North America Pv Module Encapsulant Film Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

386.62 Million

USD

1,438.59 Million

2024

2032

USD

386.62 Million

USD

1,438.59 Million

2024

2032

| 2025 –2032 | |

| USD 386.62 Million | |

| USD 1,438.59 Million | |

| % | |

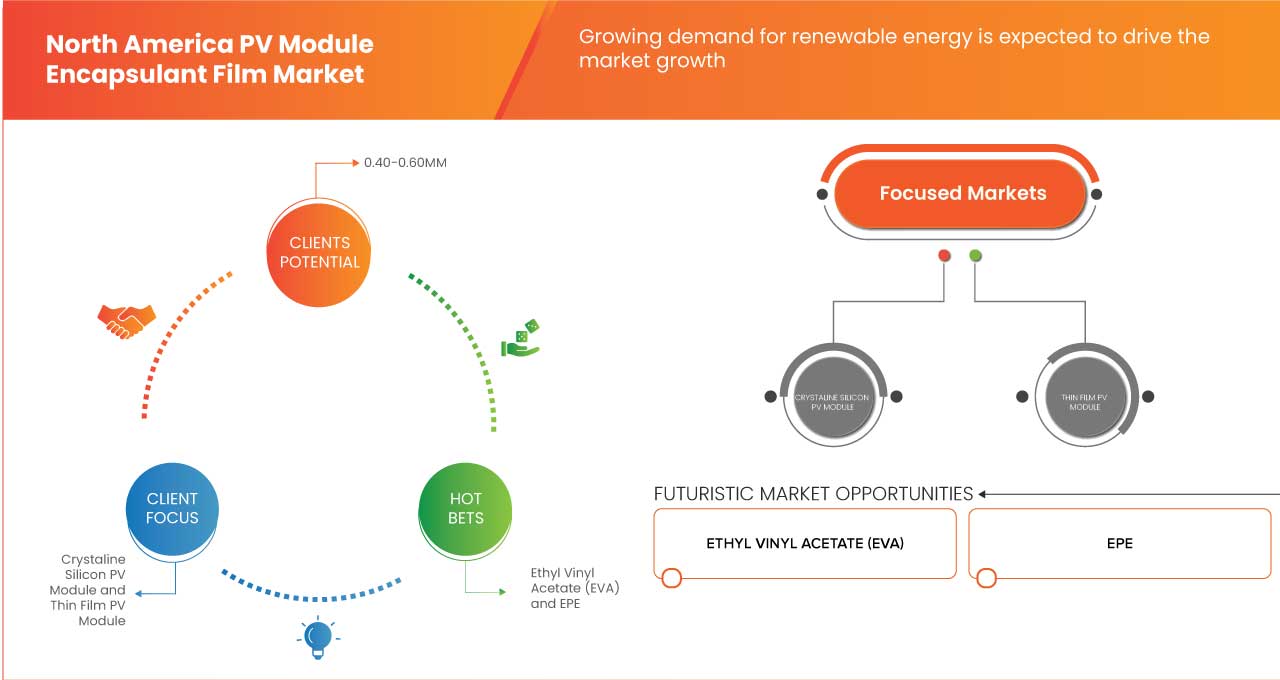

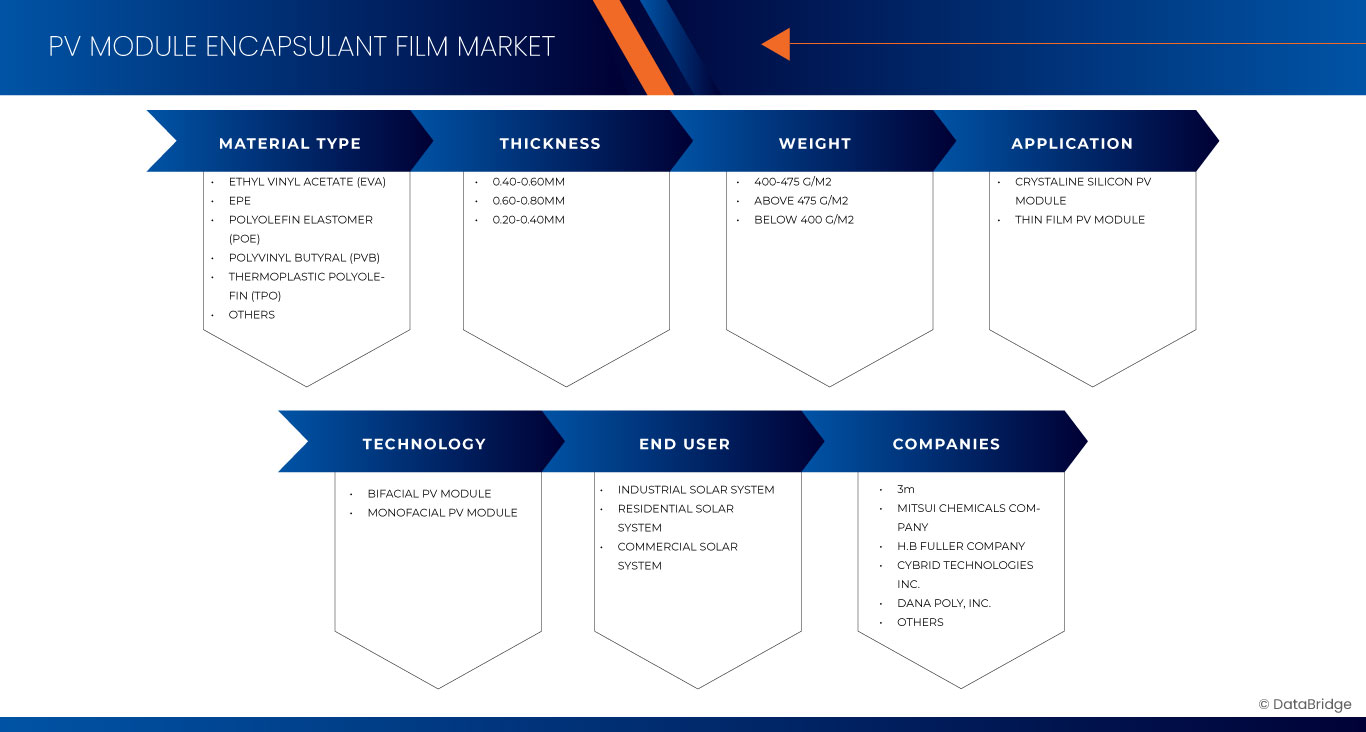

North America PV Module Encapsulant Film Market Segmentation, By Material Type (Ethyl Vinyl Acetate (EVA), EPE, Polyolefin Elastomer (POE), Polyvinyl Butyral (PVB), Thermoplastic Polyolefin (TPO), and others), Thickness (0.40-0.60MM, 0.60-0.80MM, and 0.20-0.40MM), Weight (400-475 G/M2, Above 475 G/M2, and Below 400 G/M2), Application (Crystaline Silicon PV Module, and Thin Film PV Module), Technology (Bifacial PV Module and Monofacial PV Module), End Use (Industrial Solar System, Residential Solar System, and Commercial Solar System) – Industry Trends and Forecast to 2032

North America PV Module Encapsulant Film Market Analysis

A PV module encapsulant film is a crucial component in solar panels, designed to protect and enhance the performance of photovoltaic (PV) cells. These films, typically made from materials like ethylene-vinyl acetate (EVA), act as a protective layer that insulates the solar cells from environmental factors such as moisture, dust, and UV radiation. This encapsulation ensures the durability and longevity of the solar panels, making them more reliable and efficient.

The market for PV module encapsulant films is growing in North America due to several factors. The increasing demand for renewable energy sources, driven by government initiatives and policies promoting solar energy, is a significant driver. Additionally, advancements in encapsulation materials and technologies have improved the efficiency and cost-effectiveness of solar panels, further boosting their adoption. The growing awareness of climate change and the need for sustainable energy solutions also contribute to the rising demand for PV module encapsulant films in the region.

North America PV Module Encapsulant Film Market Size

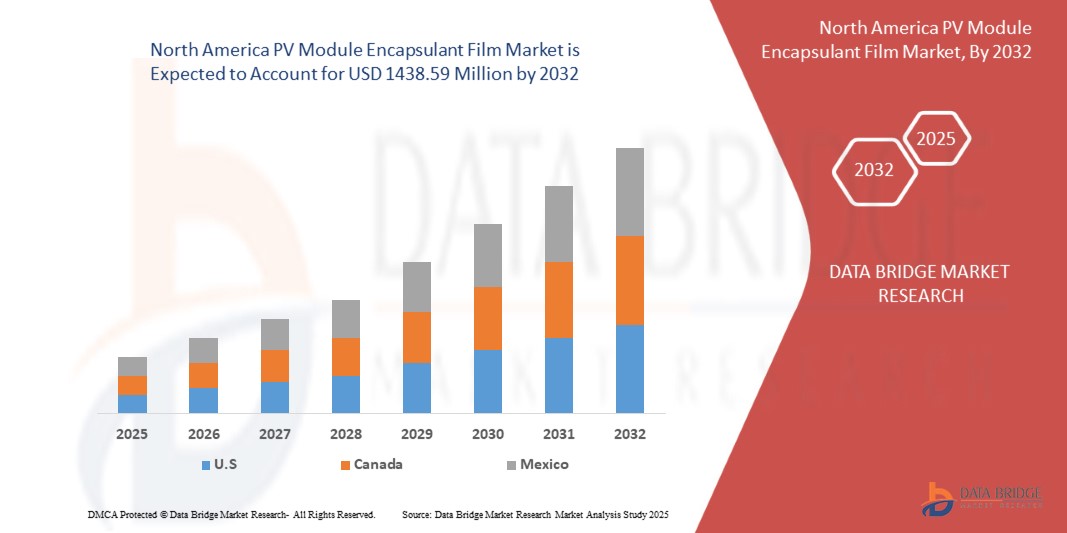

The North America PV module encapsulant film market is expected to reach USD 1438.59 million by 2032 from USD 386.62 million in 2024, growing with a substantial CAGR of 18.2% in the forecast period of 2025 to 2032.

North America PV module encapsulant film market Trends

“Increasing Installation of Rooftop Solar by Commercial and Residential Sectors”

The rising installation of rooftop solar systems in both the commercial and residential sectors is one of the most significant drivers for the growth of the North America PV Module Encapsulant Film Market. This shift toward solar energy is largely driven by the increasing demand for clean, renewable energy, government incentives, and the falling cost of solar technology. As more commercial buildings and homes adopt solar panels, the need for high-quality, durable encapsulant films has surged.

In the commercial sector, many businesses are turning to rooftop solar installations to reduce energy costs and meet sustainability targets. Companies, from large retailers to manufacturing facilities, are increasingly using solar panels to lower electricity expenses and minimize their carbon footprint. These large-scale installations require high-performance encapsulant films to ensure the solar modules' longevity and performance over time. Encapsulant films provide essential protection against environmental factors such as moisture, UV radiation, and mechanical stress, ensuring that solar panels operate at optimal efficiency.

Report Scope and Market Segmentation

|

Attributes |

North America PV module encapsulant film market Insights |

|

Segments Covered |

By Material Type: Ethyl Vinyl Acetate (EVA), EPE, Polyolefin Elastomer (POE), Polyvinyl Butyral (PVB), Thermoplastic Polyolefin (TPO), and others By Thickness: 0.40-0.60MM, 0.60-0.80MM, and 0.20-0.40MM By Weight: 400-475 G/M2, Above 475 G/M2, and Below 400 G/M2 By Application: (Crystaline Silicon PV Module, Thin Film PV Module), and Technology (Bifacial PV Module and Monofacial PV Module) By Technology: Bifacial PV Module and Monofacial PV Module By End Use: Industrial Solar System, Residential Solar System, and Commercial Solar System |

|

Countries Covered |

U.S., Canada, and Mexico |

|

Key Market Players |

3M (U.S.), Mitsui Chemicals Company (Japan), H.B Fuller Company (U.S.), Cybrid Technologies Inc. (China), Dana Poly, Inc. (U.S.), and JA Solar Technology Co.,Ltd. (China) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America PV Module Encapsulant Film Market Definition

A PV encapsulant film is a protective layer used in Photovoltaic (PV) modules to safeguard solar cells from environmental factors such as moisture, dust, and mechanical damage, ensuring their long-term performance and durability. These films are typically made from materials like ethylene vinyl acetate (EVA), polyolefins (POE), or other advanced polymers.

North America PV Module Encapsulant Film Market Dynamics

Drivers

- Growing Demand for Renewable Energy

The North America Photovoltaic (PV) module encapsulant film market is witnessing significant growth, driven largely by the increasing demand for renewable energy sources, particularly solar power. The shift towards cleaner, more sustainable energy solutions has been a dominant trend, as governments and businesses prioritize the reduction of carbon footprints and the adoption of green energy alternatives. As a result, the demand for solar photovoltaic systems has risen sharply, which in turn, drives the growth of the PV module encapsulant film market.

Encapsulant films are crucial components in solar panels, as they provide structural support, protect the cells from environmental damage, and enhance the overall performance and longevity of photovoltaic modules. These films, typically made from materials like Ethylene Vinyl Acetate (EVA), are vital for ensuring the durability of solar modules, which is essential given the long-term nature of solar investments. With the expansion of solar installations, the demand for high-quality encapsulant films is increasing to ensure the reliability and efficiency of solar panels over time.

For instance,

- In 2023, according to an article by REN21, rising renewable energy demand, with North America seeing significant solar adoption. This growth drives the PV Module Encapsulant Film Market, as encapsulant films protect solar panels, ensuring durability. Expanding solar capacity highlights the region's commitment to meeting energy needs sustainably and reducing fossil fuel reliance

- In September 2024, according to an article by IRENA, growth in renewable power, with costs for solar and wind reaching historic lows. In North America, this surge fuels the PV Module Encapsulant Film Market as solar installations expand rapidly, driven by affordability, sustainability goals, and policies supporting renewable energy adoption across residential and commercial sectors

Technological Advancements and Innovations in Encapsulant Films

The North America Photovoltaic (PV) module encapsulant film Market is experiencing robust growth, driven significantly by technological advancements and innovations in encapsulant film materials and manufacturing processes. Encapsulant films are critical components of photovoltaic (PV) modules, as they protect solar cells from moisture, UV radiation, and mechanical stresses, while ensuring efficient light transmission and electrical insulation.

Innovations in encapsulant film technology focus on enhancing performance, durability, and environmental sustainability. the development of advanced materials such as ethylene-vinyl acetate (EVA) with improved crosslinking properties, thermoplastic polyolefins (TPO), and polyvinyl butyral (PVB) has led to encapsulants with superior thermal stability and resistance to delamination. These innovations are critical as solar panels are exposed to harsh environmental conditions for 20 to 30 years.

For instance,

- In February 2024, according to an article by Royal Society of Chemistry, innovations in encapsulant materials like thermoplastic polyolefins (TPO) and advanced transparent conductive films. These materials enhance solar panel durability, efficiency, and adaptability to bifacial technologies. Such advancements drive North America's PV Module Encapsulant Film Market, aligning with the growing adoption of high-performance solar energy systems

- In January 2023, according to an article by John Wiley & Sons, Inc, innovations in encapsulant films, including thermoplastic materials and UV-stabilized polymers, that improve solar panel efficiency and lifespan. These advancements cater to the increasing adoption of bifacial and tandem PV technologies, driving North America's PV Module Encapsulant Film Market in response to the region's accelerating renewable energy expansion

Opportunities

- Advancement in Bifacial Solar Modules

The North American Photovoltaic (PV) module encapsulant film market is witnessing significant opportunities, primarily driven by advancements in bifacial solar modules. Bifacial solar modules, which capture sunlight from both the front and rear sides of the panel, offer higher energy efficiency and performance compared to traditional monofacial solar panels. As the adoption of bifacial modules grows, the demand for advanced encapsulant films, a key component of these modules, is expected to rise.

Encapsulant films play a critical role in PV modules, providing structural integrity, durability, and protection against environmental factors such as moisture, temperature fluctuations, and UV radiation. The evolution of bifacial solar technology has brought forward the need for encapsulant films that can support the unique design and performance characteristics of these modules. Unlike traditional monofacial panels, bifacial modules are often installed in environments where they can harness reflected light, and as such, encapsulant films must be optimized for this double-sided energy collection.

One of the primary advancements in encapsulant technology for bifacial modules is the development of transparent, highly durable, and efficient materials that allow more light to pass through to the rear side of the solar cells. This transparency, combined with improved moisture resistance and UV stability, enhances the overall energy yield and longevity of the panels.

For instance,

- In October 2023, according to an article by Mibet Energy, Advancements in bifacial solar modules have significantly enhanced their efficiency by capturing sunlight from both the front and rear sides of the panel. These innovations include improved durability, with tempered glass that resists UV damage and extreme weather conditions. Bifacial panels also offer better performance in diffused light, reduced degradation over time, and longer warranties compared to monofacial panels, making them ideal for commercial and utility-scale applications

The rise of bifacial solar modules presents significant opportunities for the North American PV module encapsulant film market. Advancements in encapsulant technology, offering improved transparency, durability, and performance, align with growing demand for higher efficiency in solar energy. This trend will drive innovation and position North America as a key player in the renewable energy transition.

Restraint/Challenge

- High Initial Capital Costs

The high initial capital costs associated with solar Photovoltaic (PV) systems remain a major restraint. Solar energy adoption requires substantial upfront investment, including the cost of solar panels, inverters, installation, and encapsulant films, which impacts the decision-making process for both commercial and residential sectors.

For commercial and residential customers, the initial capital outlay for a solar PV system can be daunting. While solar energy promises long-term savings, the upfront cost of purchasing and installing the system remains high. Encapsulant films, which protect solar cells and enhance the longevity of PV modules, are a critical component of the overall solar system cost. While these films are essential for ensuring high performance, their cost contributes to the overall financial burden. For residential customers, even with incentives like tax credits and rebates, the total upfront expenditure is often seen as prohibitive, especially for those with limited access to financing or capital.

North America PV Module Encapsulant Film Market Scope

The market is segmented on the basis of by material type, thickness, weight, application, technology, and end use. The growth amongst these segments will help you analyze meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

By Material Type

- Ethyl Vinyl Acetate (EVA)

- Ethyl Vinyl Acetate (EVA), BY MATERIAL TYPE

- Transparent EVA

- White EVA

- Anti-PID EVA

- Ethyl Vinyl Acetate (EVA), BY MATERIAL TYPE

- EPE

- Polyolefin Elastomer (POE)

- Polyvinyl Butyral (PVB)

- Thermoplastic Polyolefin (TPO)

- Others

By Thickness

- 0.40-0.60MM

- 0.60-0.80MM

- 0.20-0.40MM

By Weight

- 400-475 G/M2

- ABOVE 475 G/M2

- BELOW 400 G/M2

By Application

- Crystaline Silicon PV Module

- Crystaline Silicon PV Module, BY TYPE

- Polycrystaline Modlue

- Monocrystaline Modlue

- Crystaline Silicon PV Module, BY TYPE

- Thin Film PV Module

By Technology

- Bifacial PV Module

- Monofacial PV Module

By End Use

- Industrial Solar System

- Residential Solar System

- Commercial Solar System

North America PV Module Encapsulant Film Market Regional Analysis

The market is analyzed and market size insights and trends are provided by The market is segmented on the basis of by material type, thickness, weight, application, technology, and end use.

The countries covered in the market are U.S., Canada, Mexico.

U.S. is expected to dominate and fastest growing country in the market due to technological advancements and innovations in encapsulant films.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries.

Also, the presence and availability of North America brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

North America PV Module Encapsulant Film Market Share

The market competitive landscape provides details by competitors. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, North America presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

North America PV Module Encapsulant Film Market Leaders Operating in the Market Are:

- 3M (U.S.)

- Mitsui Chemicals Company (Japan)

- H.B Fuller Company (U.S.)

- Cybrid Technologies Inc. (China)

- Dana Poly, Inc. (U.S.)

- JA Solar Technology Co.,Ltd. (China)

Latest Developments in North America PV Module Encapsulant Film Market

- In September 2024, H.B. Fuller has acquired HS Butyl Limited, the UK’s leading manufacturer of high-quality butyl tapes. This acquisition strengthens H.B. Fuller's position in the global waterproofing tape market and expands its reach in Europe, where the market is significantly larger than North America. It also offers growth opportunities in engineering adhesives

- In May 2024, H.B. Fuller has acquired ND Industries, a leader in fastener locking and sealing solutions. This acquisition expands H.B. Fuller's offerings in high-growth sectors such as automotive, electronics, and aerospace. ND Industries' Vibra-Tite brand and expertise in pre-applied coatings enhance H.B. Fuller's engineering adhesives capabilities, creating new opportunities for innovation and customer solutions

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 DBMR VENDOR SHARE ANALYSIS

2.1 MARKET APPLICATION COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.1.1 POLITICAL FACTORS

4.1.2 ECONOMIC FACTORS

4.1.3 SOCIAL FACTORS

4.1.4 TECHNOLOGICAL FACTORS

4.1.5 ENVIRONMENTAL FACTORS

4.1.6 LEGAL FACTORS

4.1.7 CONCLUSION

4.2 PORTER’S FIVE FORCES

4.2.1 THREAT OF NEW ENTRANTS

4.2.2 THREAT OF SUBSTITUTES

4.2.3 BARGAINING POWER OF SUPPLIERS

4.2.4 BARGAINING POWER OF BUYERS

4.2.5 COMPETITIVE RIVALRY

4.3 IMPORT EXPORT SCENARIO

4.4 PRICING ANALYSIS

4.5 PRODUCTION CONSUMPTION ANALYSIS

4.6 VENDOR SELECTION CRITERIA

4.6.1 QUALITY AND CONSISTENCY

4.6.2 PRICE AND COST COMPETITIVENESS

4.6.3 SUPPLY CHAIN RELIABILITY AND LEAD TIMES

4.6.4 TECHNICAL CAPABILITIES AND EXPERTISE

4.6.5 SUSTAINABILITY AND COMPLIANCE

4.6.6 REPUTATION AND TRACK RECORD

4.6.7 INNOVATION AND LONG-TERM PARTNERSHIP

4.6.8 RISK MITIGATION AND FINANCIAL STABILITY

4.7 CLIMATE CHANGE SCENARIO

4.7.1 ENVIRONMENTAL CONCERNS

4.7.2 INDUSTRY RESPONSE

4.7.3 GOVERNMENT'S ROLE

4.7.4 ANALYST RECOMMENDATIONS

4.8 PRODUCTION CAPACITY OVERVIEW

4.8.1 MARKET DEMAND FOR SOLAR ENERGY

4.8.2 TECHNOLOGICAL ADVANCEMENTS IN ENCAPSULANT FILM MATERIALS

4.8.3 RAW MATERIAL AVAILABILITY AND SUPPLY CHAIN DYNAMICS

4.8.4 REGULATORY AND POLICY INFLUENCES

4.8.5 COMPETITIVE LANDSCAPE AND KEY PLAYERS

4.9 RAW MATERIAL COVERAGE

4.9.1 ETHYLENE VINYL ACETATE (EVA)

4.9.1.1 TRANSPARENT EVA

4.9.1.2 WHITE EVA

4.9.1.3 ANTI-PID EVA

4.9.2 POLYVINYL BUTYRAL (PVB)

4.9.3 POLYOLEFIN ELASTOMER (POE)

4.9.4 THERMOPLASTIC POLYOLEFIN (TPO)

4.9.5 EPE

4.9.6 OTHERS (IONOMERS AND SILICONES)

4.9.7 CONCLUSION

4.1 SUPPLY CHAIN ANALYSIS

4.10.1 OVERVIEW

4.10.2 LOGISTIC COST SCENARIO

4.10.3 IMPORTANCE OF LOGISTICS SERVICE PROVIDERS

4.11 TECHNOLOGY ADVANCEMENTS BY MANUFACTURERS

4.11.1 ADVANCED MATERIAL CHEMISTRY AND FORMULATION

4.11.2 IMPROVED OPTICAL PROPERTIES AND EFFICIENCY

4.11.3 DEVELOPMENT OF NEW MATERIALS FOR ENCAPSULANT FILMS

4.11.4 ADVANCED MANUFACTURING MACHINES FOR SHRINKAGE-RESISTANT FILMS

4.11.5 CONCLUSION

5 REGULATION COVERAGE

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 GROWING DEMAND FOR RENEWABLE ENERGY

6.1.2 TECHNOLOGICAL ADVANCEMENTS AND INNOVATIONS IN ENCAPSULANT FILMS

6.1.3 INCREASING INSTALLATION OF ROOFTOP SOLAR BY COMMERCIAL AND RESIDENTIAL SECTORS

6.1.4 DECLINING COSTS OF SOLAR PV COMPONENTS

6.2 RESTRAINTS

6.2.1 HIGH INITIAL CAPITAL COSTS

6.2.2 COMPETITION FROM ALTERNATIVE ENERGY SOURCES

6.3 OPPORTUNITIES

6.3.1 ADVANCEMENT IN BIFACIAL SOLAR MODULES

6.3.2 LARGE-SCALE SOLAR PROJECTS, SUPPORTED BY FEDERAL AND STATE-LEVEL INCENTIVES

6.3.3 CIRCULAR ECONOMY AND SUSTAINABILITY INITIATIVES

6.4 CHALLENGES

6.4.1 PERFORMANCE DEGRADATION ISSUES

6.4.2 STRINGENT REGULATIONS AND EVOLVING SAFETY STANDARDS

7 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE

7.1 OVERVIEW

7.2 ETHYL VINYL ACETATE (EVA)

7.2.1 ETHYL VINYL ACETATE (EVA), BY MATERIAL TYPE

7.3 EPE

7.4 POLYOLEFIN ELASTOMER (POE)

7.5 POLYVINYL BUTYRAL (PVB)

7.6 THERMOPLASTIC POLYOLEFIN (TPO)

7.7 OTHERS

8 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY THICKNESS

8.1 2.1 OVERVIEW

8.2 0.40-0.60MM

8.3 0.60-0.80MM

8.4 0.20-0.40MM

9 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY WEIGHT

9.1 OVERVIEW

9.2 400-475 G/M2

9.3 ABOVE 475 G/M2

9.4 BELOW 400 G/M2

10 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY APPLICATION

10.1 OVERVIEW

10.2 CRYSTALINE SILICON PV MODULE

10.2.1 CRYSTALINE SILICON PV MODULE, BY TYPE

10.3 THIN FILM PV MODULE

11 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY TECHNOLOGY

11.1 OVERVIEW

11.2 BIFACIAL PV MODULE

11.3 MONOFACIAL PV MODULE

12 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY END USE

12.1 OVERVIEW

12.2 INDUSTRIAL SOLAR SYSTEM

12.3 RESIDENTIAL SOLAR SYSTEM

12.4 COMMERCIAL SOLAR SYSTEM

13 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY COUNTRY

13.1 NORTH AMERICA

13.1.1 U.S.

13.1.2 CANADA

13.1.3 MEXICO

14 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: COMPANY LANDSCAPE

14.1 COMPANY SHARE ANALYSIS

15 SWOT ANALYSIS

16 COMPANY PROFILES

16.1 3M

16.1.1 COMPANY SNAPSHOT

16.1.2 REVENUE ANALYSIS

16.1.3 PRODUCT PORTFOLIO

16.1.4 RECENT DEVELOPMENT

16.2 MITSUI CHEMICALS ICT MATERIA, INC

16.2.1 COMPANY SNAPSHOT

16.2.2 PRODUCT PORTFOLIO

16.2.3 RECENT DEVELOPMENT

16.3 H.B. FULLER COMPANY

16.3.1 COMPANY SNAPSHOT

16.3.2 REVENUE ANALYSIS

16.3.3 PRODUCT PORTFOLIO

16.3.4 RECENT DEVELOPMENT

16.4 CYBRID TECHNOLOGIES INC.

16.4.1 COMPANY SNAPSHOT

16.4.2 REVENUE ANALYSIS

16.4.3 PRODUCT PORTFOLIO

16.4.4 RECENT DEVELOPMENT

16.5 DANA POLY, INC

16.5.1 COMPANY SNAPSHOT

16.5.2 PRODUCT PORTFOLIO

16.5.3 RECENT DEVELOPMENT

16.6 JA SOLAR TECHNOLOGY CO.,LTD.

16.6.1 COMPANY SNAPSHOT

16.6.2 PRODUCT PORTFOLIO

16.6.3 RECENT DEVELOPMENT

17 QUESTIONNAIRE

18 RELATED REPORTS

표 목록

TABLE 1 REGULATION COVERAGE

TABLE 2 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (USD THOUSAND)

TABLE 3 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (TONS)

TABLE 4 NORTH AMERICA ETHYL VINYL ACETATE (EVA) IN PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (USD THOUSAND)

TABLE 5 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY THICKNESS, 2018-2032 (USD THOUSAND)

TABLE 6 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY WEIGHT, 2018-2032 (USD THOUSAND)

TABLE 7 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 8 NORTH AMERICA CRYSTALINE SILICON PV MODULE IN PV MODULE ENCAPSULANT FILM MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 9 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY TECHNOLOGY, 2018-2032 (USD THOUSAND)

TABLE 10 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY END USE, 2018-2032 (USD THOUSAND)

TABLE 11 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY COUNTRY, 2018-2032 (USD THOUSAND)

TABLE 12 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY COUNTRY, 2018-2032 (TONS)

TABLE 13 U.S. PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (USD THOUSAND)

TABLE 14 U.S. PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (TONS)

TABLE 15 U.S. ETHYL VINYL ACETATE (EVA) IN PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (USD THOUSAND)

TABLE 16 U.S. PV MODULE ENCAPSULANT FILM MARKET, BY THICKNESS, 2018-2032 (USD THOUSAND)

TABLE 17 U.S. PV MODULE ENCAPSULANT FILM MARKET, BY WEIGHT, 2018-2032 (USD THOUSAND)

TABLE 18 U.S. PV MODULE ENCAPSULANT FILM MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 19 U.S. CRYSTALINE SILICON PV MODULE IN PV MODULE ENCAPSULANT FILM MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 20 U.S. PV MODULE ENCAPSULANT FILM MARKET, BY TECHNOLOGY, 2018-2032 (USD THOUSAND)

TABLE 21 U.S. PV MODULE ENCAPSULANT FILM MARKET, BY END USE, 2018-2032 (USD THOUSAND)

TABLE 22 CANADA PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (USD THOUSAND)

TABLE 23 CANADA PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (TONS)

TABLE 24 CANADA ETHYL VINYL ACETATE (EVA) IN PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (USD THOUSAND)

TABLE 25 CANADA PV MODULE ENCAPSULANT FILM MARKET, BY THICKNESS, 2018-2032 (USD THOUSAND)

TABLE 26 CANADA PV MODULE ENCAPSULANT FILM MARKET, BY WEIGHT, 2018-2032 (USD THOUSAND)

TABLE 27 CANADA PV MODULE ENCAPSULANT FILM MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 28 CANADA CRYSTALINE SILICON PV MODULE IN PV MODULE ENCAPSULANT FILM MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 29 CANADA PV MODULE ENCAPSULANT FILM MARKET, BY TECHNOLOGY, 2018-2032 (USD THOUSAND)

TABLE 30 CANADA PV MODULE ENCAPSULANT FILM MARKET, BY END USE, 2018-2032 (USD THOUSAND)

TABLE 31 MEXICO PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (USD THOUSAND)

TABLE 32 MEXICO PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (TONS)

TABLE 33 MEXICO ETHYL VINYL ACETATE (EVA) IN PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL TYPE, 2018-2032 (USD THOUSAND)

TABLE 34 MEXICO PV MODULE ENCAPSULANT FILM MARKET, BY THICKNESS, 2018-2032 (USD THOUSAND)

TABLE 35 MEXICO PV MODULE ENCAPSULANT FILM MARKET, BY WEIGHT, 2018-2032 (USD THOUSAND)

TABLE 36 MEXICO PV MODULE ENCAPSULANT FILM MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 37 MEXICO CRYSTALINE SILICON PV MODULE IN PV MODULE ENCAPSULANT FILM MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 38 MEXICO PV MODULE ENCAPSULANT FILM MARKET, BY TECHNOLOGY, 2018-2032 (USD THOUSAND)

TABLE 39 MEXICO PV MODULE ENCAPSULANT FILM MARKET, BY END USE, 2018-2032 (USD THOUSAND)

그림 목록

FIGURE 1 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET

FIGURE 2 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: REGIONAL VS COUNTRIES MARKET ANALYSIS

FIGURE 5 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: MULTIVARIATE MODELLING

FIGURE 7 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 8 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: DBMR MARKET POSITION GRID

FIGURE 9 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: APPLICATION COVERAGE GRID

FIGURE 11 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: SEGMENTATION

FIGURE 12 SIX SEGMENTS COMPRISE NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, BY MATERIAL (2024)

FIGURE 13 EXECUTIVE SUMMARY

FIGURE 14 STRATEGIC DECISIONS

FIGURE 15 GROWING DEMAND FOR RENEWABLE ENERGY IS EXPECTED TO DRIVE THE NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET IN THE FORECAST PERIOD

FIGURE 16 THE ETHYL VINYL ACETATE (EVA) SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET IN 2025 AND 2032

FIGURE 17 PESTEL ANALYSIS

FIGURE 18 PORTER’S FIVE FORCES

FIGURE 19 IMPORT EXPORT SCENARIO (USD THOUSAND)

FIGURE 20 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET, 2023-2032, AVERAGE SELLING PRICE (USD/KG)

FIGURE 21 PRODUCTION CONSUMPTION ANALYSIS

FIGURE 22 VENDOR SELECTION CRITERIA

FIGURE 23 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES FOR GLOBAL LIDAR MARKET

FIGURE 24 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: BY MATERIAL TYPE, 2024

FIGURE 25 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: BY THICKNESS, 2024

FIGURE 26 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: BY WEIGHT, 2024

FIGURE 27 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: BY APPLICATION, 2024

FIGURE 28 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: BY TECHNOLOGY, 2024

FIGURE 29 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: BY END USE, 2024

FIGURE 30 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: SNAPSHOT (2024)

FIGURE 31 NORTH AMERICA PV MODULE ENCAPSULANT FILM MARKET: COMPANY SHARE 2024 (%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.