世界の医療費償還市場の規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

23.10 Billion

USD

78.65 Billion

2024

2032

USD

23.10 Billion

USD

78.65 Billion

2024

2032

| 2025 –2032 | |

| USD 23.10 Billion | |

| USD 78.65 Billion | |

| % | |

|

世界の医療費償還市場のセグメンテーション、請求(全額支払および不足支払)、支払者(民間支払者および公的支払者)、サービスプロバイダー(医師の診療所、病院、診断研究所、その他)別 - 業界動向と2032年までの予測

医療費償還市場規模

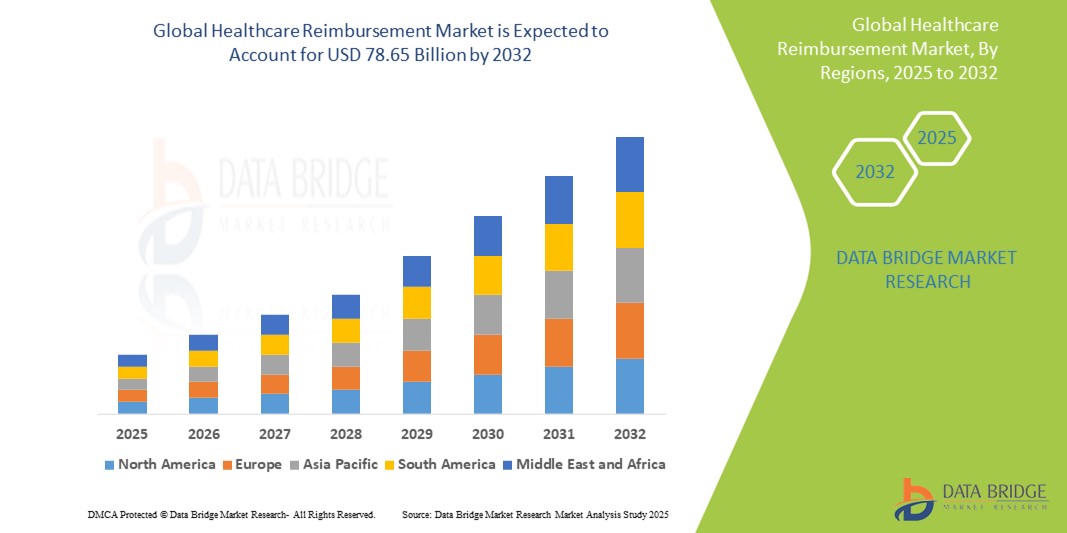

- 世界の医療費償還市場規模は2024年に231億米ドルと評価され、予測期間中に16.55%のCAGRで成長し、2032年までに786億5000万米ドル に達すると予想されています。

- 市場の成長は、効率的な医療資金調達メカニズムの需要の高まり、医療費の上昇、そして慢性疾患の負担の増大によって主に推進されており、世界的に構造化された拡張可能な償還システムを必要としています。

- さらに、政府支援の医療プログラムの拡大、価値に基づく償還モデル、そして請求処理における技術の進歩が、医療償還システムの導入を促進しています。これらの要因が重なり合い、透明性、迅速性、そして説明責任のある医療資金提供への移行が加速し、医療業界の成長を大きく後押ししています。

医療費償還市場分析

- 医療費償還システムは、医療提供者、支払者、患者間の支払い処理を容易にし、請求の合理化、エラーの削減、規制要件の遵守をサポートする役割を担っているため、公的および私的医療環境の両方で医療費を管理し、タイムリーな補償を確保する上でますます重要になっています。

- 高度な医療費償還ソリューションに対する需要の高まりは、主に医療費請求の複雑さの増大、医療サービスの拡大に伴う請求件数の増加、そして正確な償還追跡と報告を必要とする価値ベースのケアモデルへの重点の高まりによって促進されています。

- 北米は、成熟した医療インフラ、電子医療記録(EHR)の広範な導入、厳格な規制枠組み、統合された償還プラットフォームを提供する大手テクノロジーベンダーの存在を特徴とし、2024年には46.2%という最大の収益シェアで医療償還市場を支配します。

- アジア太平洋地域は、医療費の増加、保険適用範囲の拡大に向けた政府改革、デジタルヘルス技術の導入増加、医療アクセスの拡大を支援するための償還プロセスの合理化への重点化により、予測期間中に医療償還市場で最も急速に成長する地域になると予想されています。

- 低賃金セグメントは、医療費償還市場において2024年に81.7%の市場シェアを占め、医療提供者が直面する償還ギャップと資金不足に対処し、提供されたサービスに対するタイムリーな調整と正確な報酬を確保するという重要な役割を担っている。

レポートの範囲と医療費償還市場のセグメンテーション

|

属性 |

医療費償還の主要市場インサイト |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

医療費償還市場の動向

「自動化とAIを活用した請求処理の進歩」

- 世界の医療保険償還市場において、請求処理の効率化、手作業によるミスの削減、償還精度の向上を目的とした自動化および人工知能(AI)技術の導入が、重要かつ加速的に進んでいます。この変化により、従来の償還ワークフローは、より効率的でデータ主導のプロセスへと変革しています。

- 例えば、Change HealthcareやOptumなどのAI搭載プラットフォームは、機械学習アルゴリズムを活用して膨大なデータセットを分析し、不正請求を検出し、償還決定を最適化しています。同様に、IBM Watson Healthなどのクラウドベースのソリューションは、予測分析を統合することで、請求審査のスピードと精度を向上させています。

- 医療費償還におけるAIの統合により、請求の自動スクラビング、リアルタイムの適格性確認、インテリジェントな却下管理といった機能が可能になり、遅延の削減と医療提供者のキャッシュフローの改善につながります。例えば、一部のプラットフォームでは、自然言語処理(NLP)を用いて複雑な医療コードや書類を解釈し、請求却下を最小限に抑えています。さらに、ロボティック・プロセス・オートメーション(RPA)は、定型的な請求業務の迅速化に役立ち、スタッフがより価値の高い業務に集中できるようにします。

- 償還システムと電子医療記録(EHR)および医療提供者ポータルのシームレスな統合により、請求、請求、支払いの一元管理が容易になります。統合プラットフォームを通じて、関係者は償還状況を監視し、問題を迅速に解決し、規制遵守を確保できます。

- 関係者が複雑な医療請求プロセスの管理において効率性、正確性、コンプライアンスを重視する傾向が強まるにつれ、高度なAIと自動化機能を備えた医療費償還プラットフォームの需要は、病院、保険会社、政府機関全体で急速に高まっています。

医療費償還市場の動向

ドライバ

「医療費の高騰と効率的な償還システムへの需要の高まり」

- 世界中で高騰する医療費と、医療費請求および保険請求の複雑さが増していることが、高度な医療費償還ソリューションの需要を刺激する大きな要因となっています。

- 例えば、2024年には、Change Healthcareなどの大手企業が、請求処理の自動化と支払い遅延の削減を目的とした、AIを活用した強化された償還プラットフォームを導入し、コスト効率の高い医療財務管理の切迫したニーズに対応しました。こうした大手企業によるイノベーションは、予測期間中の市場成長を加速させると予想されます。

- 医療提供者と支払者は、タイムリーな支払いを確保しながら経費を管理するというプレッシャーが高まる中、自動化、リアルタイムの請求追跡、エラー検出を提供する償還システムは、従来の手動プロセスに比べて重要な改善をもたらします。

- さらに、価値に基づくケアモデルの採用の増加と医療の透明性を目的とした政府の取り組みにより、関係者はコンプライアンスをサポートし、収益サイクルを最適化する、より堅牢な償還フレームワークを導入するよう求められています。

- 電子医療記録(EHR)や医療情報交換(HIE)と保険償還ソリューションの統合が進むにつれ、シームレスなデータ共有が可能になり、業務効率が向上しています。また、請求管理を簡素化し、支払者と医療提供者間の多様なやり取りをサポートする、拡張性と使いやすさを兼ね備えたプラットフォームへの需要も高まっており、世界中の病院、診療所、保険会社における導入が進んでいます。

抑制/挑戦

「データセキュリティと高額な導入コストに関する懸念」

- 医療費償還システムにおけるデータセキュリティとプライバシーの脆弱性に関する懸念は、市場への導入拡大にとって大きな課題となっています。これらのプラットフォームは患者や財務に関する機密情報を扱うため、サイバー攻撃の格好の標的となり、医療提供者や保険支払者の間で、潜在的なデータ漏洩やコンプライアンスリスクへの懸念が高まっています。

- 例えば、医療データ漏洩やランサムウェア攻撃の注目を集めた事件により、一部の組織は、強力なセキュリティ対策を講じずに償還ワークフローを完全にデジタル化することに慎重になっています。

- こうした懸念に対処するには、高度な暗号化、多要素認証、そして厳格な規制遵守(米国のHIPAAや欧州のGDPRなど)が不可欠です。OptumやCernerといった企業は、強固なセキュリティフレームワークと定期的なシステム監査を重視し、顧客のデータ安全性を確保しています。さらに、高度な償還プラットフォームの導入には、ソフトウェアライセンスの取得、既存の医療ITシステムとの統合、スタッフのトレーニングなど、比較的高額な初期コストがかかるため、特に小規模な医療機関や発展途上地域の組織にとって導入の障壁となる可能性があります。

- クラウドベースおよびモジュール型の償還ソリューションは初期費用の削減に役立っていますが、導入に伴う財務上の負担と複雑さが、広範な市場浸透の課題となっています。

- 強化されたサイバーセキュリティプロトコル、ベストプラクティスの教育、拡張可能で費用対効果の高い償還プラットフォームの開発を通じてこれらの障害を克服することは、医療償還市場の持続的な成長に不可欠です。

医療費償還市場の展望

市場は、請求、支払者、およびサービスプロバイダーに基づいてセグメント化されています。

- 請求により

請求額に基づき、医療費償還市場は、全額支払済みと未払いの2つに分類されます。未払いセグメントは、請求システムの複雑化、コードエラー、そして保険金請求の再提出や不服申し立てが必要となる保険金却下の増大により、2024年には81.7%という最大の収益シェアを占め、市場を席巻しました。これらの課題により、未払い請求は、失われた収益の回復と請求精度の向上を目指す医療提供者にとって重要な焦点となっています。

全額支払セグメントは、請求処理テクノロジーの強化、AI 対応の請求システム、および支払者とプロバイダーの連携の改善によるエラーの削減と初回提出時の請求承認率の向上により、予測期間中に最も急速に成長すると予想されています。

- 支払者別

支払者に基づいて、市場は民間支払者と公的支払者に区分されます。民間支払者セグメントは、特に雇用主と民間保険会社が医療費の資金調達において中心的な役割を果たしている先進地域において、商業保険プランの広範な普及により、2024年には市場を牽引するでしょう。これらの支払者は、デジタル償還システムを早期に導入しており、自動化とデータ分析による運用コストの削減に注力しています。

公的保険支払者セグメントは、政府の医療プログラムの拡大、人口の高齢化、発展途上国および新興経済国全体での公的保険の払い戻しプロセスの合理化への取り組みにより、予測期間中に最も急速に成長すると予想されています。

- サービスプロバイダー別

サービスプロバイダーに基づいて、市場は診療所、病院、診断検査室、その他に分類されます。2024年には、病院セグメントが収益面で市場を牽引しました。これは、入院・外来サービス、手術、長期ケアの膨大な量によって、堅牢な償還管理を必要とする複雑で高額な請求が発生するためです。

診断ラボ部門は、予防的健康診断や慢性疾患診断の増加、そして利益率の低い大量の検査に対する効率的かつ正確な請求処理へのニーズの高まりを背景に、予測期間中に最も急速な成長が見込まれています。COVID-19パンデミック中およびパンデミック後のラボサービスへの依存度の高まりも、このセグメントの成長加速に貢献しています。

医療費償還市場の地域分析

- 成熟した医療インフラ、電子医療記録(EHR)の普及、厳格な規制枠組み、統合型償還プラットフォームを提供する大手テクノロジーベンダーの存在により、北米は2024年に46.2%という最大の収益シェアで医療償還市場を支配します。

- この地域は、請求の透明性と標準化をサポートする強力な規制枠組みに加えて、高度なデジタル請求および償還システムの早期導入からも恩恵を受けています。

- さらに、米国とカナダでは慢性疾患の蔓延と人口の高齢化が進み、医療サービスの量が大幅に増加し、効率的かつ正確な償還プロセスへの需要が高まっています。大手医療提供者、保険支払者、そしてヘルステック企業の存在は、北米の市場におけるリーダーシップをさらに強化しています。

米国医療保険償還市場の洞察

米国の医療費償還市場は、メディケア、メディケイド、そして広範な雇用主主導の医療保険制度といった、米国の強固な公的・民間保険制度に牽引され、2024年には北米最大の収益シェア89%を占めると予測されています。市場は、包括的な医療保険制度、高い医療処置利用率、そして高度なデジタル請求処理システムの恩恵を受けています。さらに、価値に基づく償還モデルや一括支払いといった改革により、医療費償還の効率性と透明性が強化され、市場の成長がさらに加速しています。

欧州医療保険償還市場の洞察

欧州の医療費償還市場は、ドイツ、英国、フランスなどの国々における国民皆保険制度の普及に支えられ、予測期間中、着実な拡大が見込まれます。英国のNHS(国民保健サービス)やドイツの法定健康保険といった強力な公的保険機関の存在は、償還可能な医療サービスへの幅広いアクセスを確保しています。電子請求管理システムの導入拡大と、EU諸国における償還枠組みの標準化に向けた取り組みは、プロセスの合理化と国境を越えた医療費償還を促進しています。

英国の医療費償還市場の洞察

英国の医療保険償還市場は、ほぼ全人口をカバーする国民保健サービス(NHS)への継続的な支援を背景に、着実な成長が見込まれています。患者中心の償還戦略への重点化と、予防医療および地域密着型ケアへの資金提供が拡大しています。請求提出やリアルタイムの支払い追跡のためのeヘルスプラットフォームの活用など、政府によるデジタル化の推進は業務効率の向上につながり、償還枠組みの強化につながっています。

ドイツの医療保険償還市場の洞察

ドイツの医療保険償還市場は、法定保険会社と民間保険会社からなる高度に構造化された二重支払者制度に支えられ、堅調な年平均成長率(CAGR)で成長すると予測されています。医療費の高騰、人口の高齢化、そして価値に基づくケアへの圧力が、特に慢性疾患および長期ケアサービスにおける償還請求を促進しています。さらに、電子患者記録とDRG(医療保険償還システム)に基づく病院償還の統合により、よりデータ主導型で透明性の高い償還環境が促進されています。

アジア太平洋地域の医療保険償還市場に関する洞察

アジア太平洋地域の医療費償還市場は、予測期間(2025~2032年)において、発展途上国における医療アクセスと保険普及率の拡大を背景に、最も高いCAGRを記録すると予想されています。中国、インド、インドネシアなどの国では、国民健康保険制度の導入・強化に向けた政府の取り組みが、償還制度の変革を促しています。デジタルヘルスの普及と遠隔医療サービスの増加も、請求件数の増加を促し、地域全体で償還モデルの近代化を必要としています。

日本医療保険償還市場インサイト

日本の医療保険償還市場は、国民皆保険制度と高齢化の進展によって牽引されており、特に慢性疾患や高齢者ケアにおいて、償還対象となる医療サービスに対する需要が高まっています。政府による定期的な診療報酬改定、請求審査へのAIの導入、そして高度なデジタルヘルスインフラの整備は、効率的な償還サイクルに貢献しています。さらに、先進医療に対する価値に基づく償還制度のイノベーションも勢いを増しています。

インドの医療保険償還市場の洞察

インドの医療保険償還市場は、アユシュマン・バーラトなどの政府資金による制度の拡大と民間保険の普及率上昇に後押しされ、2024年にはアジア太平洋地域で大きなシェアを獲得しました。急速な都市化、中間層の所得増加、そして医療のデジタル化は、公的部門と民間部門の両方で保険金請求件数の増加を促進しています。ヘルステック系スタートアップ企業と保険会社の連携強化も、保険金請求処理のスピードと透明性の向上に寄与しています。

医療費償還市場シェア

医療費償還業界は、主に次のような老舗企業によって主導されています。

- ユナイテッドヘルスグループ(米国)

- アエトナ社(米国)

- シグナ・ヘルスケア(米国)

- アンセム保険会社(米国)

- ヒューマナ(米国)

- センテーン・コーポレーション(米国)

- カイザー財団ヘルスプラン(米国)

- モリナ・ヘルスケア社(米国)

- ウェルケア・ヘルス・プランズ(米国)

- CVSヘルス(米国)

- ブパ(英国)

- AXA(フランス)

- アリアンツ(ドイツ)

- アビバ(英国)

- AOK – Die Gesundheitskasse (ドイツ)

- DKV(ドイツ)

- 日本生命保険株式会社(日本)

- 中国平安保険(グループ)有限公司(中国)

- マニュライフ(カナダ)

世界の医療保険償還市場の最新動向

- 2024年1月、マスターカードは、自社のバーチャルカード技術を活用したインドにおける医療費支払いに関する提携を発表しました。この取り組みは、医療分野における支払いプロセスの合理化を目指しています。

- 2024年1月、インドの総合保険評議会は、臨床施設法に基づき登録された15床の病院がキャッシュレス入院を提供できると発表しました。この措置は、保険加入者にとって医療へのアクセスを容易にすることを目的としています。

- 2024年4月、価値に基づくケアの導入を促進するための共同の取り組みとして、米国健康保険計画(AHIP)、米国医師会(AMA)、全米アカウンタブルケア組織協会(NAACOS)は、自主的なベストプラクティスを概説したプレイブックを発表しました。この取り組みは特に民間セクターを対象としており、従来の出来高払いモデルから、患者のアウトカムとケアの質を重視するモデルへの移行を加速することを目指しています。

- 2023年12月、米国のメディケア・メディケイドサービスセンター(CMS)は、従来のメディケア受給者全員を2023年12月までに価値に基づくケアモデルに移行させることを目指し、文書化と報告のための電子医療記録の活用を重視しました。これは、成果に基づく償還への移行が進んでいることを示しています。

- 2023年8月、AIを専門とする米国企業Codoxoは、医療費抑制と支払いの整合性プログラムを強化するために設計された生成AI製品「ClaimPilot」をリリースしました。このイノベーションは、入院患者と施設の請求監査を自動化することで、効率性を向上させ、人員の制約を軽減することを目指しています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。