>Mercado de integración de tecnología de la información (TI) de atención médica de EE. UU., por producto y servicios (producto y servicios), aplicación (integración de dispositivos médicos, integración interna, integración de hospitales, integración de laboratorios, integración de clínicas e integración de radiología), tamaño de las instalaciones (grandes, medianas y pequeñas), modo de compra (organización de compra grupal e individual), usuario final (hospitales, laboratorios, centros de diagnóstico, centros de radiología y clínicas): tendencias de la industria y pronóstico hasta 2029.

Análisis y perspectivas del mercado de integración de tecnología de la información (TI) en el sector sanitario de EE. UU.

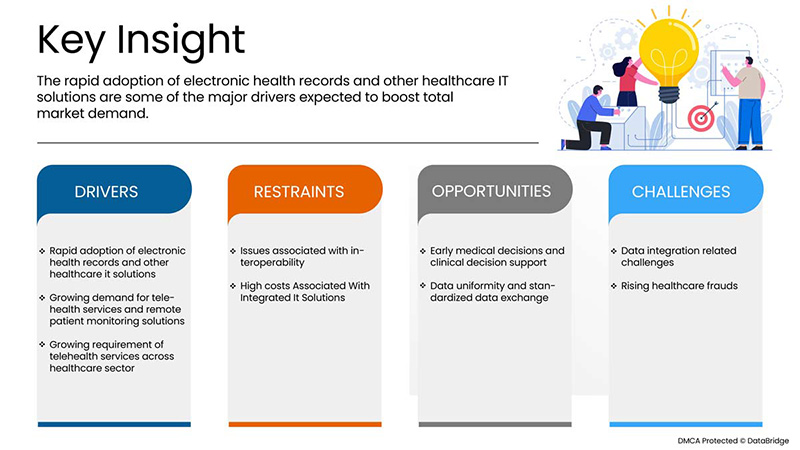

La creciente adopción de registros médicos electrónicos y otras soluciones de TI para el cuidado de la salud, la creciente demanda de servicios de telesalud y soluciones de monitoreo remoto de pacientes y el creciente requisito de servicios de telesalud en todo el sector de la salud son los factores que se espera que impulsen el crecimiento del mercado.

Sin embargo, se espera que los problemas asociados con la interoperabilidad y los altos costos asociados con las soluciones de TI integradas limiten el crecimiento del mercado.

Se espera que los avances tecnológicos en el campo de las imágenes para ensayos clínicos con fines de diagnóstico y tratamiento de enfermedades crónicas impulsen el crecimiento del mercado. Data Bridge Market Research analiza que el mercado de integración de tecnología de la información (TI) para el sector sanitario de EE. UU. crecerá a una tasa compuesta anual del 13,7 % durante el período de pronóstico de 2022 a 2029.

|

Métrica del informe |

Detalles |

|

Período de pronóstico |

2022 a 2029 |

|

Año base |

2021 |

|

Años históricos |

2020 (Personalizable para 2019-2014) |

|

Unidades cuantitativas |

Ingresos en millones de USD y precios en USD |

|

Segmentos cubiertos |

Por producto y servicios (Product and Services), aplicación (integración de dispositivos médicos, integración interna, integración de hospitales, integración de laboratorios, integración de clínicas e integración de radiología), tamaño de la instalación (grande, mediana y pequeña), modo de compra (organización de compra grupal e individual), usuario final (hospitales, laboratorios, centros de diagnóstico, centros de radiología y clínicas) |

|

Países cubiertos |

A NOSOTROS |

|

Actores del mercado cubiertos |

Lyniate, Redox, Inc., Carepoint Health, Nextgen Healthcare Inc., Interfaceware, Inc. Koninklijke Philips, Oracle, AVI-SPL, INC., Allscripts Healthcare solutions, Inc., Epic systems corporation, Qualcomm life Inc., Capsule Technologies Inc., Orion health, Quality syetems, Inc., Cerner corporation, Intersystems corporation, intersystem corporation, Infor Inc., GE Healthcare, MCKESSON Corporation, Meditech, entre otras. |

Definición de mercado

La integración de TI en el sector de la salud es el área de TI que implica el diseño, desarrollo, creación, uso y mantenimiento de sistemas de información para el sector de la salud. Los sistemas de información de salud automatizados e interoperables seguirán mejorando la atención médica y la salud pública, reduciendo los costos, aumentando la eficiencia, reduciendo los errores y mejorando la satisfacción del paciente, al mismo tiempo que optimizan el reembolso para los proveedores de atención médica ambulatoria y hospitalaria. La importancia de la TI en el sector de la salud es el resultado de la combinación de la evolución de la tecnología y las políticas gubernamentales cambiantes que influyen en la calidad de la atención al paciente.

Algunos de los productos de integración de TI para el cuidado de la salud son motores de interfaz/integración, software de integración de dispositivos médicos y soluciones y servicios de integración de medios, implementación e integración, soporte y mantenimiento, capacitación y educación, y consultoría. La TI para el cuidado de la salud permite a los proveedores de atención médica gestionar mejor la atención al paciente mediante el uso y el intercambio seguros de información médica. Al desarrollar registros médicos electrónicos (EHR) seguros y privados para la mayoría de los estadounidenses y hacer que la información médica esté disponible electrónicamente, cuando y donde se la necesite, la TI para el cuidado de la salud puede mejorar la calidad de la atención, al mismo tiempo que hace que la atención médica sea más rentable. Con la ayuda de la TI para el cuidado de la salud, los proveedores de atención médica tendrán información precisa y completa sobre la salud del paciente. De esa manera, los proveedores pueden brindar la mejor atención posible, ya sea durante una visita de rutina o una emergencia médica. Esto es especialmente importante si un paciente tiene una afección médica grave y esta es la forma de compartir información de manera segura con los pacientes y sus familiares a través de Internet.

Los pacientes y sus familias pueden participar plenamente en las decisiones sobre su atención médica y obtener información para ayudar a diagnosticar problemas de salud, reducir errores médicos y brindar una atención más segura a un menor costo. Durante el período de pronóstico, se prevé que los avances tecnológicos en la integración de TI en el sector de la atención médica impulsen el crecimiento del mercado.

Dinámica del mercado de integración de tecnologías de la información (TI) en el sector sanitario de EE. UU.

Conductores

- Adopción rápida de registros médicos electrónicos y otras soluciones informáticas para el cuidado de la salud

Los datos de los pacientes son complejos, confidenciales y, a menudo, no están estructurados. Incorporar esta información al proceso de prestación de servicios de salud es un desafío que se debe afrontar para aprovechar la oportunidad de mejorar la atención al paciente. Si bien el historial clínico electrónico (HER, por sus siglas en inglés) se ha utilizado durante más de una década, el mercado se ha acelerado recientemente debido a las iniciativas gubernamentales en diferentes países para mejorar la seguridad de los datos de los pacientes.

Por ejemplo,

- En junio de 2021, agencias de financiación de la salud como el Instituto Nacional de Salud (NIH), en EE. UU., habían financiado soluciones de TI para la atención médica digital.

- En marzo de 2020, la Oficina del Coordinador Nacional de Tecnologías de Información en Salud (ONC) emitió un informe sobre la oportunidad de financiamiento (NOFO), en el marco de los Proyectos de Aceleración de Vanguardia (LEAP) en Tecnologías de Información en Salud (TI en Salud).

Los servicios de TI ayudan a integrar a distintos usuarios finales en todo el sistema de atención sanitaria, incluidos hospitales, unidades de enfermería, farmacias y compañías de seguros de salud. Sin embargo, la integración de estos datos y su disponibilidad en tiempo real son esenciales para que los profesionales de la salud aseguren una toma de decisiones eficaz. Se espera que la rápida adopción de registros médicos electrónicos y otras soluciones de TI para la atención sanitaria impulse el crecimiento del mercado.

- Creciente demanda de servicios de telesalud y soluciones de monitoreo remoto de pacientes

En la actualidad, los servicios de telesalud se solicitan para fines de monitoreo y consultoría. Los avances en las soluciones de atención médica han ayudado a ofrecer contenido educativo y garantizar una comunicación ininterrumpida entre pacientes y proveedores de atención médica. El funcionamiento exitoso de las soluciones de monitoreo remoto de pacientes depende de la integración exitosa de dispositivos médicos y de Tecnologías de la Información y las Comunicaciones (TIC) que permitan la prestación de servicios médicos a largas distancias.

Por ejemplo,

- En 2021, según un informe del Departamento de Salud y Servicios Humanos de EE. UU., se descubrió que el uso de telesalud de Medicare aumentó 63 veces entre 2019 y 2020.

- En julio de 2020, en Europa, un estudio realizado por HIMSS y Siemens Healthineers descubrió que el 93% de los centros de atención médica habían adoptado al menos un tipo de servicio o solución de telemedicina justo antes del brote de COVID-19.

Con los avances tecnológicos, estas soluciones desempeñan un papel importante en la mejora de la monitorización remota y el cumplimiento del tratamiento por parte de los pacientes, y, en consecuencia, de su calidad de vida. Por lo tanto, se espera que la creciente demanda de soluciones de monitorización remota y de dispositivos remotos impulse el crecimiento de los proveedores de soluciones de integración de tecnología de la información (TI) para el sector sanitario de EE. UU. en los próximos años.

Oportunidades

- Decisiones médicas tempranas y apoyo a la toma de decisiones clínicas

La tecnología ha abierto puertas para mejorar y respaldar la atención médica, que desempeña un papel importante a la hora de hacer que la medicina sea más precisa y dar forma a la prestación de atención. Las tecnologías innovadoras, como la inteligencia artificial, la robótica y la automatización, son facilitadores cruciales para expandir la medicina de precisión, transformar la prestación de atención médica y mejorar la experiencia del paciente.

Por ejemplo,

- En 2020, según el Centro Nacional de Información Biotecnológica (NCBI), el sistema de apoyo a la toma de decisiones clínicas (CDSS) tiene como objetivo mejorar la prestación de servicios de atención médica al mejorar las decisiones médicas con conocimiento clínico específico, información del paciente y otra información de salud.

Las decisiones médicas que se toman son principalmente fructíferas, ya que afectan significativamente el desarrollo de mejores y más avanzados productos de imágenes médicas en el mercado. Por lo tanto, se espera que el aumento de las decisiones médicas tempranas y el apoyo a las decisiones clínicas generen una mayor oportunidad para el mercado.

- Aumentar la concienciación entre las personas

La integración de TI para el cuidado de la salud ofrece opciones alternativas para recibir servicios de salud en los EE. UU., lo que mejora el acceso y reduce los costos asociados con los viajes para recibir servicios. Sin embargo, no se ha aprovechado todo el potencial de la TI para el cuidado de la salud debido a su adopción lenta y fragmentada.

Por ejemplo,

- En 2019, según el Centro Nacional de Información Biotecnológica (NCBI), el Software para la Evolución del Conocimiento en Medicina (SEKMED) es una plataforma web de trabajo interactiva y dinámica que emplea un enfoque multidimensional del conocimiento, que considera las diversas dimensiones vinculadas a la práctica clínica, como la científica, la organizativa, la profesional y la experiencial. La solución también permite la colaboración y las interacciones a través de un proceso iterativo y continuo de generación de conocimiento respaldado por la participación de la comunidad de práctica.

Estos programas y eventos de concientización han aumentado el crecimiento del mercado y han brindado oportunidades para que las empresas crezcan, ya que estos programas o publicaciones de concientización ayudan a las personas a comprender las necesidades o requisitos de la integración de TI en el sector de la salud.

Restricciones/Desafíos

- Altos costos asociados con soluciones de TI integradas

Los altos costos iniciales de adquisición, los costos de mantenimiento continuos y las interrupciones en los flujos de trabajo que contribuyen a pérdidas temporales actúan como un freno para el crecimiento del mercado.

Por ejemplo,

- Según ScienceSoft USA Corporation, el costo del software de ultrasonido es de USD 30.000 para integrar una solución de atención médica con un sistema EHR y se requieren USD 150.000 para habilitar las capacidades de integración de EHR de un producto de software.

Además, se espera que los costos de mantenimiento y soporte después de la implementación de la integración de EHR obstaculicen aún más el crecimiento del mercado.

- Desafíos relacionados con la integración de datos

La información relacionada con los pacientes se ha creado desde diferentes departamentos y en todos los puntos de tratamiento dentro de la organización de atención médica, lo que hace que sea una industria con un uso intensivo de la información y registros de pacientes más confiables. Sin embargo, es esencial brindar información confiable mediante la combinación de grandes cantidades de datos para producir registros de pacientes completos y confiables. Debido a que se utilizan una variedad de equipos médicos e instrumentos de diagnóstico en los sistemas de atención médica, existe una creciente necesidad de conectar todos estos sistemas para ayudar a los profesionales de la salud a responder rápidamente en varios puntos de prestación de atención.

Por ejemplo,

- En octubre de 2016, según el informe publicado en la Conferencia Internacional sobre Innovaciones en Ciencia, Ingeniería y Tecnología (ICISET) de 2016, se mencionaron y analizaron diferentes problemas para la integración de datos de atención médica en Bangladesh para desarrollar un almacén de datos de salud a nivel nacional para el ciudadano y descubrir el conocimiento oculto de diferentes repositorios de datos de salud requiere la integración de datos de salud de fuentes ampliamente diversificadas.

Impacto de la COVID-19 en el mercado de integración de tecnologías de la información (TI) sanitarias de EE. UU.

Los servicios de diagnóstico por imágenes han sido lentos y complicados debido a la necesidad de prácticas estrictas de prevención y control de infecciones desarrolladas para contener el riesgo de transmisión y proteger al personal de atención médica. Por lo tanto, la decisión de obtener imágenes de pacientes sospechosos o pacientes con COVID-19 positivo se basa en su impacto en la mejora del estado del paciente. El uso de tecnología de la información sanitaria (HIT) durante la pandemia de la enfermedad por coronavirus 2019 (COVID-19) ha aumentado rápidamente. Durante la pandemia, la HIT se ha utilizado para brindar servicios de telesalud, educación sobre la enfermedad por coronavirus 2 del síndrome respiratorio agudo severo, actualizaciones sobre epidemiología y tratamientos y, más recientemente, acceso a sistemas de programación para las vacunas contra la COVID-19.

Acontecimientos recientes

- En agosto de 2022, Oracle anunció la disponibilidad de conexiones directas rápidas a Oracle Cloud Infrastructure (OCI) que ayudan a las instituciones miembros de Internet2 a realizar la transición a la nube. A través de una conexión de red dedicada a Internet2 Cloud Connect, las instituciones pueden utilizar sus conexiones a Internet2 existentes para ampliar su centro de datos a OCI en cuestión de días sin cargo adicional de Internet2 por hasta 5 Gbps. Esto facilita que las organizaciones accedan y utilicen los recursos de la nube para respaldar la investigación, la colaboración y la empresa académica sin nuevas inversiones significativas.

- En junio de 2022, Epic Systems Corporation anunció su plan de unirse a un nuevo marco de intercambio de información sanitaria para mejorar la interoperabilidad de los datos sanitarios en todo el país. El Trusted Exchange Framework and Common Agreement (TEFCA) ha unido las redes de información para ayudar a garantizar que todas las personas se beneficien de registros sanitarios completos y longitudinales dondequiera que reciban atención. Esto ha ayudado a la empresa a expandir su negocio.

Alcance del mercado de integración de tecnología de la información (TI) en el sector sanitario de EE. UU.

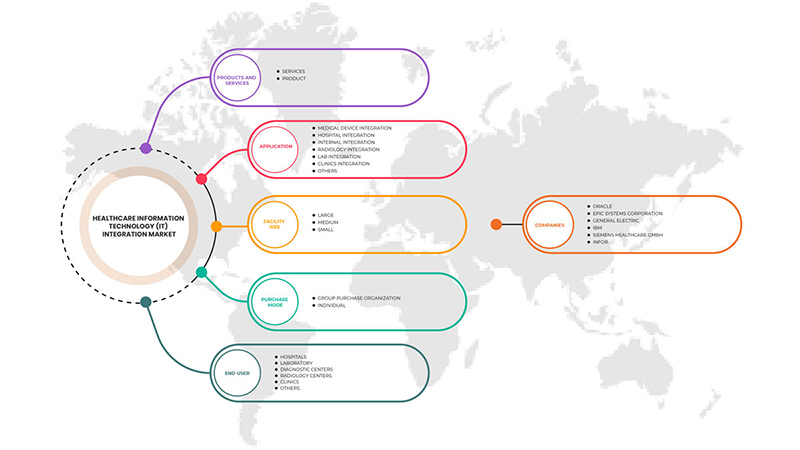

El mercado de integración de tecnología de la información (TI) para el sector sanitario de EE. UU. está segmentado en cinco segmentos importantes según el producto y los servicios, la aplicación, el tamaño de las instalaciones, el modo de compra y el usuario final. El crecimiento entre estos segmentos le ayudará a analizar los segmentos de crecimiento reducido de las industrias y a proporcionar a los usuarios una valiosa descripción general del mercado y conocimientos del mercado para ayudarlos a tomar decisiones estratégicas para identificar las principales aplicaciones del mercado.

Productos y servicios

- Servicios

- Producto

En función del producto y servicio, el mercado se segmenta en servicios y productos.

Solicitud

- Integración de dispositivos médicos

- Integración interna

- Integración hospitalaria

- Integración de laboratorio

- Integración de Clínicas

- Integración de radiología

- Otras aplicaciones

Según la aplicación, el mercado está segmentado en integración de dispositivos médicos, integración interna, integración de hospitales , integración de laboratorios, integración de clínicas , integración de radiología y otras aplicaciones.

Tamaño de la instalación

- Grande

- Medio

- Pequeño

Según el tamaño de las instalaciones, el mercado se segmenta en grande, mediano y pequeño.

Modo de compra

- Organización de compras grupales

- Individual

Según el modo de compra, el mercado se segmenta en organizaciones de compra grupal e individuales.

Usuario final

- Hospitales

- Laboratorio

- Centros de diagnóstico

- Centros de radiología

- Clínicas

- Otros

Según el usuario final, el mercado está segmentado en hospitales, laboratorios, centros de diagnóstico , centros de radiología, clínicas y otros.

Análisis y perspectivas regionales del mercado de integración de tecnología de la información (TI) en el sector sanitario de EE. UU.

Se analiza el mercado de integración de tecnología de la información (TI) de atención médica de EE. UU. y se brindan información y tendencias sobre el tamaño del mercado por regiones, productos y servicios, aplicaciones, tamaño de las instalaciones, modo de compra y usuario final como se mencionó anteriormente.

El país cubierto en este informe de mercado es EE. UU.

Se espera que Estados Unidos domine el mercado debido a su última tecnología avanzada e invenciones en integración de TI en el ámbito de la atención médica.

La sección de países del informe también proporciona factores individuales que impactan en el mercado y cambios en las regulaciones en el mercado a nivel nacional que afectan las tendencias actuales y futuras del mercado. Los puntos de datos como nuevas ventas, ventas de reemplazo, demografía del país, epidemiología de enfermedades y aranceles de importación y exportación son algunos de los principales indicadores utilizados para pronosticar el escenario del mercado para países individuales. Además, se consideran la presencia y disponibilidad de marcas norteamericanas y los desafíos que enfrentan debido a la gran o escasa competencia de las marcas locales y nacionales que impactan en los canales de venta al proporcionar un análisis de pronóstico de los datos del país.

Análisis del panorama competitivo y de la cuota de mercado de integración de tecnologías de la información (TI) sanitarias en EE. UU.

El panorama competitivo del mercado de integración de tecnología de la información (TI) para el cuidado de la salud de EE. UU. brinda detalles sobre los competidores. Los detalles incluidos son una descripción general de la empresa, las finanzas de la empresa, los ingresos generados, el potencial de mercado, la inversión en I+D, las nuevas iniciativas de mercado, la presencia en América del Norte, los sitios e instalaciones de producción, las capacidades de producción, las fortalezas y debilidades de la empresa, el lanzamiento de productos, la amplitud y la variedad de productos y el dominio de las aplicaciones. Los puntos de datos anteriores proporcionados solo están relacionados con el enfoque de las empresas en relación con el mercado de integración de tecnología de la información (TI) para el cuidado de la salud de EE. UU.

Algunos de los principales actores que operan en el mercado son Lyniate, Redox, Inc., carepoint health, Nextgen Healthcare Inc., Interfaceware, Inc. Koninklijke Philips, Oracle, AVI-SPL, INC., Allscripts Healthcare solutions, Inc, Epic systems corporation, Qualcomm life Inc., Capsule Technologies Inc. Orion health, Quality syetems, Inc., Cerner corporation, Intersystems corporation, intersystem corporation, Infor Inc., GE Healthcare, MCKESSON Corporation, Meditech entre otros.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Tabla de contenido

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 MULTIVARIATE MODELLING

2.7 MARKET APPLICATION COVERAGE GRID

2.8 PRODUCT AND SERVICES LIFELINE CURVE

2.9 DBMR MARKET POSITION GRID

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHT

4.1 POTENTIAL HEALTHCARE IT TECHNOLOGIES

4.1.1 ELECTRONIC HEALTH RECORDS (EHRS)

4.1.2 ELECTRONIC MEDICAL RECORDS (EMRS)

4.1.3 ARTIFICIAL INTELLIGENCE (AI)

4.1.4 TELEMEDICINE

5 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET SHARE ANALYSIS-

6 REGULATIONS

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 RAPID ADOPTION OF ELECTRONIC HEALTH RECORDS AND OTHER HEALTHCARE IT SOLUTIONS

7.1.2 GROWING DEMAND FOR TELEHEALTH SERVICES AND REMOTE PATIENT MONITORING SOLUTIONS

7.1.3 GROWING REQUIREMENT OF TELEHEALTH SERVICES ACROSS HEALTHCARE SECTOR

7.2 RESTRAINTS

7.2.1 ISSUES ASSOCIATED WITH INTEROPERABILITY

7.2.2 HIGH COSTS ASSOCIATED WITH INTEGRATED IT SOLUTIONS

7.3 OPPORTUNITIES

7.3.1 EARLY MEDICAL DECISIONS AND CLINICAL DECISION SUPPORT

7.3.2 DATA UNIFORMITY AND STANDARDIZED DATA EXCHANGE

7.3.3 INCREASING AWARENESS AMONG PEOPLE

7.4 CHALLENGES

7.4.1 DATA INTEGRATION RELATED CHALLENGES

7.4.2 RISING HEALTHCARE FRAUDS

8 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT AND SERVICES

8.1 OVERVIEW

8.2 SERVICES

8.2.1 SUPPORT & MAINTENANCE

8.2.2 IMPLEMENTATION & INTEGRATION

8.2.3 TRAINING & EDUCATION

8.2.4 CONSULTING

8.3 PRODUCT

8.3.1 INTERFACE/INTEGRATION ENGINES

8.3.1.1 Group Purchase Organization

8.3.1.2 Individual

8.3.2 MEDICAL DEVICE INTEGRATION SOFTWARE

8.3.2.1 Group Purchase Organization

8.3.2.2 Individual

8.3.3 MEDIA INTEGRATION SOLUTIONS

8.3.3.1 Group Purchase Organization

8.3.3.2 Individual

8.3.4 OTHER INTEGRATION TOOLS

9 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY APPLICATION

9.1 OVERVIEW

9.2 MEDICAL DEVICE INTEGRATION

9.3 HOSPITAL INTEGRATION

9.4 INTERNAL INTEGRATION

9.5 RADIOLOGY INTEGRATION

9.6 LAB INTEGRATION

9.7 CLINICS INTEGRATION

9.8 OTHERS

10 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY FACILITY SIZE

10.1 OVERVIEW

10.2 LARGE

10.3 MEDIUM

10.4 SMALL

11 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PURCHASE MODE

11.1 OVERVIEW

11.2 GROUP PURCHASE ORGANIZATION

11.3 INDIVIDUAL

12 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY END USER

12.1 OVERVIEW

12.2 HOSPITAL

12.3 DIAGNOSTIC CENTERS

12.4 RADIOLOGY CENTERS

12.5 LABORATORY

12.6 CLINICS

12.7 OTHERS

13 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: COMPANY LANDSCAPE

13.1 COMPANY SHARE ANALYSIS: U.S.

14 SWOT ANALYSIS

15 COMPANY PROFILE

15.1 ORACLE (BOTH PROVIDERS)

15.1.1 COMPANY SNAPSHOT

15.1.2 REVENUE ANALYSIS

15.1.3 PRODUCT PORTFOLIO

15.1.4 RECENT DEVELOPMENTS

15.2 EPIC SYSTEMS CORPORATION (EMR PROVIDERS)

15.2.1 COMPANY SNAPSHOT

15.2.2 PRODUCT PORTFOLIO

15.2.3 RECENT DEVELOPMENT

15.3 GENERAL ELECTRIC

15.3.1 COMPANY SNAPSHOT

15.3.2 REVENUE ANALYSIS

15.3.3 PRODUCT PORTFOLIO

15.3.4 RECENT DEVELOPMENTS

15.4 IBM (INTEGRATION PROVIDERS)

15.4.1 COMPANY SNAPSHOT

15.4.2 REVENUE ANALYSIS

15.4.3 PRODUCT PORTFOLIO

15.4.4 RECENT DEVELOPMENTS

15.5 SIEMENS HEALTHCARE GMBH (INTEGRATION PROVIDERS)

15.5.1 COMPANY SNAPSHOT

15.5.2 REVENUE ANALYSIS

15.5.3 PRODUCT PORTFOLIO

15.5.4 RECENT DEVELOPMENTS

15.6 ALLSCRIPTS HEALTHCARE, LLC AND/OR ITS AFFILIATES. (EMR PROVIDERS)

15.6.1 COMPANY SNAPSHOT

15.6.2 REVENUE ANALYSIS

15.6.3 PRODUCT PORTFOLIO

15.6.4 RECENT DEVELOPMENTS

15.7 COGNIZANT (INTEGRATION PROVIDERS)

15.7.1 COMPANY SNAPSHOT

15.7.2 REVENUE ANALYSIS

15.7.3 PRODUCT PORTFOLIO

15.7.4 RECENT DEVELOPMENTS

1.5 INFOR.

15.7.5 COMPANY SNAPSHOT

15.7.6 PRODUCT PORTFOLIO

15.7.7 RECENT DEVELOPMENT

15.8 INTERSYSTEM CORPORATION (INTRGRATION PROVIDERS)

15.8.1 COMPANY SNAPSHOT

15.8.2 PRDUCT PORTFOLIO

15.8.3 RECENT DEVELOPMENTS

15.9 INTERFACEWARE INC.(INTEGRATION PROVIDERS)

15.9.1 COMPANY SNAPSHOT

15.9.2 PRODUCT PORTFOLIO

15.9.3 RECENT DEVELOPMENTS

15.1 KONNKLIJKE PHILIPS N.V. (2021) (BOTH PROVIDERS)

15.10.1 COMPANY SNAPSHOT

15.10.2 REVENUE ANALYSIS

15.10.3 PRODUCT PORTFOLIO

15.10.4 RECENT DEVELOPMENTS

15.11 LYNIATE

15.11.1 COMPANY SNAPSHOT

15.11.2 PRODUCT PORTFOLIO

15.11.3 RECENT DEVELOPMENTS

15.12 MASIMO (2021) (INTEGRATION PROVIDERS)

15.12.1 COMPANY SNAPSHOT

15.12.2 REVENUE ANALYSIS

15.12.3 PRODUCT PORTFOLIO

15.12.4 RECENT DEVELOPMENT

15.13 MDI SOLUTIONS (INTGRATION PROVIDERS)

15.13.1 COMPANY SNAPSHOT

15.13.2 PRODUCT PORTFOLIO

15.13.3 RECENT DEVELOPMENTS

15.14 MEDICAL INFORMATION TECHNOLOGY, INC. (EMR PROVIDERS)

15.14.1 COMPANY SNAPSHOT

15.14.2 PRODUCT PORTFOLIO

15.14.3 RECENT DEVELOPMENTS

15.15 NXGN MANAGEMENT, LLC (EMR PROVIDERS)

15.15.1 COMPANY SNAPSHOT

15.15.2 REVENUE ANALYSIS

15.15.3 PRODUCT PORTFOLIO

15.15.4 RECENT DEVELOPMENTS

15.16 ORION HEALTH GROUP (INTEGRATION PROVIDERS)

15.16.1 COMPANY SNAPSHOT

15.16.2 REVENUE ANALYSIS

1.11.3. PRODUCT PORTFOLIO 115

15.16.3 RECENT DEVELOPMENTS

15.17 REDOX, INC.(INTEGRATION PROVIDERS)

15.17.1 COMPANY SNAPSHOT

15.17.2 PRODUCT PORTFOLIO

15.17.3 RECENT DEVELOPMENTS

15.18 SUMMIT HEALTHCARE SERVICES, INC.(INTEGRATION PROVIDERS)

15.18.1 COMPANY SNAPSHOT

15.18.2 PRODUCT PORTFOLIO

15.18.3 RECENT DEVELOPMENTS

15.19 QVERA (INTEGRATION PROVIDERS)

15.19.1 COMPANY SNAPSHOT

15.19.2 PRODUCT PORTFOLIO

15.19.3 RECENT DEVELOPMENTS

16 QUESTIONNAIRE

17 RELATED REPORTS

Lista de Tablas

TABLE 1 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 2 U.S. SERVICES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 3 U.S. PRODUCT IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 4 U.S. INTERFACE/INTEGRATION ENGINES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 5 U.S. MEDICAL DEVICE INTEGRATION SOFTWARE IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 6 U.S. MEDIA INTEGRATION SOLUTIONS IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 7 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 8 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY FACILITY SIZE, 2020-2029 (USD MILLION)

TABLE 9 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PURCHASE MODE, 2020-2029 (USD MILLION)

TABLE 10 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY END USER, 2020-2029 (USD MILLION)

Lista de figuras

FIGURE 1 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: SEGMENTATION

FIGURE 2 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: DATA TRIANGULATION

FIGURE 3 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: DROC ANALYSIS

FIGURE 4 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: REGIONAL VS COUNTRY MARKET ANALYSIS

FIGURE 5 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: MARKET APPLICATION COVERAGE GRID

FIGURE 8 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: DBMR MARKET POSITION GRID

FIGURE 9 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: SEGMENTATION

FIGURE 10 GROWING DEMAND FOR HEALTHCARE IT SOLUTIONS, TELEHEALTH SERVICES, AND REMOTE PATIENT MONITORING SOLUTIONS ARE EXPECTED TO DRIVE THE U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 11 SERVICES SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET FROM 2022 TO 2029

FIGURE 12 DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES OF U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET

FIGURE 13 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PRODUCT AND SERVICES, 2021

FIGURE 14 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PRODUCT AND SERVICES, 2022-2029 (USD MILLION)

FIGURE 15 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PRODUCT AND SERVICES, CAGR (2022-2029)

FIGURE 16 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PRODUCT AND SERVICES, LIFELINE CURVE

FIGURE 17 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY APPLICATION, 2021

FIGURE 18 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY APPLICATION, 2022-2029 (USD MILLION)

FIGURE 19 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY APPLICATION, CAGR (2022-2029)

FIGURE 20 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY APPLICATION, LIFELINE CURVE

FIGURE 21 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY FACILITY SIZE, 2021

FIGURE 22 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY FACILITY SIZE, 2022-2029 (USD MILLION)

FIGURE 23 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY FACILITY SIZE, CAGR (2022-2029)

FIGURE 24 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY FACILITY SIZE, LIFELINE CURVE

FIGURE 25 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PURCHASE MODE, 2021

FIGURE 26 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PURCHASE MODE, 2022-2029 (USD MILLION)

FIGURE 27 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PURCHASE MODE, CAGR (2022-2029)

FIGURE 28 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PURCHASE MODE, LIFELINE CURVE

FIGURE 29 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY END USER, 2021

FIGURE 30 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 31 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY END USER, CAGR (2022-2029)

FIGURE 32 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY END USER, LIFELINE CURVE

FIGURE 33 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: COMPANY SHARE 2021 (%)

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.