TO 50%

8.4 ABOVE 50%

9 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM

9.1 OVERVIEW

9.2 COMMERCIAL AVIATION

9.2.1 BY TYPE

9.2.1.1 NARROW BODY AIRCRAFT

9.2.1.2 WIDE-BODY AIRCRAFT (WBA)

9.2.1.3 VERY LARGE AIRCRAFT (VLA)

9.2.1.4 REGIONAL TRANSPORT AIRCRAFT (RTA)

9.2.2 BY FUEL TYPE

9.2.2.1 BIOFUEL

9.2.2.2 HYDROGEN

9.2.2.3 POWER TO LIQUID FUEL

9.3 BUSINESS & GENERAL AVIATION

9.3.1 BIOFUEL

9.3.2 HYDROGEN

9.3.3 POWER TO LIQUID FUEL

9.4 MILITARY AVIATION

9.4.1 BIOFUEL

9.4.2 HYDROGEN

9.4.3 POWER TO LIQUID FUEL

9.5 UNMANNED AERIAL VEHICLE

9.5.1 BIOFUEL

9.5.2 HYDROGEN

9.5.3 POWER TO LIQUID FUEL

10 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY REGION

10.1 EUROPE

10.1.1 U.K.

10.1.2 GERMANY

10.1.3 FRANCE

10.1.4 SPAIN

10.1.5 ITALY

10.1.6 RUSSIA

10.1.7 NETHERLANDS

10.1.8 SWITZERLAND

10.1.9 TURKEY

10.1.10 BELGIUM

10.1.11 REST OF EUROPE

11 EUROPE SUSTAINABLE AVIATION FUEL MARKET: COMPANY LANDSCAPE

11.1 COMPANY SHARE ANALYSIS: EUROPE

12 SWOT ANALYSIS

13 COMPANY PROFILES

13.1 NESTE

13.1.1 COMPANY SNAPSHOT

13.1.2 REVENUE ANALYSIS

13.1.3 COMPANY SHARE ANALYSIS

13.1.4 PRODUCT PORTFOLIO

13.1.5 RECENT DEVELOPMENTS

13.2 BP P.L.C.

13.2.1 COMPANY SNAPSHOT

13.2.2 REVENUE ANALYSIS

13.2.3 COMPANY SHARE ANALYSIS

13.2.4 SERVICE PORTFOLIO

13.2.5 RECENT DEVELOPMENTS

13.3 PREEM AB.

13.3.1 COMPANY SNAPSHOT

13.3.2 COMPANY SHARE ANALYSIS

13.3.3 PRODUCT PORTFOLIO

13.3.4 RECENT DEVELOPMENT

13.4 CEPSA

13.4.1 COMPANY SNAPSHOT

13.4.2 COMPANY SHARE ANALYSIS

13.4.3 PRODUCT PORTFOLIO

13.4.4 RECENT DEVELOPMENT

13.5 CHEVRON CORPORATION

13.5.1 COMPANY SNAPSHOT

13.5.2 REVENUE ANALYSIS

13.5.3 COMPANY SHARE ANALYSIS

13.5.4 PRODUCT PORTFOLIO

13.5.5 RECENT DEVELOPMENTS

13.6 AVFUEL CORPORATION

13.6.1 COMPANY SNAPSHOT

13.6.2 PRODUCT PORTFOLIO

13.6.3 RECENT DEVELOPMENT

13.7 ENI

13.7.1 COMPANY SNAPSHOT

13.7.2 REVENUE ANALYSIS

13.7.3 PRODUCT PORTFOLIO

13.7.4 RECENT DEVELOPMENTS

13.8 EXXON MOBIL CORPORATION

13.8.1 COMPANY SNAPSHOT

13.8.2 REVENUE ANALYSIS

13.8.3 PRODUCT PORTFOLIO

13.8.4 RECENT DEVELOPMENTS

13.9 FULCRUM BIOENERGY

13.9.1 COMPANY SNAPSHOT

13.9.2 PRODUCT PORTFOLIO

13.9.3 RECENT DEVELOPMENT

13.1 GEVO

13.10.1 COMPANY SNAPSHOT

13.10.2 REVENUE ANALYSIS

13.10.3 PRODUCT PORTFOLIO

13.10.4 RECENT DEVELOPMENTS

13.11 HONEYWELL INTERNATIONAL INC.

13.11.1 COMPANY SNAPSHOT

13.11.2 REVENUE ANALYSIS

13.11.3 PRODUCT PORTFOLIO

13.11.4 RECENT DEVELOPMENTS

13.12 HYPOINT INC.

13.12.1 COMPANY SNAPSHOT

13.12.2 PRODUCT PORTFOLIO

13.12.3 RECENT DEVELOPMENT

13.13 JOHNSON MATTHEY

13.13.1 COMPANY SNAPSHOT

13.13.2 REVENUE ANALYSIS

13.13.3 PRODUCT PORTFOLIO

13.13.4 RECENT DEVELOPMENT

13.14 LANZATECH

13.14.1 COMPANY SNAPSHOT

13.14.2 PRODUCT PORTFOLIO

13.14.3 RECENT DEVELOPMENT

13.15 PROMETHEUS FUELS

13.15.1 COMPANY SNAPSHOT

13.15.2 PRODUCT PORTFOLIO

13.15.3 RECENT DEVELOPMENT

13.16 SKYNRG

13.16.1 COMPANY SNAPSHOT

13.16.2 PRODUCT PORTFOLIO

13.16.3 RECENT DEVELOPMENTS

13.17 SASOL

13.17.1 COMPANY SNAPSHOT

13.17.2 REVENUE ANALYSIS

13.17.3 PRODUCT PORTFOLIO

13.17.4 RECENT DEVELOPMENTS

13.18 TOTALENERGIES

13.18.1 COMPANY SNAPSHOT

13.18.2 REVENUE ANALYSIS

13.18.3 PRODUCT PORTFOLIO

13.18.4 RECENT DEVELOPMENT

13.19 VELOCYS

13.19.1 COMPANY SNAPSHOT

13.19.2 REVENUE ANALYSIS

13.19.3 PRODUCT PORTFOLIO

13.19.4 RECENT DEVELOPMENTS

13.2 VIRENT, INC.

13.20.1 COMPANY SNAPSHOT

13.20.2 PRODUCT PORTFOLIO

13.20.3 RECENT DEVELOPMENT

13.21 WORLD ENERGY

13.21.1 COMPANY SNAPSHOT

13.21.2 PRODUCT PORTFOLIO

13.21.3 RECENT DEVELOPMENT

13.22 ZEROAVIA, INC.

13.22.1 COMPANY SNAPSHOT

13.22.2 PRODUCT PORTFOLIO

13.22.3 RECENT DEVELOPMENT

14 QUESTIONNAIRE

15 RELATED REPORTS

表格列表

TABLE 1 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 2 EUROPE BIOFUEL IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 3 EUROPE HYDROGEN IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 4 EUROPE POWER TO LIQUID FUEL IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 5 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 6 EUROPE HYDROPROCESSED FATTY ACID EASTERS AND FATTY ACIDS - SYNTHETIC PARAFFINIC KEROSENE (HEFA-SPK) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 7 EUROPE FISCHER TROPSCH SYNTHETIC PARAFFINIC KEROSENE (FT-SPK) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 8 EUROPE SYNTHETIC ISO-PARAFFIN FROM FERMENTED HYDROPROCESSED SUGAR (HFS-SIP) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 9 EUROPE FISCHER TROPSCH (FT) SYNTHETIC PARAFFINIC KEROSENE WITH AROMATICS (FT-SPK/A) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 10 EUROPE ALCOHOL TO JET SPK (ATJ-SPK) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 11 EUROPE CATALYTIC HYDROTHERMOLYSIS JET (CHJ) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 12 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 13 EUROPE BELOW 30% IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 14 EUROPE 30% TO 50% IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 15 EUROPE ABOVE 50% IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 16 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 17 EUROPE COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 18 EUROPE COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 19 EUROPE COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 20 EUROPE BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 21 EUROPE BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 22 EUROPE MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 23 EUROPE MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 24 EUROPE UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 25 EUROPE UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 26 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY COUNTRY, 2020-2029 (EURO MILLION)

TABLE 27 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY COUNTRY, 2020-2029 (METRIC TONNES)

TABLE 28 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 29 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 30 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 31 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 32 EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 33 EUROPE COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 34 EUROPE COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 35 EUROPE BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 36 EUROPE MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 37 EUROPE UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 38 U.K. SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 39 U.K. SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 40 U.K. SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 41 U.K. SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 42 U.K. SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 43 U.K. COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 44 U.K. COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 45 U.K. BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 46 U.K. MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 47 U.K. UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 48 GERMANY SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 49 GERMANY SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 50 GERMANY SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 51 GERMANY SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 52 GERMANY SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 53 GERMANY COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 54 GERMANY COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 55 GERMANY BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 56 GERMANY MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 57 GERMANY UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 58 FRANCE SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 59 FRANCE SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 60 FRANCE SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 61 FRANCE SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 62 FRANCE SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 63 FRANCE COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 64 FRANCE COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 65 FRANCE BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 66 FRANCE MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 67 FRANCE UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 68 SPAIN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 69 SPAIN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 70 SPAIN SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 71 SPAIN SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 72 SPAIN SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 73 SPAIN COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 74 SPAIN COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 75 SPAIN BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 76 SPAIN MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 77 SPAIN UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 78 ITALY SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 79 ITALY SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 80 ITALY SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 81 ITALY SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 82 ITALY SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 83 ITALY COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 84 ITALY COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 85 ITALY BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 86 ITALY MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 87 ITALY UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 88 RUSSIA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 89 RUSSIA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 90 RUSSIA SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 91 RUSSIA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 92 RUSSIA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 93 RUSSIA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 94 RUSSIA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 95 RUSSIA BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 96 RUSSIA MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 97 RUSSIA UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 98 NETHERLANDS SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 99 NETHERLANDS SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 100 NETHERLANDS SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 101 NETHERLANDS SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 102 NETHERLANDS SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 103 NETHERLANDS COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 104 NETHERLANDS COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 105 NETHERLANDS BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 106 NETHERLANDS MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 107 NETHERLANDS UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 108 SWITZERLAND SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 109 SWITZERLAND SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 110 SWITZERLAND SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 111 SWITZERLAND SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 112 SWITZERLAND SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 113 SWITZERLAND COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 114 SWITZERLAND COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 115 SWITZERLAND BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 116 SWITZERLAND MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 117 SWITZERLAND UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 118 TURKEY SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 119 TURKEY SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 120 TURKEY SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 121 TURKEY SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 122 TURKEY SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 123 TURKEY COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 124 TURKEY COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 125 TURKEY BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 126 TURKEY MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 127 TURKEY UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 128 BELGIUM SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 129 BELGIUM SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 130 BELGIUM SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 131 BELGIUM SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 132 BELGIUM SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 133 BELGIUM COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 134 BELGIUM COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 135 BELGIUM BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 136 BELGIUM MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 137 BELGIUM UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 138 REST OF EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 139 REST OF EUROPE SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

图片列表

FIGURE 1 EUROPE SUSTAINABLE AVIATION FUEL MARKET: SEGMENTATION

FIGURE 2 EUROPE SUSTAINABLE AVIATION FUEL MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE SUSTAINABLE AVIATION FUEL MARKET: DROC ANALYSIS

FIGURE 4 EUROPE SUSTAINABLE AVIATION FUEL MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE SUSTAINABLE AVIATION FUEL MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE SUSTAINABLE AVIATION FUEL MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE SUSTAINABLE AVIATION FUEL MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE SUSTAINABLE AVIATION FUEL MARKET: VENDOR SHARE ANALYSIS

FIGURE 9 EUROPE SUSTAINABLE AVIATION FUEL MARKET: SEGMENTATION

FIGURE 10 THE INCREASING NEED FOR REDUCTION IN GHG EMISSIONS IN THE AVIATION INDUSTRY IS EXPECTED TO DRIVE THE EUROPE SUSTAINABLE AVIATION FUEL MARKET IN THE FORECAST PERIOD

FIGURE 11 BIO FUEL SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF EUROPE SUSTAINABLE AVIATION FUEL MARKET IN 2022 & 2029

FIGURE 12 NORTH AMERICA IS EXPECTED TO DOMINATE AND BE THE FASTEST-GROWING REGION IN THE EUROPE SUSTAINABLE AVIATION FUEL MARKET IN THE FORECAST PERIOD

FIGURE 13 VALUE CHAIN ANALYSIS FRAMEWORK

FIGURE 14 DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGE OF EUROPE SUSTAINABLE AVIATION FUEL MARKET

FIGURE 15 EUROPE AIR TRANSPORT PASSENGER DEMAND

FIGURE 16 EUROPE SUSTAINABLE AVIATION FUEL MARKET: BY TECHNOLOGY, 2021

FIGURE 17 EUROPE SUSTAINABLE AVIATION FUEL MARKET: BY MANUFACTURING TECHNOLOGY, 2021

FIGURE 18 EUROPE SUSTAINABLE AVIATION FUEL MARKET: BY BLENDING CAPACITY, 2021

FIGURE 19 EUROPE SUSTAINABLE AVIATION FUEL MARKET: BY BLENDING PLATFORM, 2021

FIGURE 20 EUROPE SUSTAINABLE AVIATION FUEL MARKET: SNAPSHOT (2021)

FIGURE 21 EUROPE SUSTAINABLE AVIATION FUEL MARKET: BY COUNTRY (2021)

FIGURE 22 EUROPE SUSTAINABLE AVIATION FUEL MARKET: BY COUNTRY (2022 & 2029)

FIGURE 23 EUROPE SUSTAINABLE AVIATION FUEL MARKET: BY COUNTRY (2021 & 2029)

FIGURE 24 EUROPE SUSTAINABLE AVIATION FUEL MARKET: BY FUEL TYPE (2022-2029)

FIGURE 25 EUROPE SUSTAINABLE AVIATION FUEL MARKET: COMPANY SHARE 2021 (%)

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。