سوق تكامل تكنولوجيا معلومات الرعاية الصحية في الولايات المتحدة، حسب المنتج والخدمات (المنتج والخدمات)، التطبيق (تكامل الأجهزة الطبية، التكامل الداخلي، تكامل المستشفيات، تكامل المختبرات، تكامل العيادات وتكامل الأشعة)، حجم المنشأة (كبيرة ومتوسطة وصغيرة)، وضع الشراء (منظمة الشراء الجماعي والفردية)، المستخدم النهائي (المستشفيات والمختبرات ومراكز التشخيص ومراكز الأشعة والعيادات) - اتجاهات الصناعة والتوقعات حتى عام 2029.

تحليل ورؤى حول سوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة

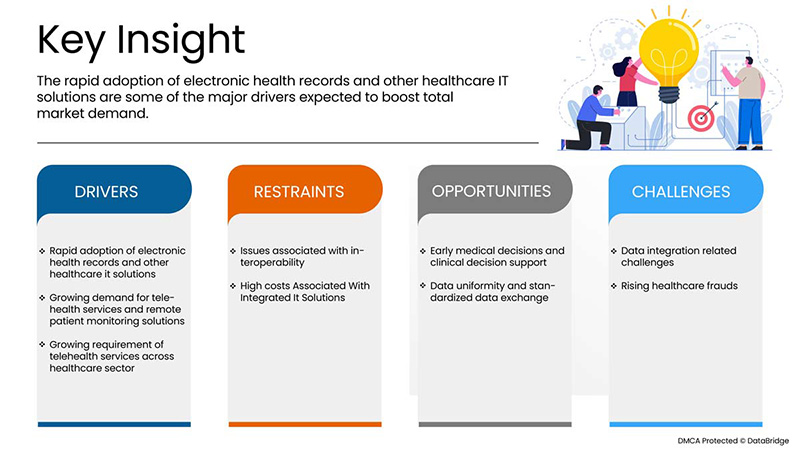

إن الاعتماد المتزايد على السجلات الصحية الإلكترونية وحلول الرعاية الصحية الأخرى، والطلب المتزايد على خدمات الرعاية الصحية عن بعد وحلول مراقبة المرضى عن بعد والمتطلبات المتزايدة لخدمات الرعاية الصحية عن بعد في قطاع الرعاية الصحية هي العوامل التي من المتوقع أن تدفع نمو السوق.

ومع ذلك، من المتوقع أن تعمل القضايا المرتبطة بالتوافق التشغيلي، والتكاليف المرتفعة المرتبطة بحلول تكنولوجيا المعلومات المتكاملة على تقييد نمو السوق.

من المتوقع أن يؤدي التقدم التكنولوجي المتزايد في التصوير التجريبي السريري لتشخيص وعلاج الأمراض المزمنة إلى دفع نمو السوق. تحلل شركة Data Bridge Market Research أن سوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة سينمو بمعدل نمو سنوي مركب يبلغ 13.7٪، خلال الفترة المتوقعة من 2022 إلى 2029.

|

تقرير القياس |

تفاصيل |

|

فترة التنبؤ |

2022 إلى 2029 |

|

سنة الأساس |

2021 |

|

سنوات تاريخية |

2020 (قابلة للتخصيص حتى 2019-2014) |

|

وحدات كمية |

الإيرادات بالملايين من الدولارات الأمريكية، والتسعير بالدولار الأمريكي |

|

القطاعات المغطاة |

حسب المنتج والخدمات (المنتج والخدمات)، التطبيق (تكامل الأجهزة الطبية، التكامل الداخلي، تكامل المستشفيات، تكامل المختبرات، تكامل العيادات وتكامل الأشعة)، حجم المنشأة (كبيرة ومتوسطة وصغيرة)، طريقة الشراء (منظمة شراء جماعية وفردية)، المستخدم النهائي (المستشفيات والمختبرات ومراكز التشخيص ومراكز الأشعة والعيادات) |

|

الدول المغطاة |

نحن |

|

الجهات الفاعلة في السوق المشمولة |

Lyniate، Redox، Inc.، carepoint health، Nextgen Healthcare Inc.، Interfaceware، Inc. Koninklijke Philips، Oracle، AVI-SPL، INC.، Allscripts Healthcare solutions، Inc، Epic systems corporation، Qualcomm life Inc.، Capsule technologies Inc. Orion health، Quality syetems، Inc.، Cerner corporation، Intersystems corporation، intersystem corporation، Infor Inc.، GE Healthcare، MCKESSON Corporation، Meditech وغيرها |

تعريف السوق

تكامل تكنولوجيا المعلومات في مجال الرعاية الصحية هو مجال تكنولوجيا المعلومات الذي يشمل تصميم وتطوير وإنشاء واستخدام وصيانة أنظمة المعلومات لصناعة الرعاية الصحية. ستستمر أنظمة معلومات الرعاية الصحية الآلية والمتوافقة في تحسين الرعاية الطبية والصحة العامة، وخفض التكاليف، وزيادة الكفاءة، والحد من الأخطاء وتحسين رضا المرضى، مع تحسين سداد تكاليف مقدمي الرعاية الصحية للمرضى الداخليين والخارجيين. تنبع أهمية تكنولوجيا المعلومات الصحية من الجمع بين التكنولوجيا المتطورة والسياسات الحكومية المتغيرة التي تؤثر على جودة رعاية المرضى.

إن بعض منتجات تكامل تكنولوجيا المعلومات في مجال الرعاية الصحية هي محركات الواجهة/التكامل، وبرامج تكامل الأجهزة الطبية وحلول وخدمات تكامل الوسائط، والتنفيذ والتكامل، والدعم والصيانة، والتدريب والتعليم، والاستشارات. إن تكنولوجيا المعلومات الصحية تجعل من الممكن لمقدمي الرعاية الصحية إدارة رعاية المرضى بشكل أفضل من خلال الاستخدام الآمن وتبادل المعلومات الصحية. ومن خلال تطوير السجلات الصحية الإلكترونية الآمنة والخاصة لمعظم الأميركيين وجعل المعلومات الصحية متاحة إلكترونيًا، متى وأينما كانت هناك حاجة إليها، يمكن لتكنولوجيا المعلومات الصحية تحسين جودة الرعاية، حتى مع جعل الرعاية الصحية أكثر فعالية من حيث التكلفة. وبمساعدة تكنولوجيا المعلومات الصحية، سيكون لدى مقدمي الرعاية الصحية معلومات دقيقة وكاملة حول صحة المريض. وبهذه الطريقة، يمكن لمقدمي الرعاية تقديم أفضل رعاية ممكنة، سواء أثناء زيارة روتينية أو حالة طبية طارئة. وهذا مهم بشكل خاص إذا كان المريض يعاني من حالة طبية خطيرة وهذه هي الطريقة لمشاركة المعلومات بشكل آمن مع المرضى وأفراد أسرهم عبر الإنترنت.

يمكن للمرضى وأسرهم المشاركة بشكل كامل في اتخاذ القرارات المتعلقة برعايتهم الصحية والمعلومات للمساعدة في تشخيص المشاكل الصحية والحد من الأخطاء الطبية وتوفير رعاية أكثر أمانًا بتكاليف أقل. ومن المتوقع أن تعمل التطورات التكنولوجية في تكامل تكنولوجيا المعلومات في مجال الرعاية الصحية خلال فترة التنبؤ على دفع نمو السوق.

ديناميكيات سوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة

السائقين

- التبني السريع للسجلات الصحية الإلكترونية وحلول تكنولوجيا المعلومات الصحية الأخرى

إن بيانات المرضى معقدة وسرية وغير منظمة في كثير من الأحيان. إن دمج هذه المعلومات في عملية تقديم الرعاية الصحية يشكل تحديًا يجب مواجهته من أجل استغلال الفرصة لتحسين رعاية المرضى. وعلى الرغم من أن السجل الصحي الإلكتروني (HER) قيد الاستخدام منذ أكثر من عقد من الزمان، فقد تسارعت وتيرة السوق مؤخرًا بسبب المبادرات الحكومية في بلدان مختلفة لتحسين أمان بيانات المرضى.

على سبيل المثال،

- في يونيو 2021، قامت وكالات تمويل الصحة مثل المعهد الوطني للصحة (NIH)، في الولايات المتحدة، بتمويل حلول تكنولوجيا المعلومات للرعاية الصحية الرقمية

- في مارس 2020، أصدر مكتب المنسق الوطني لتكنولوجيا المعلومات الصحية (ONC) تقريرًا عن فرصة التمويل (NOFO)، في إطار مشاريع تسريع الحافة الرائدة (LEAP) في تكنولوجيا المعلومات الصحية (Health IT)

تساعد خدمات تكنولوجيا المعلومات في دمج مختلف المستخدمين النهائيين في جميع أنحاء نظام الرعاية الصحية، بما في ذلك المستشفيات ووحدات التمريض والصيدليات وشركات التأمين الصحي. ومع ذلك، فإن دمج هذه البيانات وتوافرها في الوقت الفعلي أمر ضروري لمهنيي الرعاية الصحية لضمان اتخاذ قرارات فعالة. ومن المتوقع أن يؤدي التبني السريع للسجلات الصحية الإلكترونية وحلول تكنولوجيا المعلومات الأخرى في مجال الرعاية الصحية إلى دفع نمو السوق.

- الطلب المتزايد على خدمات الرعاية الصحية عن بعد وحلول مراقبة المرضى عن بعد

في الوقت الحالي، يتم طلب خدمات الرعاية الصحية عن بعد لأغراض المراقبة والاستشارات. وقد ساعد التقدم في حلول الرعاية الصحية في تقديم المحتوى التعليمي وضمان التواصل المستمر بين المرضى ومقدمي الرعاية الصحية. ويعتمد التشغيل الناجح لحلول مراقبة المرضى عن بعد على التكامل الناجح للأجهزة الطبية وتكنولوجيا المعلومات والاتصالات التي تمكن من تقديم الخدمات الطبية عبر مسافات طويلة.

على سبيل المثال،

- في عام 2021، وفقًا لتقرير صادر عن وزارة الصحة والخدمات الإنسانية الأمريكية، وجد أن استخدام الرعاية الصحية عن بعد في برنامج الرعاية الطبية زاد بمقدار 63 ضعفًا بين عامي 2019 و2020

- في يوليو 2020، وجدت دراسة أجرتها HIMSS وSiemens Healthineers في أوروبا أن 93% من مرافق الرعاية الصحية قد تبنت نوعًا واحدًا على الأقل من خدمات أو حلول الطب عن بعد قبل تفشي مرض كوفيد-19 مباشرة

مع التقدم في التكنولوجيا، تلعب هذه الحلول دورًا مهمًا في تحسين المراقبة عن بعد وامتثال المرضى، وبالتالي جودة حياتهم. لذلك، من المتوقع أن يؤدي الطلب المتزايد على حلول المراقبة عن بعد والأجهزة عن بعد إلى دفع نمو مزودي حلول تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة في السنوات القادمة.

فرص

- القرارات الطبية المبكرة ودعم القرارات السريرية

لقد فتحت التكنولوجيا الأبواب لتحسين ودعم الرعاية الصحية التي تلعب دورًا رئيسيًا في جعل الطب أكثر دقة وتشكيل تقديم الرعاية. تعد التقنيات المبتكرة، مثل الذكاء الاصطناعي والروبوتات والأتمتة، عوامل تمكينية حاسمة لتوسيع نطاق الطب الدقيق وتحويل تقديم الرعاية وتحسين تجربة المريض.

على سبيل المثال،

- في عام 2020، وفقًا للمركز الوطني لمعلومات التكنولوجيا الحيوية (NCBI)، يهدف نظام دعم القرار السريري (CDSS) إلى تحسين تقديم الرعاية الصحية من خلال تعزيز القرارات الطبية بالمعرفة السريرية المستهدفة ومعلومات المريض وغيرها من المعلومات الصحية

إن القرارات الطبية المتخذة مثمرة في المقام الأول لأنها تؤثر بشكل كبير على تطوير منتجات التصوير الطبي الأفضل والأكثر تقدمًا في السوق. لذلك، من المتوقع أن يؤدي الارتفاع في القرارات الطبية المبكرة ودعم القرار السريري إلى خلق فرصة أكبر للسوق.

- زيادة الوعي بين الناس

يقدم تكامل تكنولوجيا المعلومات في مجال الرعاية الصحية خيارات بديلة لتلقي خدمات الرعاية الصحية في الولايات المتحدة، مما يحسن الوصول ويقلل التكاليف المرتبطة بالسفر للحصول على الخدمات. ومع ذلك، لم يتم تحقيق الإمكانات الكاملة لتكنولوجيا المعلومات في مجال الرعاية الصحية مع الاستخدام البطيء والمجزأ.

على سبيل المثال،

- في عام 2019، وفقًا للمركز الوطني لمعلومات التكنولوجيا الحيوية (NCBI)، فإن برنامج تطوير المعرفة في الطب (SEKMED) عبارة عن منصة ويب تفاعلية وديناميكية تعمل على استخدام نهج متعدد الأبعاد للمعرفة، والذي يأخذ في الاعتبار الأبعاد المختلفة المرتبطة بالممارسة السريرية مثل العلمية والتنظيمية والمهنية والتجريبية. يسمح الحل أيضًا بالتعاون والتفاعل من خلال عملية تكرارية ومتواصلة لتوليد المعرفة بدعم من مشاركة مجتمع الممارسة.

لقد أدت هذه البرامج والأحداث التوعوية إلى زيادة نمو السوق وتوفير الفرص للشركات للنمو حيث تساعد هذه البرامج أو المنشورات التوعوية الأشخاص على الحصول على احتياجات أو متطلبات تكامل تكنولوجيا المعلومات في الرعاية الصحية.

القيود/التحديات

- التكاليف المرتفعة المرتبطة بحلول تكنولوجيا المعلومات المتكاملة

تشكل تكاليف الاستحواذ الأولية المرتفعة، وتكاليف الصيانة المستمرة، وانقطاعات سير العمل التي تساهم في الخسائر المؤقتة عائقًا أمام نمو السوق.

على سبيل المثال،

- وفقًا لشركة ScienceSoft USA Corporation، فإن تكلفة برنامج الموجات فوق الصوتية هي 30 ألف دولار أمريكي مطلوب لدمج حل الرعاية الصحية مع نظام EHR واحد، و150 ألف دولار أمريكي مطلوب لتمكين قدرات تكامل EHR لمنتج برمجي.

علاوة على ذلك، من المتوقع أن تؤدي تكاليف الصيانة والدعم بعد تنفيذ تكامل السجلات الصحية الإلكترونية إلى إعاقة نمو السوق بشكل أكبر.

- التحديات المتعلقة بتكامل البيانات

لقد تم إنشاء المعلومات المتعلقة بالمرضى من أقسام مختلفة وفي جميع نقاط العلاج داخل منظمة الرعاية الصحية، مما يجعلها صناعة كثيفة المعلومات وسجلات المرضى موثوقة، ومع ذلك، من الضروري تقديم معلومات موثوقة من خلال الجمع بين كميات هائلة من البيانات من أجل إنتاج سجلات شاملة وجديرة بالثقة للمرضى. نظرًا لاستخدام مجموعة متنوعة من المعدات الطبية وأدوات التشخيص في أنظمة الرعاية الصحية، فهناك حاجة متزايدة لربط كل هذه الأنظمة لمساعدة ممارسي الرعاية الصحية في الاستجابة بسرعة في نقاط تقديم الرعاية المختلفة.

على سبيل المثال،

- في أكتوبر 2016، وفقًا للتقرير المنشور في المؤتمر الدولي للابتكارات في العلوم والهندسة والتكنولوجيا (ICISET) لعام 2016، فقد ذكروا وحللوا مشاكل مختلفة لتكامل بيانات الرعاية الصحية في بنغلاديش لتطوير مستودع بيانات صحية على المستوى الوطني للمواطن واكتشاف المعرفة المخفية من مستودعات البيانات الصحية المختلفة يتطلب دمج البيانات الصحية من مصادر متنوعة على نطاق واسع.

تأثير COVID-19 على سوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة

كانت خدمات التصوير التشخيصي تستغرق وقتًا طويلاً ومعقدة بسبب الحاجة إلى ممارسات صارمة لمكافحة العدوى والوقاية منها تم تطويرها لاحتواء خطر انتقال العدوى وحماية العاملين في مجال الرعاية الصحية. وبالتالي، فإن قرار تصوير المرضى المشتبه بهم أو المرضى المصابين بـ COVID-19 يعتمد على تأثيرهم على تحسين حالة المريض. زاد استخدام تكنولوجيا المعلومات الصحية (HIT) أثناء جائحة مرض فيروس كورونا 2019 (COVID-19) بسرعة. أثناء الوباء، تم استخدام HIT لتوفير خدمات الرعاية الصحية عن بعد، والتثقيف بشأن مرض فيروس كورونا 2 المسبب لمتلازمة الجهاز التنفسي الحادة الوخيمة، والتحديثات حول علم الأوبئة والعلاجات، ومؤخرًا، الوصول إلى أنظمة الجدولة للقاحات COVID-19.

التطورات الأخيرة

- في أغسطس 2022، أعلنت شركة Oracle عن توفر اتصالات مباشرة سريعة مع البنية التحتية لسحابة Oracle (OCI) التي تساعد المؤسسات الأعضاء في Internet2 على الانتقال إلى السحابة. من خلال اتصال شبكة مخصص لـ Internet2 Cloud Connect، يمكن للمؤسسات الاستفادة من اتصالات Internet2 الحالية لتوسيع مركز البيانات الخاص بها إلى OCI في غضون أيام دون رسوم إضافية من Internet2 لما يصل إلى 5 جيجابت في الثانية. وهذا يجعل من السهل على المؤسسات الوصول إلى موارد السحابة واستخدامها لدعم البحث والتعاون والمؤسسة الأكاديمية دون استثمارات جديدة كبيرة.

- في يونيو 2022، أعلنت شركة Epic Systems Corporation عن خطتها للانضمام إلى إطار عمل جديد لتبادل المعلومات الصحية لتحسين قابلية التشغيل البيني للبيانات الصحية في جميع أنحاء البلاد. لقد جمع إطار عمل التبادل الموثوق والاتفاقية المشتركة (TEFCA) شبكات المعلومات معًا للمساعدة في ضمان استفادة جميع الأشخاص من السجلات الصحية الكاملة والطولية أينما تلقوا الرعاية. وقد ساعد هذا الشركة على توسيع أعمالها.

نطاق سوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة

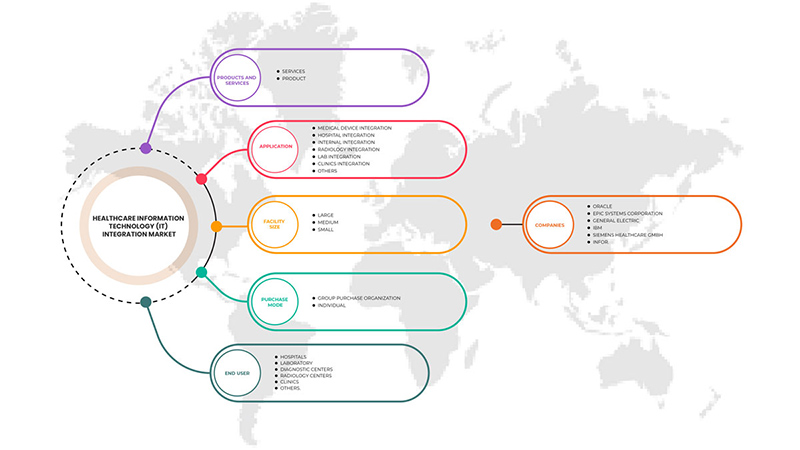

يتم تقسيم سوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة إلى خمسة قطاعات بارزة بناءً على المنتج والخدمات والتطبيق وحجم المنشأة وطريقة الشراء والمستخدم النهائي. سيساعدك النمو بين هذه القطاعات على تحليل قطاعات النمو الضئيلة في الصناعات وتزويد المستخدمين بنظرة عامة قيمة على السوق ورؤى السوق لمساعدتهم على اتخاذ قرارات استراتيجية لتحديد تطبيقات السوق الأساسية.

المنتجات والخدمات

- خدمات

- منتج

بناءً على المنتج والخدمات، يتم تقسيم السوق إلى خدمات ومنتج.

طلب

- تكامل الأجهزة الطبية

- التكامل الداخلي

- تكامل المستشفى

- تكامل المختبر

- تكامل العيادات

- تكامل الأشعة

- تطبيقات أخرى

بناءً على التطبيق، يتم تقسيم السوق إلى تكامل الأجهزة الطبية، والتكامل الداخلي، وتكامل المستشفيات ، وتكامل المختبرات، وتكامل العيادات ، وتكامل الأشعة وغيرها من التطبيقات.

حجم المنشأة

- كبير

- واسطة

- صغير

بناءً على حجم المنشأة، يتم تقسيم السوق إلى كبيرة ومتوسطة وصغيرة.

وضع الشراء

- منظمة الشراء الجماعي

- فردي

بناءً على نمط الشراء، يتم تقسيم السوق إلى منظمة شراء جماعية وفردية.

المستخدم النهائي

- المستشفيات

- معمل

- مراكز التشخيص

- مراكز الأشعة

- العيادات

- آحرون

بناءً على المستخدم النهائي، يتم تقسيم السوق إلى المستشفيات والمختبرات ومراكز التشخيص ومراكز الأشعة والعيادات وغيرها.

تحليل/رؤى إقليمية لسوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة

يتم تحليل سوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة، ويتم توفير رؤى حجم السوق والاتجاهات حسب المناطق والمنتج والخدمات والتطبيق وحجم المنشأة وطريقة الشراء والمستخدم النهائي كما هو مذكور أعلاه.

الدولة التي يغطيها تقرير السوق هذا هي الولايات المتحدة

ومن المتوقع أن تهيمن الولايات المتحدة على السوق بفضل أحدث تقنياتها المتقدمة واختراعاتها في تكامل تكنولوجيا المعلومات الخاصة بالرعاية الصحية.

كما يوفر قسم الدولة في التقرير عوامل فردية مؤثرة على السوق والتغييرات في اللوائح في السوق محليًا والتي تؤثر على الاتجاهات الحالية والمستقبلية للسوق. تعد نقاط البيانات مثل المبيعات الجديدة ومبيعات الاستبدال والتركيبة السكانية للدولة وعلم الأوبئة المرضية ورسوم الاستيراد والتصدير من بين المؤشرات الرئيسية المستخدمة للتنبؤ بسيناريو السوق للدول الفردية. كما يتم النظر في وجود وتوافر العلامات التجارية في أمريكا الشمالية والتحديات التي تواجهها بسبب المنافسة الكبيرة أو النادرة من العلامات التجارية المحلية والمحلية التي تؤثر على قنوات المبيعات أثناء تقديم تحليل توقعات لبيانات الدولة.

تحليل المشهد التنافسي وحصة سوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة

يوفر المشهد التنافسي لسوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة تفاصيل عن المنافس. تتضمن التفاصيل نظرة عامة على الشركة، والبيانات المالية للشركة، والإيرادات المتولدة، وإمكانات السوق، والاستثمار في البحث والتطوير، ومبادرات السوق الجديدة، والحضور في أمريكا الشمالية، ومواقع الإنتاج والمرافق، والقدرات الإنتاجية، ونقاط القوة والضعف للشركة، وإطلاق المنتج، وعرض المنتج، ونطاقه، وهيمنة التطبيق. ترتبط نقاط البيانات المذكورة أعلاه فقط بتركيز الشركات فيما يتعلق بسوق تكامل تكنولوجيا المعلومات للرعاية الصحية في الولايات المتحدة.

بعض اللاعبين الرئيسيين العاملين في السوق هم Lyniate و Redox و Inc. و carepoint health و Nextgen Healthcare Inc. و Interfaceware و Inc. و Koninklijke Philips و Oracle و AVI-SPL و INC. و Allscripts Healthcare solutions و Inc و Epic systems corporation و Qualcomm life Inc. و Capsule technologies Inc. و Orion health و Quality syetems و Inc. و Cerner corporation و Intersystems corporation و intersystem corporation و Infor Inc. و GE Healthcare و MCKESSON Corporation و Meditech وغيرها.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 MULTIVARIATE MODELLING

2.7 MARKET APPLICATION COVERAGE GRID

2.8 PRODUCT AND SERVICES LIFELINE CURVE

2.9 DBMR MARKET POSITION GRID

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHT

4.1 POTENTIAL HEALTHCARE IT TECHNOLOGIES

4.1.1 ELECTRONIC HEALTH RECORDS (EHRS)

4.1.2 ELECTRONIC MEDICAL RECORDS (EMRS)

4.1.3 ARTIFICIAL INTELLIGENCE (AI)

4.1.4 TELEMEDICINE

5 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET SHARE ANALYSIS-

6 REGULATIONS

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 RAPID ADOPTION OF ELECTRONIC HEALTH RECORDS AND OTHER HEALTHCARE IT SOLUTIONS

7.1.2 GROWING DEMAND FOR TELEHEALTH SERVICES AND REMOTE PATIENT MONITORING SOLUTIONS

7.1.3 GROWING REQUIREMENT OF TELEHEALTH SERVICES ACROSS HEALTHCARE SECTOR

7.2 RESTRAINTS

7.2.1 ISSUES ASSOCIATED WITH INTEROPERABILITY

7.2.2 HIGH COSTS ASSOCIATED WITH INTEGRATED IT SOLUTIONS

7.3 OPPORTUNITIES

7.3.1 EARLY MEDICAL DECISIONS AND CLINICAL DECISION SUPPORT

7.3.2 DATA UNIFORMITY AND STANDARDIZED DATA EXCHANGE

7.3.3 INCREASING AWARENESS AMONG PEOPLE

7.4 CHALLENGES

7.4.1 DATA INTEGRATION RELATED CHALLENGES

7.4.2 RISING HEALTHCARE FRAUDS

8 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT AND SERVICES

8.1 OVERVIEW

8.2 SERVICES

8.2.1 SUPPORT & MAINTENANCE

8.2.2 IMPLEMENTATION & INTEGRATION

8.2.3 TRAINING & EDUCATION

8.2.4 CONSULTING

8.3 PRODUCT

8.3.1 INTERFACE/INTEGRATION ENGINES

8.3.1.1 Group Purchase Organization

8.3.1.2 Individual

8.3.2 MEDICAL DEVICE INTEGRATION SOFTWARE

8.3.2.1 Group Purchase Organization

8.3.2.2 Individual

8.3.3 MEDIA INTEGRATION SOLUTIONS

8.3.3.1 Group Purchase Organization

8.3.3.2 Individual

8.3.4 OTHER INTEGRATION TOOLS

9 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY APPLICATION

9.1 OVERVIEW

9.2 MEDICAL DEVICE INTEGRATION

9.3 HOSPITAL INTEGRATION

9.4 INTERNAL INTEGRATION

9.5 RADIOLOGY INTEGRATION

9.6 LAB INTEGRATION

9.7 CLINICS INTEGRATION

9.8 OTHERS

10 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY FACILITY SIZE

10.1 OVERVIEW

10.2 LARGE

10.3 MEDIUM

10.4 SMALL

11 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PURCHASE MODE

11.1 OVERVIEW

11.2 GROUP PURCHASE ORGANIZATION

11.3 INDIVIDUAL

12 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY END USER

12.1 OVERVIEW

12.2 HOSPITAL

12.3 DIAGNOSTIC CENTERS

12.4 RADIOLOGY CENTERS

12.5 LABORATORY

12.6 CLINICS

12.7 OTHERS

13 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: COMPANY LANDSCAPE

13.1 COMPANY SHARE ANALYSIS: U.S.

14 SWOT ANALYSIS

15 COMPANY PROFILE

15.1 ORACLE (BOTH PROVIDERS)

15.1.1 COMPANY SNAPSHOT

15.1.2 REVENUE ANALYSIS

15.1.3 PRODUCT PORTFOLIO

15.1.4 RECENT DEVELOPMENTS

15.2 EPIC SYSTEMS CORPORATION (EMR PROVIDERS)

15.2.1 COMPANY SNAPSHOT

15.2.2 PRODUCT PORTFOLIO

15.2.3 RECENT DEVELOPMENT

15.3 GENERAL ELECTRIC

15.3.1 COMPANY SNAPSHOT

15.3.2 REVENUE ANALYSIS

15.3.3 PRODUCT PORTFOLIO

15.3.4 RECENT DEVELOPMENTS

15.4 IBM (INTEGRATION PROVIDERS)

15.4.1 COMPANY SNAPSHOT

15.4.2 REVENUE ANALYSIS

15.4.3 PRODUCT PORTFOLIO

15.4.4 RECENT DEVELOPMENTS

15.5 SIEMENS HEALTHCARE GMBH (INTEGRATION PROVIDERS)

15.5.1 COMPANY SNAPSHOT

15.5.2 REVENUE ANALYSIS

15.5.3 PRODUCT PORTFOLIO

15.5.4 RECENT DEVELOPMENTS

15.6 ALLSCRIPTS HEALTHCARE, LLC AND/OR ITS AFFILIATES. (EMR PROVIDERS)

15.6.1 COMPANY SNAPSHOT

15.6.2 REVENUE ANALYSIS

15.6.3 PRODUCT PORTFOLIO

15.6.4 RECENT DEVELOPMENTS

15.7 COGNIZANT (INTEGRATION PROVIDERS)

15.7.1 COMPANY SNAPSHOT

15.7.2 REVENUE ANALYSIS

15.7.3 PRODUCT PORTFOLIO

15.7.4 RECENT DEVELOPMENTS

1.5 INFOR.

15.7.5 COMPANY SNAPSHOT

15.7.6 PRODUCT PORTFOLIO

15.7.7 RECENT DEVELOPMENT

15.8 INTERSYSTEM CORPORATION (INTRGRATION PROVIDERS)

15.8.1 COMPANY SNAPSHOT

15.8.2 PRDUCT PORTFOLIO

15.8.3 RECENT DEVELOPMENTS

15.9 INTERFACEWARE INC.(INTEGRATION PROVIDERS)

15.9.1 COMPANY SNAPSHOT

15.9.2 PRODUCT PORTFOLIO

15.9.3 RECENT DEVELOPMENTS

15.1 KONNKLIJKE PHILIPS N.V. (2021) (BOTH PROVIDERS)

15.10.1 COMPANY SNAPSHOT

15.10.2 REVENUE ANALYSIS

15.10.3 PRODUCT PORTFOLIO

15.10.4 RECENT DEVELOPMENTS

15.11 LYNIATE

15.11.1 COMPANY SNAPSHOT

15.11.2 PRODUCT PORTFOLIO

15.11.3 RECENT DEVELOPMENTS

15.12 MASIMO (2021) (INTEGRATION PROVIDERS)

15.12.1 COMPANY SNAPSHOT

15.12.2 REVENUE ANALYSIS

15.12.3 PRODUCT PORTFOLIO

15.12.4 RECENT DEVELOPMENT

15.13 MDI SOLUTIONS (INTGRATION PROVIDERS)

15.13.1 COMPANY SNAPSHOT

15.13.2 PRODUCT PORTFOLIO

15.13.3 RECENT DEVELOPMENTS

15.14 MEDICAL INFORMATION TECHNOLOGY, INC. (EMR PROVIDERS)

15.14.1 COMPANY SNAPSHOT

15.14.2 PRODUCT PORTFOLIO

15.14.3 RECENT DEVELOPMENTS

15.15 NXGN MANAGEMENT, LLC (EMR PROVIDERS)

15.15.1 COMPANY SNAPSHOT

15.15.2 REVENUE ANALYSIS

15.15.3 PRODUCT PORTFOLIO

15.15.4 RECENT DEVELOPMENTS

15.16 ORION HEALTH GROUP (INTEGRATION PROVIDERS)

15.16.1 COMPANY SNAPSHOT

15.16.2 REVENUE ANALYSIS

1.11.3. PRODUCT PORTFOLIO 115

15.16.3 RECENT DEVELOPMENTS

15.17 REDOX, INC.(INTEGRATION PROVIDERS)

15.17.1 COMPANY SNAPSHOT

15.17.2 PRODUCT PORTFOLIO

15.17.3 RECENT DEVELOPMENTS

15.18 SUMMIT HEALTHCARE SERVICES, INC.(INTEGRATION PROVIDERS)

15.18.1 COMPANY SNAPSHOT

15.18.2 PRODUCT PORTFOLIO

15.18.3 RECENT DEVELOPMENTS

15.19 QVERA (INTEGRATION PROVIDERS)

15.19.1 COMPANY SNAPSHOT

15.19.2 PRODUCT PORTFOLIO

15.19.3 RECENT DEVELOPMENTS

16 QUESTIONNAIRE

17 RELATED REPORTS

List of Table

TABLE 1 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 2 U.S. SERVICES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 3 U.S. PRODUCT IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 4 U.S. INTERFACE/INTEGRATION ENGINES IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 5 U.S. MEDICAL DEVICE INTEGRATION SOFTWARE IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 6 U.S. MEDIA INTEGRATION SOLUTIONS IN HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PRODUCT & SERVICES, 2020-2029 (USD MILLION)

TABLE 7 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 8 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY FACILITY SIZE, 2020-2029 (USD MILLION)

TABLE 9 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY PURCHASE MODE, 2020-2029 (USD MILLION)

TABLE 10 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET, BY END USER, 2020-2029 (USD MILLION)

List of Figure

FIGURE 1 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: SEGMENTATION

FIGURE 2 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: DATA TRIANGULATION

FIGURE 3 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: DROC ANALYSIS

FIGURE 4 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: REGIONAL VS COUNTRY MARKET ANALYSIS

FIGURE 5 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: MARKET APPLICATION COVERAGE GRID

FIGURE 8 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: DBMR MARKET POSITION GRID

FIGURE 9 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: SEGMENTATION

FIGURE 10 GROWING DEMAND FOR HEALTHCARE IT SOLUTIONS, TELEHEALTH SERVICES, AND REMOTE PATIENT MONITORING SOLUTIONS ARE EXPECTED TO DRIVE THE U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 11 SERVICES SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET FROM 2022 TO 2029

FIGURE 12 DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES OF U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET

FIGURE 13 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PRODUCT AND SERVICES, 2021

FIGURE 14 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PRODUCT AND SERVICES, 2022-2029 (USD MILLION)

FIGURE 15 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PRODUCT AND SERVICES, CAGR (2022-2029)

FIGURE 16 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PRODUCT AND SERVICES, LIFELINE CURVE

FIGURE 17 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY APPLICATION, 2021

FIGURE 18 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY APPLICATION, 2022-2029 (USD MILLION)

FIGURE 19 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY APPLICATION, CAGR (2022-2029)

FIGURE 20 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY APPLICATION, LIFELINE CURVE

FIGURE 21 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY FACILITY SIZE, 2021

FIGURE 22 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY FACILITY SIZE, 2022-2029 (USD MILLION)

FIGURE 23 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY FACILITY SIZE, CAGR (2022-2029)

FIGURE 24 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY FACILITY SIZE, LIFELINE CURVE

FIGURE 25 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PURCHASE MODE, 2021

FIGURE 26 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PURCHASE MODE, 2022-2029 (USD MILLION)

FIGURE 27 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PURCHASE MODE, CAGR (2022-2029)

FIGURE 28 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY PURCHASE MODE, LIFELINE CURVE

FIGURE 29 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY END USER, 2021

FIGURE 30 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 31 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY END USER, CAGR (2022-2029)

FIGURE 32 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: BY END USER, LIFELINE CURVE

FIGURE 33 U.S. HEALTHCARE INFORMATION TECHNOLOGY (IT) INTEGRATION MARKET: COMPANY SHARE 2021 (%)

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.