北米の半導体製造装置市場

Market Size in USD Billion

CAGR :

%

| 2024 –2030 | |

| % | |

>北米の半導体製造装置市場、装置タイプ別(フロントエンド装置およびバックエンド装置)、寸法別(3D、2.5D、2D)、製品タイプ別(メモリ、MEMS、ファウンドリ、アナログ、MPU、ロジック、ディスクリート、その他)、サプライチェーン参加者別(ファウンドリ、アウトソーシングされた半導体組立およびテスト(OSAT)企業、統合デバイス製造(IDM)企業)、ファブ施設装置別(工場自動化、ガス制御装置、化学制御装置) - 2030年までの業界動向と予測。

北米の半導体製造装置市場の分析と洞察

半導体製造装置市場は、コネクテッドデバイスや自動車産業における半導体装置の採用増加により、大幅に成長しています。ICの設計が複雑になるにつれて、より多くの半導体製品がICの作成に組み込まれています。半導体は、IC開発コストの削減、最終製品の価値の向上、市場投入までの時間の短縮、量産までの時間の短縮に役立つため、電子設計プロセスに不可欠なものになっています。企業がICの設計ギャップを埋めるのに役立ちます。

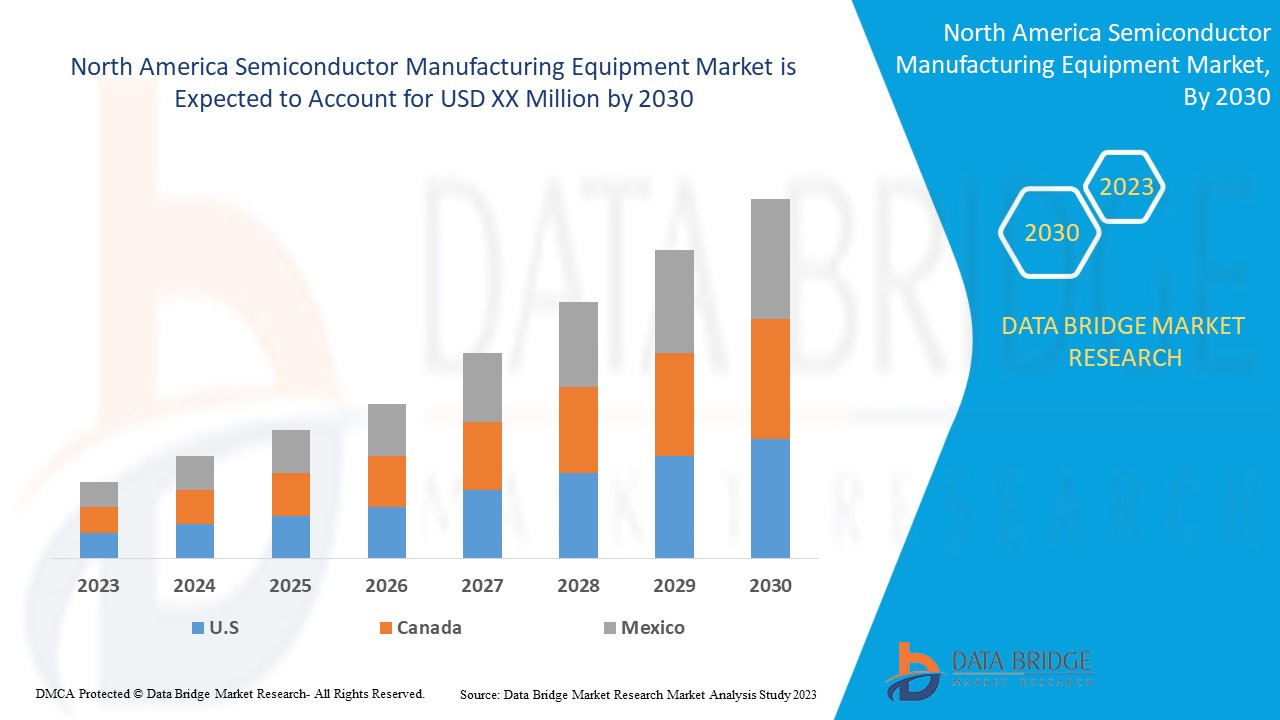

Data Bridge Market Researchは、北米の半導体製造装置市場は2023年から2030年の予測期間中に9.1%のCAGRで成長すると分析しています。

|

レポートメトリック |

詳細 |

|

予測期間 |

2023年から2030年 |

|

基準年 |

2022 |

|

歴史的な年 |

2021 (2020 - 2015 にカスタマイズ可能) |

|

定量単位 |

売上高(百万米ドル)、販売数量(個数)、価格(米ドル) |

|

対象セグメント |

装置タイプ(フロントエンド装置およびバックエンド装置)、寸法(3D、2.5D、2D)、製品タイプ(メモリ、MEMS、ファウンドリ、アナログ、MPU、ロジック、ディスクリート、その他)、サプライチェーン参加者(ファウンドリ、アウトソーシングされた半導体組立およびテスト(OSAT)企業、統合デバイス製造(IDM)企業)、およびファブ施設装置(ファクトリーオートメーション、ガス制御機器、化学制御機器)別。 |

|

対象国 |

北米では米国、カナダ、メキシコ。 |

|

対象となる市場プレーヤー |

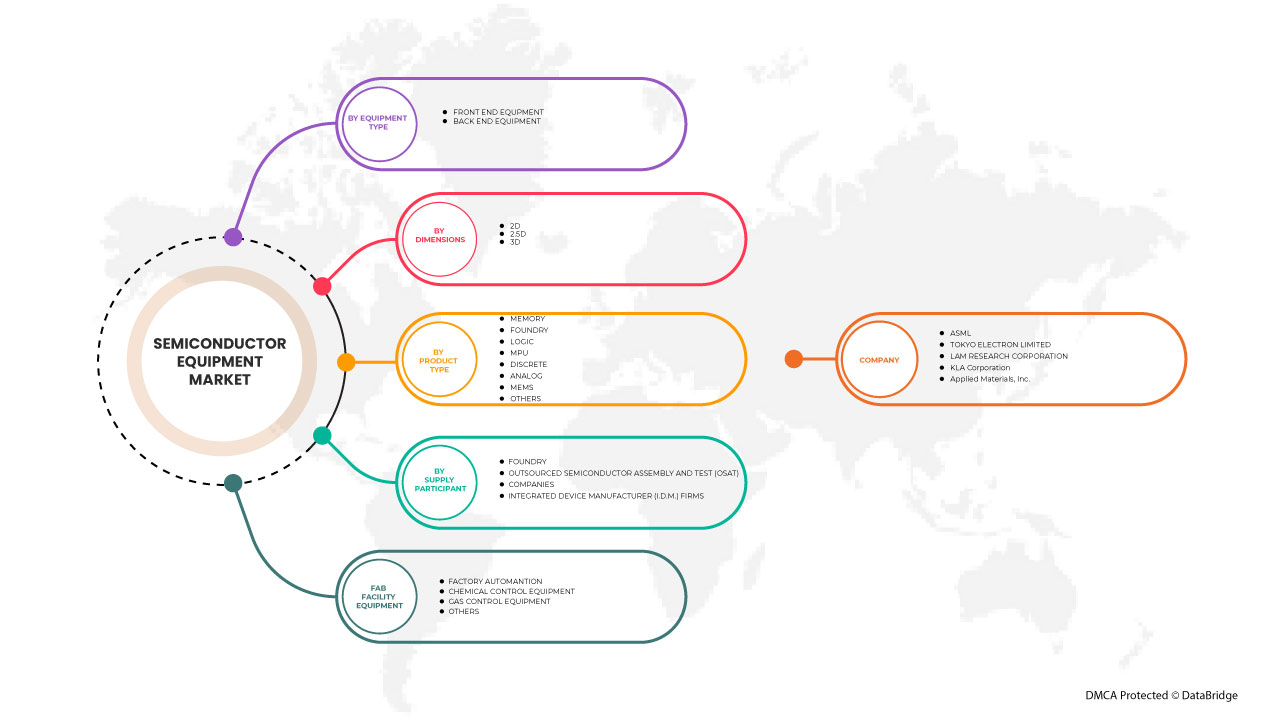

ASML、KLA Corporation、Plasma-Therm、LAM RESEARCH CORPORATION、Veeco Instruments Inc.、EV Group、東京エレクトロン株式会社、キヤノンマシナリー株式会社、ノードソン株式会社、日立ハイテク株式会社、Advanced Dicing Technologies、Evatec AG、NOIVION、Modutek.com、QP Technologies、Applied Materials, Inc.、株式会社SCREENホールディングス、テラダイン株式会社、Onto Innovation、株式会社アドバンテスト、東京精密株式会社、SÜSS MicroTec SE、ASMPT、FormFactor、UNITES Systems as、Gigaphoton Inc.、Palomar Technologies など。 |

半導体製造装置の定義

Semiconductor equipment generally refers to the production equipment required to produce various semiconductor products and belongs to the key supporting link of the semiconductor industry chain. Semiconductor equipment is the technological leader in the semiconductor industry. Chip design, wafer manufacturing, and packaging and testing must be designed and manufactured within the scope of equipment technology. The advancement of equipment technology also promotes the development of the semiconductor industry.

Semiconductor Manufacturing Equipment Market Dynamics

This section deals with understanding the market drivers, advantages, opportunities, restraints and challenges. All of this is discussed in detail as below:

Drivers

-

INCREASING CONSUMPTION OF CONSUMER ELECTRONICS

Increasing consumers' disposable income and need for advanced electronic products drive the consumer electronics market. Consumers are becoming techno-savvy and adopting new technologies at work, in daily routines, in personal entertainment, and others. Smart devices are adopting the major market share owing to improved control, features, and other functions. Consumers are ready to spend extra money on advanced gadgets to enhance their experiences and living standards. The flexible electronics equipped with flexible sensors are available in the market under premium category products; hence acceptance for premium products is driving the market growth.

-

GROWING DEMAND FOR SEMICONDUCTORS ACROSS THE GLOBE

A substance with specialised electrical properties called a semiconductor can be used as the basis for computers and other electronic devices. Typically, it is a solid chemical element or compound that, in some circumstances, transmits electricity but not in others. Because of this, it is the perfect medium for controlling electrical current and common electrical appliances.

Semiconductors are microscopic electrical devices comprised of silicon, germanium, or gallium arsenide compounds. The semiconductor industry develops and produces semiconductors. Almost every electronic device includes semiconductors, including televisions, computers, medical diagnostic tools, cell phones, and video games. The big, cumbersome vacuum tube technology of the past has been replaced by the modern, ever-shrinking semiconductor thanks to advancements made in the semiconductor industry since 1960, allowing for the creation of smaller, faster, and even more dependable electronic devices. Electronics firms and manufacturers in the United States, Japan, China, South Korea, France, and Italy currently make up the USD 300 billion semiconductor sector.

Opportunity

-

RISE IN DIGITAL SUPPLY CHAIN ACROSS THE GLOBE

A supply chain that uses data analytics and digital technologies to make decisions, improve performance, and react swiftly to changing circumstances is known as a "digital supply chain." Digital supply networks are fundamentally driven by data generated by current supply chains, which is stored in data warehouses and evaluated for useful insights.

As a necessary initial step, historical supply chain management technologies such as demand planning, asset management, warehouse management system, transportation and logistics management, procurement, and order fulfillment must be fully integrated. However, to digitise a supply chain, data from those operations must also be mined, and the equipment that enables them to provide the required data must be instrumented.

The emergence of the Cloud, the rollout of 5G, connected vehicles, and digitalization have all contributed to a never-before-seen demand for high-performance computing. The most coveted semiconductor market is also racing to board the digitalization train. A key element of improved supply chain resilience is data insights. Semiconductor firms may make quicker, data-driven choices by utilizing technology and applications to capture precise data and analytics at all supply chain points.

Restraints/Challenges

- DISRUPTION IN THE SUPPLY CHAIN INDUSTRY

The war for semiconductors, specifically contested by the automotive and high-tech consumer industries, is one of the biggest North America issues affecting supply chains in specialized industries.

The Covid-19 pandemic, which shut down auto manufacturing while skyrocketing North America consumption of domestic electronics, was the conflict's major cause. However, the source of the problem predates the North America lockdown.

Manufacturing suddenly decreased in 2020 due to hastily cancelled orders and just-in-time procedures when the pandemic lockdown began. However, as customers used more laptop computers, 5G phones, gaming consoles, and other .T.I.T. devices, demand for silicon chips soared due to the epidemic working circumstances. A V-shaped recovery for personal computers, mobile devices, cars, and wireless communications resulted from a fall in semiconductor demand by the end of 2020.

Recent Development

- In September 2022, Onto Innovation announced its first lot to deliver the Company’s Dragonfly G3 system with the new EB40 module to a top three semiconductor manufacturer. This helps the company expand its product portfolio and the offering to the market.

Semiconductor Manufacturing Equipment Market Scope

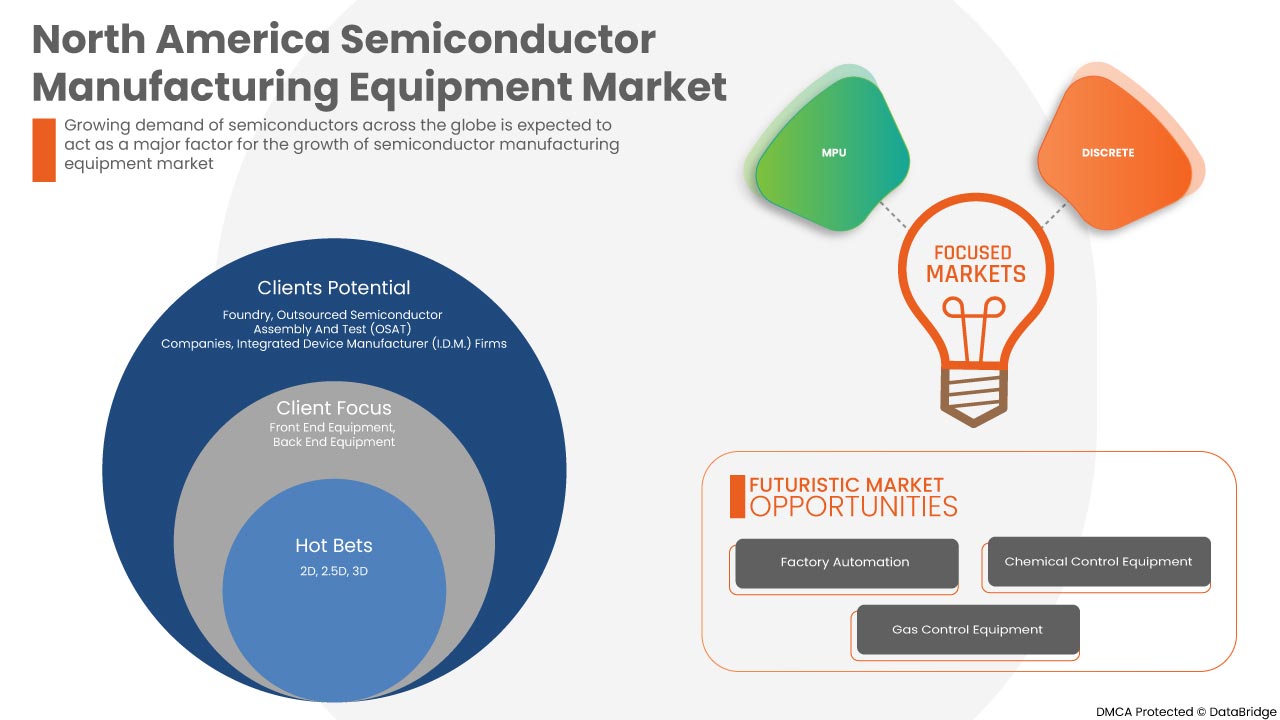

The semiconductor manufacturing equipment market is segmented on the basis of by equipment type, dimensions, product type, supply chain participant and fab facility equipment. The growth amongst these segments will help you analyze meager growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Equipment Type

- Front End Equipment

- Back End Equipment

On the basis of equipment type, the market is segmented into front end equipment and back end equipment.

Dimensions

- 2D

- 2.5D

- 3D

On the basis of dimensions, the market is segmented into 2D, 2.5D, and 3D.

Product Type

- Memory

- Foundry

- Logic

- MPU

- Discrete

- Analog

- MEMS

- Other

On the basis of product type, the market is segmented into memory, foundry, logic, M.P.U., discrete, analog, MEMS, and others.

Supply Chain Participant

- Foundry

- Outsourced Semiconductor Assembly And Test (OSAT) Companies

- Integrated Device Manufacturer (I.D.M.) Firms

On the basis of supply chain participant, the market is segmented into foundry, outsourced semiconductor assembly and test (OSAT) companies, and integrated device manufacturer (I.D.M.) firms.

Fab Facility Equipment

- Factory Automation

- Chemical Control Equipment

- Gas Control Equipment

- Other

On the basis of fab facility equipment, the market is segmented into factory automation, chemical control equipment, gas control equipment, and others.

Semiconductor Manufacturing Equipment Market Regional Analysis/Insights

The semiconductor manufacturing equipment market is analysed and market size insights and trends are provided by equipment type, dimensions, product type, supply chain participant and fab facility equipment.

The countries covered in the semiconductor manufacturing equipment market report are U.S., Canada and Mexico in North America.

In North America, the U.S. is expected to dominate the market due to the rise in digital supply chain across the globe.

The country section of the report also provides individual market impacting factors and changes in regulations in the market domestically that impacts the current and future trends of the market. Data points such as new sales, replacement sales, country demographics, disease epidemiology and import-export tariffs are some of the major pointers used to forecast the market scenario for individual countries. Also, presence and availability of North America brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of sales channels are considered while providing forecast analysis of the country data.

Competitive Landscape and Semiconductor Manufacturing Equipment Market Share Analysis

半導体製造装置市場の競争状況は、競合他社ごとに詳細を提供します。含まれる詳細には、会社概要、会社の財務状況、収益、市場の可能性、研究開発への投資、新しい市場への取り組み、北米でのプレゼンス、生産拠点と施設、生産能力、会社の強みと弱み、ソリューションの導入、製品の幅広さと幅広さ、アプリケーションの優位性などがあります。提供されている上記のデータ ポイントは、半導体製造装置市場に関連する会社の焦点にのみ関連しています。

北米の半導体製造装置市場で活動している主要企業には、ASML、KLA Corporation、Plasma-Therm、LAM RESEARCH CORPORATION、Veeco Instruments Inc.、EV Group、東京エレクトロン株式会社、キヤノンマシナリー株式会社、ノードソン株式会社、日立ハイテク株式会社、Advanced Dicing Technologies、Evatec AG、NOIVION、Modutek.com、QP Technologies、Applied Materials, Inc.、株式会社SCREEN Holdings、Teradyne Inc.、Onto Innovation、株式会社アドバンテスト、東京精密株式会社、SÜSS MicroTec SE、ASMPT、FormFactor、UNITES Systems as、Gigaphoton Inc.、Palomar Technologiesなどがあります。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

目次

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELING

2.9 COMPONENT TYPE TIMELINE CURVE

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 INCREASING CONSUMPTION OF CONSUMER ELECTRONICS

5.1.2 GROWING DEMAND FOR SEMICONDUCTORS ACROSS THE GLOBE

5.1.3 EMERGENCE OF A LARGE NUMBER OF SEMICONDUCTOR MANUFACTURING FACILITIES

5.1.4 TECHNOLOGICAL ADVANCEMENTS AND THE ADOPTION OF INNOVATIVE TECHNOLOGIES SUCH AS ARTIFICIAL INTELLIGENCE AND BLOCKCHAIN

5.1.5 GROWING ADOPTION OF IOT ACROSS THE SEMICONDUCTOR INDUSTRY

5.2 RESTRAINTS

5.2.1 HIGH COMPETITION IN THE SEMICONDUCTOR MANUFACTURING MARKET

5.2.2 HIGH R&D COST IN THE SEMICONDUCTOR EQUIPMENT MARKET

5.3 OPPORTUNITIES

5.3.1 RISE IN DIGITAL SUPPLY CHAIN ACROSS THE GLOBE

5.3.2 INTRODUCTION OF KERFLESS WAFER OVER TRADITIONAL WAFER

5.3.3 VERY HIGH GROWTH OF THE AUTOMOBILE INDUSTRY

5.4 CHALLENGES

5.4.1 DISRUPTION IN THE SUPPLY CHAIN INDUSTRY

5.4.2 ENVIRONMENTAL CONCERNS RAISED DUE TO SEMICONDUCTOR PRODUCTION

6 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE

6.1 OVERVIEW

6.2 FRONT END EQUIPMENT

6.2.1 LITHOGRAPHY

6.2.1.1 DUV

6.2.1.2 EUV

6.2.2 DEPOSITION

6.2.2.1 PVD

6.2.2.2 CVD

6.2.3 WAFER SURFACE CONDITIONING

6.2.3.1 ETCHING

6.2.3.2 CHEMICAL

6.2.4 CLEANING

6.2.4.1 BATCH SPRAY CLEANING SYSTEM

6.2.4.2 SINGLE-WAFER SPRAY SYSTEM

6.2.4.3 SINGLE-WAFER CRYOGENIC SYSTEM

6.2.4.4 BATCH IMMERSION CLEANING SYSTEM

6.2.4.5 SCRUBBER

6.2.5 OTHER EQUIPMENT

6.3 BACK END EQUIPMENT

6.3.1 TESTING

6.3.2 ASSEMBLY AND PACKING

6.3.3 DICING EQUIPMENT

6.3.4 BONDING EQUIPMENT

6.3.5 METROLOGY

7 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS

7.1 OVERVIEW

7.2 3D

7.3 2.5D

7.4 2D

8 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE

8.1 OVERVIEW

8.2 MEMORY

8.3 MEMS

8.4 FOUNDRY

8.5 ANALOG

8.6 MPU

8.7 LOGIC

8.8 DISCRETE

8.9 OTHERS

9 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT

9.1 OVERVIEW

9.2 INTEGRATED DEVICE MANUFACTURER (IDM) FIRMS

9.3 FOUNDRY

9.4 OUTSOURCED SEMICONDUCTOR ASSEMBLY AND TEST (OSAT) COMPANIES

10 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT

10.1 OVERVIEW

10.2 FACTORY AUTOMATION

10.2.1 FRONT END EQUIPMENT

10.2.2 BACK END EQUIPMENT

10.3 GAS CONTROL EQUIPMENT

10.3.1 FRONT END EQUIPMENT

10.3.2 BACK END EQUIPMENT

10.4 CHEMICAL CONTROL EQUIPMENT

10.4.1 FRONT END EQUIPMENT

10.4.2 BACK END EQUIPMENT

10.5 OTHERS

11 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION

11.1 NORTH AMERICA

11.1.1 U.S.

11.1.2 CANADA

11.1.3 MEXICO

12 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 ASML

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENT

14.2 TOKYO ELECTRON LIMITED

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENTS

14.3 LAM RESEARCH CORPORATION

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENT

14.4 KLA CORPORATION

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENT

14.5 APPLIED MATERIALS, I.N.C.

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT AND TECHNOLOGIES PORTFOLIO

14.5.5 RECENT DEVELOPMENTS

14.6 ADVANCED DICING TECHNOLOGIES

14.6.1 COMPANY SNAPSHOT

14.6.2 PRODUCT PORTFOLIO

14.6.3 RECENT DEVELOPMENTS

14.7 ADVANTEST CORPORATION

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCTS PORTFOLIO

14.7.4 RECENT DEVELOPMENTS

14.8 ASMPT

14.8.1 COMPANY SNAPSHOT

14.8.2 REVENUE ANALYSIS

14.8.3 PRODUCTS PORTFOLIO

14.8.4 RECENT DEVELOPMENTS

14.9 CANON MACHINERY INC.

14.9.1 COMPANY SNAPSHOT

14.9.2 PRODUCT PORTFOLIO

14.9.3 RECENT DEVELOPMENT

14.1 EV GROUP

14.10.1 COMPANY SNAPSHOT

14.10.2 PRODUCT PORTFOLIO

14.10.3 RECENT DEVELOPMENTS

14.11 EVATEC AG

14.11.1 COMPANY SNAPSHOT

14.11.2 PRODUCT PORTFOLIO

14.11.3 RECENT DEVELOPMENT

14.12 FORMFACTOR.

14.12.1 COMPANY SNAPSHOT

14.12.2 REVENUE ANALYSIS

14.12.3 PRODUCTS PORTFOLIO

14.12.4 RECENT DEVELOPMENTS

14.13 GIGAPHOTON INC.

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCTS PORTFOLIO

14.13.3 RECENT DEVELOPMENTS

14.14 HITACHI HIGH-TECH CORPORATION

14.14.1 COMPANY SNAPSHOT

14.14.2 PRODUCT PORTFOLIO

14.14.3 RECENT DEVELOPMENTS

14.15 MODUTEK CORPORATION

14.15.1 COMPANY SNAPSHOT

14.15.2 PRODUCT PORTFOLIO

14.15.3 RECENT DEVELOPMENTS

14.16 NOIVION S.R.L.

14.16.1 COMPANY SNAPSHOT

14.16.2 PRODUCT PORTFOLIO

14.16.3 RECENT DEVELOPMENTS

14.17 NORDSON CORPORATION

14.17.1 COMPANY SNAPSHOT

14.17.2 REVENUE ANALYSIS

14.17.3 PRODUCT PORTFOLIO

14.17.4 RECENT DEVELOPMENTS

14.18 ONTO INNOVATION.

14.18.1 COMPANY SNAPSHOT

14.18.2 REVENUE ANALYSIS

14.18.3 PRODUCTS PORTFOLIO

14.18.4 RECENT DEVELOPMENTS

14.19 PALOMAR TECHNOLOGIES

14.19.1 COMPANY SNAPSHOT

14.19.2 PRODUCTS PORTFOLIO

14.19.3 RECENT DEVELOPMENTS

14.2 PLASMA-THERM

14.20.1 COMPANY SNAPSHOT

14.20.2 PRODUCT PORTFOLIO

14.20.3 RECENT DEVELOPMENTS

14.21 QP TECHNOLOGIES

14.21.1 COMPANY SNAPSHOT

14.21.2 SERVICE PORTFOLIO

14.21.3 RECENT DEVELOPMENT

14.22 SCREEN HOLDINGS CO., LTD.

14.22.1 COMPANY SNAPSHOT

14.22.2 REVENUE ANALYSIS

14.22.3 PRODUCTS PORTFOLIO

14.22.4 RECENT DEVELOPMENTS

14.23 SÜSS MICROTEC SE

14.23.1 COMPANY SNAPSHOT

14.23.2 REVENUE ANALYSIS

14.23.3 PRODUCT PORTFOLIO

14.23.4 RECENT DEVELOPMENTS

14.24 TERADYNE INC.

14.24.1 COMPANY SNAPSHOT

14.24.2 REVENUE ANALYSIS

14.24.3 PRODUCTS PORTFOLIO

14.24.4 RECENT DEVELOPMENTS

14.25 TOKYO SEIMITSU CO., LTD

14.25.1 COMPANY SNAPSHOT

14.25.2 REVENUE ANALYSIS

14.25.3 PRODUCTS PORTFOLIO

14.25.4 RECENT DEVELOPMENTS

14.26 UNITES SYSTEMS A.S.

14.26.1 COMPANY SNAPSHOT

14.26.2 PRODUCT PORTFOLIO

14.26.3 RECENT DEVELOPMENTS

14.27 VEECO INSTRUMENTS INC.

14.27.1 COMPANY SNAPSHOT

14.27.2 REVENUE ANALYSIS

14.27.3 PRODUCT PORTFOLIO

14.27.4 RECENT DEVELOPMENT

15 QUESTIONNAIRE

16 RELATED REPORTS

表のリスト

TABLE 1 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 2 NORTH AMERICA FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 3 NORTH AMERICA FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 4 NORTH AMERICA LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 5 NORTH AMERICA DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 6 NORTH AMERICA WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 7 NORTH AMERICA CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 8 NORTH AMERICA BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 9 NORTH AMERICA BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 10 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 11 NORTH AMERICA 3D IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 12 NORTH AMERICA 2.5D IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 13 NORTH AMERICA 2D IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 14 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 15 NORTH AMERICA MEMORY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 16 NORTH AMERICA MEMS IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 17 NORTH AMERICA FOUNDRY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 18 NORTH AMERICA ANALOG IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 19 NORTH AMERICA MPU IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 20 NORTH AMERICA LOGIC IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 21 NORTH AMERICA DISCRETE IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 22 NORTH AMERICA OTHERS IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 23 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 24 NORTH AMERICA INTEGRATED DEVICE MANUFACTURER (IDM) FIRMS IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 25 NORTH AMERICA FOUNDRY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 26 NORTH AMERICA OUTSOURCED SEMICONDUCTOR ASSEMBLY AND TEST (OSAT) COMPANIES IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 27 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 28 NORTH AMERICA FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 29 NORTH AMERICA FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 30 NORTH AMERICA GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 31 NORTH AMERICA GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 32 NORTH AMERICA CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 33 NORTH AMERICA CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 34 NORTH AMERICA OTHERS IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 35 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY COUNTRY, 2021-2030 (USD MILLION)

TABLE 36 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 37 NORTH AMERICA FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 38 NORTH AMERICA LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 39 NORTH AMERICA DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 40 NORTH AMERICA WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 41 NORTH AMERICA CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 42 NORTH AMERICA BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 43 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 44 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 45 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 46 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 47 NORTH AMERICA FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 48 NORTH AMERICA GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 49 NORTH AMERICA CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 50 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 51 U.S. FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 52 U.S. LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 53 U.S. DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 54 U.S. WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 55 U.S. CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 56 U.S. BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 57 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 58 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 59 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 60 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 61 U.S. FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 62 U.S. GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 63 U.S. CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 64 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 65 CANADA FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 66 CANADA LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 67 CANADA DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 68 CANADA WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 69 CANADA CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 70 CANADA BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 71 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 72 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 73 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 74 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 75 CANADA FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 76 CANADA GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 77 CANADA CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 78 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 79 MEXICO FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 80 MEXICO LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 81 MEXICO DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 82 MEXICO WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 83 MEXICO CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 84 MEXICO BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 85 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 86 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 87 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 88 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 89 MEXICO FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 90 MEXICO GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 91 MEXICO CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

図表一覧

FIGURE 1 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET :DBMR MARKET POSITION GRID

FIGURE 8 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: VENDOR SHARE ANALYSIS

FIGURE 9 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: SEGMENTATION

FIGURE 10 GROWING DEMAND FOR SEMICONDUCTOR ACROSS THE GLOBE IS BOOSTING THE GROWTH OF THE SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET IN THE FORECAST PERIOD OF 2023 -2030

FIGURE 11 EQUIPMENT TYPE SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET IN 2023 - 2030

FIGURE 12 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET

FIGURE 13 DESKTOP VS MOBILE VS TABLET MARKET SHARE WORLDWIDE, APRIL 2020

FIGURE 14 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY EQUIPMENT TYPE, 2022

FIGURE 15 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY DIMENSIONS, 2022

FIGURE 16 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY PRODUCT TYPE, 2022

FIGURE 17 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY SUPPLY CHAIN PARTICIPANT, 2022

FIGURE 18 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY FAB FACILITY EQUIPMENT, 2022

FIGURE 19 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: SNAPSHOT (2022)

FIGURE 20 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY COUNTRY (2022)

FIGURE 21 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY COUNTRY (2023 & 2030)

FIGURE 22 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY COUNTRY (2022 & 2030)

FIGURE 23 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY EQUIPMENT TYPE (2023-2030)

FIGURE 24 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: COMPANY SHARE 2022 (%)

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。