Asia Pacific Departmental Pacs Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

3.39 Billion

USD

5.52 Billion

2024

2032

USD

3.39 Billion

USD

5.52 Billion

2024

2032

| 2025 –2032 | |

| USD 3.39 Billion | |

| USD 5.52 Billion | |

| % | |

|

Segmentación del mercado de PACS departamentales de Asia-Pacífico (PACS), por tipo de producto (PACS tradicionales y especializados), componente (software, servicios y hardware), aplicación (resonancia magnética, tomografía computarizada, radiografía digital, ultrasonido, imágenes nucleares, arcos en C y otros), nivel de integración (PACS integrados y autónomos), usuario final (hospitales, cadenas/centros de radiología, centros de cirugía ambulatoria y otros), canal de distribución (licitaciones directas, administradores externos y otros): tendencias del sector y pronóstico hasta 2032.

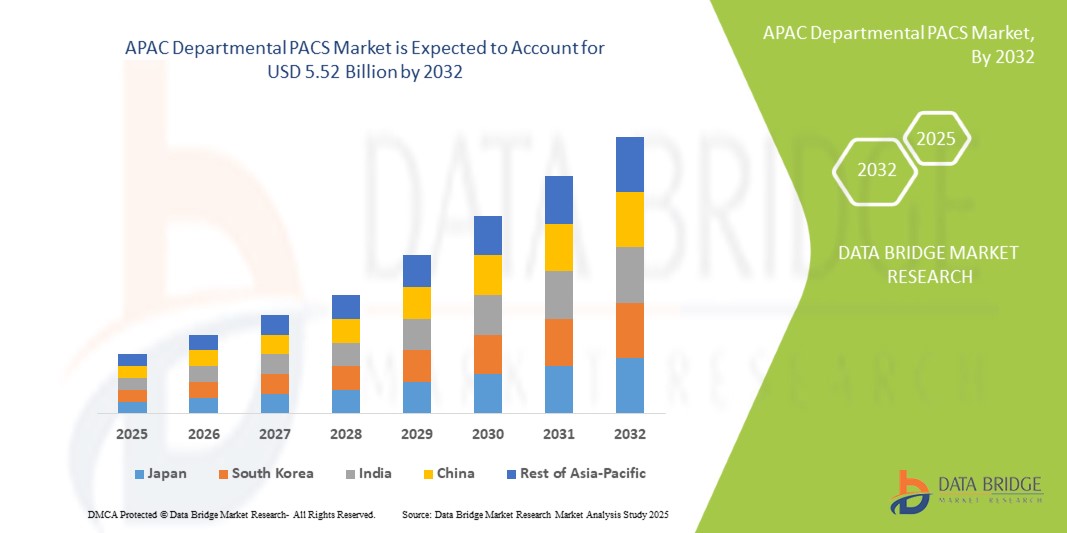

Tamaño del mercado de PACS departamentales de APAC

- El tamaño del mercado de PACS departamental de APAC se valoró enUSD 3.390 millones en 2024y se espera que alcance5.520 millones de dólares para 2032, en unCAGR del 6,30 %durante el período de pronóstico

- Este crecimiento está impulsado por factores como la creciente digitalización de la atención médica, la creciente prevalencia de enfermedades crónicas, los avances tecnológicos, las iniciativas gubernamentales, la mejora de la infraestructura y la adopción en las economías emergentes.

Análisis del mercado de PACS departamentales de APAC

- El mercado de PACS departamentales está experimentando una expansión constante, impulsado por la creciente adopción de tecnologías sanitarias avanzadas en las instituciones médicas. Los hospitales y centros de diagnóstico integran cada vez más estos sistemas para optimizar el flujo de trabajo y la atención al paciente.

- La demanda de soluciones PACS departamentales también se ve influenciada por la creciente necesidad de sistemas eficientes de almacenamiento y recuperación de datos en imágenes médicas. Estos sistemas proporcionan acceso centralizado a las imágenes de los pacientes, mejorando la precisión diagnóstica y reduciendo los costos operativos.

- Se espera que China domine el mercado de PACS departamental de APAC debido a su infraestructura de atención médica avanzada, la alta adopción de tecnologías de imágenes digitales y la fuerte presencia de proveedores líderes de PACS.

- Se espera que India sea la región de más rápido crecimiento en el mercado PACS departamental de APAC durante el período de pronóstico debido a la rápida digitalización de la atención médica, las crecientes inversiones en imágenes médicas y la creciente demanda de soluciones de diagnóstico eficientes.

- Se espera que el segmento PACS especializado domine el mercado con una participación de mercado del 28 % en 2025 debido a sus funcionalidades personalizadas para especialidades médicas específicas, mejorando la precisión del diagnóstico y la eficiencia del flujo de trabajo.

Alcance del informe y segmentación del mercado PACS departamental de APAC

|

Atributos |

Perspectivas clave del mercado de los PACS departamentales de APAC |

|

Segmentos cubiertos |

|

|

Países cubiertos |

Asia-Pacífico

|

|

Actores clave del mercado |

|

|

Oportunidades de mercado |

|

|

Conjuntos de información de datos de valor añadido |

Además de los conocimientos sobre escenarios de mercado, como el valor de mercado, la tasa de crecimiento, la segmentación, la cobertura geográfica y los principales actores, los informes de mercado seleccionados por Data Bridge Market Research también incluyen un análisis profundo de expertos, epidemiología de pacientes, análisis de la cartera de productos, análisis de precios y marco regulatorio. |

Tendencias del mercado de PACS departamentales de APAC

“Aumentar la integración deInteligencia artificialen sistemas de imágenes”

- La IA está revolucionando las industrias, mejorando la eficiencia, la precisión y la funcionalidad de los sistemas de imágenes.

- Por ejemplo, DeepMind de Google ha desarrollado un sistema de IA que supera a los expertos humanos en el diagnóstico de enfermedades oculares a partir de escáneres de retina.

- En el ámbito sanitario, los algoritmos de IA analizan imágenes médicas (radiografías, resonancias magnéticas, tomografías computarizadas, ecografías) con alta precisión.

- Por ejemplo, el software de inteligencia artificial de Aidoc ayuda a los radiólogos a identificar rápidamente casos críticos en tomografías computarizadas, lo que reduce el tiempo de respuesta en la atención de emergencia.

- La IA ayuda a detectar afecciones como cáncer, enfermedades cardiovasculares y trastornos neurológicos de forma más temprana y precisa.

- Por ejemplo, los modelos de aprendizaje profundo de PathAI ayudan a los patólogos a diagnosticar tejidos cancerosos con mayor precisión, reduciendo los errores de diagnóstico.

- La IA puede identificar patrones en imágenes que los expertos humanos podrían pasar por alto, lo que conduce a diagnósticos más rápidos y confiables.

- Por ejemplo, el sistema de IA desarrollado por Enlitic ha demostrado que puede detectar fracturas sutiles en radiografías que a menudo los radiólogos pasan por alto.

- En seguridad, los sistemas de imágenes impulsados por IA se utilizan para el reconocimiento facial y la vigilancia para monitorear actividades e identificar a las personas.

Dinámica del mercado de PACS departamentales de APAC

Conductor

Creciente demanda de detección temprana de enfermedades

- La creciente demanda de detección temprana de enfermedades está impulsando el mercado de PACS departamental de APAC

- Los proveedores de atención médica se están centrando en la atención preventiva, que requiere tecnologías de imágenes avanzadas para la identificación temprana de enfermedades.

- Los sistemas PACS permiten el almacenamiento, la recuperación y el uso compartido eficientes deimágenes médicas, lo que conduce a diagnósticos oportunos y precisos

- La detección temprana de enfermedades como el cáncer, las enfermedades cardiovasculares y los trastornos neurológicos produce mejores resultados para los pacientes.

- La integración de IA y aprendizaje automático con PACS mejora la precisión del diagnóstico y la eficiencia del flujo de trabajo, impulsando el crecimiento del mercado.

Por ejemplo,

- La solución PACS impulsada por IA de Aidoc ayuda a los radiólogos a identificar casos críticos en tomografías computarizadas con mayor rapidez, lo que mejora la velocidad del diagnóstico en situaciones de emergencia.

- La inteligencia artificial DeepMind de Google ha demostrado su capacidad de superar a los expertos humanos en el diagnóstico de enfermedades oculares a partir de exploraciones de retina, lo que ilustra el poder de la integración de IA en PACS para la detección temprana de enfermedades.

Oportunidad

Creciente demanda de soluciones PACS basadas en la nube

- La creciente demanda de soluciones PACS basadas en la nube presenta una oportunidad significativa en el mercado PACS departamental de APAC.

- Las organizaciones de atención médica buscan cada vez más reducir los costos de infraestructura y mejorar la escalabilidad.

- Los PACS basados en la nube ofrecen flexibilidad, menor inversión de capital inicial y mantenimiento simplificado en comparación con los sistemas locales tradicionales.

- Estos sistemas permiten a los proveedores de atención médica almacenar y acceder a datos de imágenes médicas de forma remota, lo que es especialmente beneficioso en regiones con infraestructura física limitada o para centros de atención médica que operan en múltiples ubicaciones.

- La escalabilidad de la nube ayuda a gestionar el creciente volumen de datos de imágenes médicas sin la necesidad de actualizaciones constantes de hardware.

Por ejemplo,

- Ambra Health ofrece soluciones PACS basadas en la nube que permiten a los proveedores de atención médica acceder y compartir datos de imágenes de forma remota, lo que reduce los costos de infraestructura y mejora la flexibilidad operativa.

- Everlight Radiology utiliza PACS basado en la nube para proporcionar informes de radiología en tiempo real, lo que permite el acceso a opiniones de expertos en áreas desatendidas, mejorando la atención al paciente y la eficiencia del diagnóstico.

Restricción/Desafío

“Altos costos asociados con la implementación”

- Los altos costos asociados con la implementación de sistemas de gestión de imágenes médicas, como PACS, actúan como una restricción importante para el mercado de PACS departamental de APAC.

- Los costos incluyen no sólo la inversión inicial en hardware y software, sino también los gastos continuos relacionados con el mantenimiento del sistema, las actualizaciones y la capacitación del personal.

- Los centros de atención sanitaria más pequeños y aquellos en regiones en desarrollo a menudo enfrentan limitaciones presupuestarias, lo que dificulta la asignación de fondos para soluciones de imágenes avanzadas.

- La carga financiera de integrar PACS con los sistemas de información hospitalaria existentes, garantizar la seguridad de los datos y cumplir con las regulaciones sanitarias aumenta aún más los costos.

- Estos desafíos económicos pueden disuadir a los proveedores de atención médica de adoptar la tecnología PACS a pesar de sus beneficios en la mejora de la precisión del diagnóstico y la eficiencia operativa.

Por ejemplo,

- En muchos hospitales rurales de la India, los altos costos de implementación de sistemas PACS han retrasado la adopción de estas tecnologías, limitando el acceso a herramientas de diagnóstico avanzadas.

- Un estudio de la Organización Mundial de la Salud (OMS) destacó que las pequeñas clínicas en el sudeste asiático tienen dificultades para afrontar los costos de instalación y mantenimiento de los sistemas PACS, lo que dificulta su capacidad de proporcionar servicios de imágenes de alta calidad.

Alcance del mercado de PACS departamentales de APAC

El mercado está segmentado según el tipo de producto, componente, aplicación, nivel de integración, usuario final y canal de distribución.

|

Segmentación |

Subsegmentación |

|

Por tipo de producto |

|

|

Por componente |

|

|

Por aplicación |

|

|

Por nivel de integración |

|

|

Por el usuario final |

|

|

Por canal de distribución |

|

Se proyecta que en 2025, las soluciones PACS especializadas dominarán el mercado con la mayor participación en el segmento de tipo de producto.

Se espera que el segmento de PACS especializados domine el mercado de PACS departamental de APAC con la mayor participación del 28 % en 2025. Gracias a sus soluciones personalizadas que atienden especialidades médicas específicas como oncología, cardiología, ortopedia y oftalmología, estos sistemas están diseñados para procesar datos de imágenes complejos, mejorando la precisión diagnóstica y la eficiencia del flujo de trabajo.

Se espera que la resonancia magnética represente la mayor participación durante el período de pronóstico en el mercado tecnológico.

En 2025, se prevé que el segmento de resonancia magnética domine el mercado con la mayor cuota de mercado, entre el 30 % y el 35 %, gracias a su papel fundamental en el diagnóstico no invasivo y a su capacidad para proporcionar imágenes de alta resolución de tejidos blandos. La resonancia magnética se utiliza ampliamente para diagnosticar trastornos neurológicos, problemas musculoesqueléticos, cánceres y otras afecciones complejas.

Análisis regional del mercado de PACS departamental de APAC

China posee la mayor participación en el mercado de PACS departamental de Asia-Pacífico.

- Se prevé que China tenga la mayor participación de mercado debido a su sólida infraestructura de atención médica y la adopción generalizada de tecnologías de imágenes avanzadas.

- Las importantes inversiones del país en digitalización de la atención sanitaria y en expansión de la red hospitalaria contribuyen a su posición de liderazgo en el mercado de PACS.

- Con el crecimiento de la industria de dispositivos médicos, China está bien posicionada para mantener su dominio en el sector PACS.

- Las iniciativas gubernamentales que apoyan las herramientas de salud digital fortalecen aún más la integración de los sistemas PACS en los centros de atención médica en China.

Se proyecta que India registre la CAGR más alta en el mercado de PACS departamental de Asia-Pacífico.

- Se prevé que India experimente la tasa de crecimiento anual compuesta (CAGR) más alta en el mercado PACS de APAC, impulsada por su sector de atención médica en expansión.

- La creciente demanda de soluciones de imágenes avanzadas en las industrias de dispositivos médicos y hospitales de la India, en rápido desarrollo, impulsa el rápido crecimiento del mercado.

- La industria de la salud de la India es un impulsor clave, ya que representa una parte significativa del sector médico en general, lo que impulsa la adopción de PACS.

- El creciente número de hospitales y centros de diagnóstico en la India resalta la necesidad de sistemas de imágenes eficientes, lo que acelera el crecimiento de PACS en la región.

Cuota de mercado de PACS departamentales de APAC

El panorama competitivo del mercado ofrece detalles por competidor. Se incluye información general de la empresa, sus estados financieros, ingresos generados, potencial de mercado, inversión en investigación y desarrollo, nuevas iniciativas de mercado, presencia global, plantas de producción, capacidad de producción, fortalezas y debilidades de la empresa, lanzamiento de productos, alcance y variedad de productos, y dominio de las aplicaciones. Los datos anteriores se refieren únicamente al enfoque de mercado de las empresas.

Los principales líderes del mercado que operan en el mercado son:

- Corporación FUJIFILM(Japón)

- Mach 7 Technologies Limited (Australia)

- Reyence (Japón)

- SinoVision (China)

- Servicios de informes de TeleRAD Private Limited (India)

- Corporación de sistemas médicos Canon(Japón)

- Konica Minolta, Inc.(Japón)

- INFINITT Salud(Corea del Sur)

- Samsung Medison(Corea del Sur)

Últimos avances en el mercado de PACS departamental de APAC

- En enero de 2024, FUJIFILM Diosynth Biotechnologies (EE. UU.) y SHL Medical (Suiza) firmaron una alianza estratégica para satisfacer la creciente demanda del mercado de medicamentos autoinyectables. Esta colaboración ampliará la capacidad de producción de FUJIFILM en Dinamarca, alcanzando hasta 30 millones de unidades anuales para principios de 2025. Mediante la integración de la plataforma de autoinyectores Molly de SHL, la alianza busca optimizar los procesos de producción y reducir los riesgos en la cadena de suministro. Este desarrollo beneficiará a las empresas farmacéuticas y biotecnológicas, al agilizar la comercialización y mejorar el acceso de los pacientes a los medicamentos autoinyectables.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.