Global Geomembranes Market

Market Size in USD Billion

USD

2.80 Billion

USD

4.58 Billion

2024

2032

USD

2.80 Billion

USD

4.58 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.80 Billion | |

| USD 4.58 Billion | |

| % | |

|

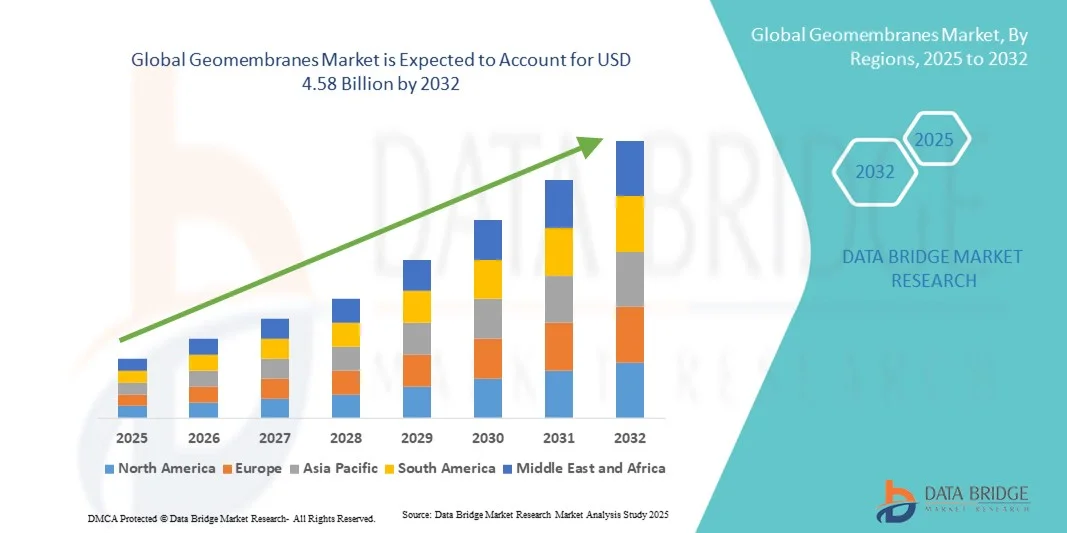

Geomembranes Market Size

- The global geomembranes market size was valued at USD 2.80 billion in 2024 and is expected to reach USD 4.58 billion by 2032, at a CAGR of 6.35% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced materials and technological advancements in geosynthetic solutions, leading to enhanced durability and environmental protection in construction, waste management, and water containment applications

- Furthermore, rising demand from infrastructure, mining, and environmental sectors for efficient, cost-effective, and sustainable solutions is positioning geomembranes as a critical component in modern engineering projects. These converging factors are accelerating the uptake of geomembrane solutions, thereby significantly boosting the industry's growth

Geomembranes Market Analysis

- Geomembranes, offering high-performance synthetic liners for environmental, industrial, and civil applications, are increasingly vital components in modern infrastructure projects due to their durability, chemical resistance, and cost-efficiency

- The escalating demand for geomembranes is primarily fueled by rapid urbanization, growing industrial activities, stringent environmental regulations, and a rising preference for sustainable water management and containment solutions

- North America dominated the geomembranes market with the largest revenue share of 44.5% in 2024, driven by advanced infrastructure development, strong industrial base, and the presence of key industry players, with the U.S. witnessing substantial adoption in construction, mining, and environmental protection projects

- Asia-Pacific is expected to be the fastest-growing region in the Geomembranes market during the forecast period, owing to rapid urbanization, growing industrial activities, and rising investments in water management and environmental projects in countries such as China, India, and Japan

- The Blown Film segment dominated the geomembranes market with a revenue share of 46.3% in 2024, owing to its superior uniformity, thickness consistency, and mechanical properties. Blown film geomembranes are widely used in large-scale landfill, mining, and water containment applications, as they offer excellent strength-to-weight ratios

Report Scope and Geomembranes Market Segmentation

|

Attributes |

Geomembranes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Geomembranes Market Trends

Enhanced Adoption Driven by Sustainability and Infrastructure Needs

- A significant and accelerating trend in the global geomembranes market is the increasing focus on sustainable construction, water management, and environmental protection. Geomembranes are being widely adopted in applications such as landfill liners, water reservoirs, mining operations, and wastewater treatment due to their durability, impermeability, and cost-effectiveness

- For instance, high-density polyethylene (HDPE) geomembranes are increasingly used in municipal landfill projects to prevent soil and groundwater contamination, while PVC and EPDM geomembranes are gaining popularity in water reservoirs and irrigation systems

- The integration of advanced manufacturing techniques and enhanced material formulations is improving the mechanical strength, chemical resistance, and UV stability of geomembranes, allowing their use in increasingly challenging environments

- Development of multilayer and composite geomembranes is enabling superior performance for complex applications, such as industrial waste containment and chemical storage, enhancing their reliability and lifecycle performance

- Growing environmental regulations and global initiatives promoting water conservation and waste management are further accelerating the adoption of geomembranes in both developed and emerging markets

- The trend towards sustainable and resilient infrastructure projects is creating new opportunities for geomembranes in urban development, industrial facilities, and renewable energy projects

- Manufacturers are increasingly focusing on innovation, quality certifications, and product customization to meet specific site requirements, boosting confidence among engineers, contractors, and project owners

Geomembranes Market Dynamics

Driver

Rising Infrastructure Development and Environmental Protection Initiatives

- The increasing demand for sustainable infrastructure, efficient water management systems, and safe waste containment is a significant driver for the growth of the geomembranes market

- For instance, in 2024, several large-scale municipal water storage and treatment projects in North America and Europe adopted HDPE and composite geomembranes to enhance environmental safety and reduce leakage risks. Such adoption by key projects is expected to propel industry growth during the forecast period

- Geographical expansion of industrial, mining, and agricultural operations is driving the need for reliable and long-lasting containment solutions. Geomembranes offer superior chemical resistance, low permeability, and mechanical strength compared to traditional liners, making them a preferred choice

- Government regulations enforcing environmental protection and contamination control in landfills, mining sites, and water bodies are encouraging the widespread use of geomembranes

- Infrastructure projects in developing regions are increasingly using geomembranes due to their cost-effectiveness, ease of installation, and adaptability to diverse climatic conditions

- Technological innovations, such as the development of composite and reinforced geomembranes, are enabling broader application areas, further contributing to market growth

- Rising awareness among project developers and environmental agencies regarding sustainability and regulatory compliance continues to propel geomembrane adoption globally

Restraint/Challenge

High Material Costs, Installation Complexity, and Technical Limitations

- The relatively high cost of advanced geomembranes, particularly multilayer or reinforced variants, can be a barrier for small-scale or budget-constrained projects

- Installation challenges, including the need for skilled labor, precise site preparation, and specialized welding techniques, can increase project timelines and overall costs

- Inadequate awareness of proper geomembrane handling, storage, and installation procedures may lead to performance issues such as punctures, leaks, or premature degradation, affecting project reliability

- Environmental and climatic conditions, such as extreme temperatures, UV exposure, and chemical contact, can reduce geomembrane lifespan if not properly selected or maintained

- Competition from alternative containment solutions, such as clay liners or concrete linings, may limit market penetration in certain applications, especially where cost is a major constraint

- Ensuring consistent quality across manufacturers and regions remains a challenge, as variations in material properties can affect long-term performance

- Addressing these challenges requires better technical training, improved material standardization, cost-optimized manufacturing, and widespread awareness campaigns to highlight the benefits and proper usage of geomembranes

- Strategic partnerships between manufacturers, contractors, and regulatory bodies will be crucial for sustained market growth

Geomembranes Market Scope

The market is segmented on the basis of raw material, manufacturing process, and application.

- By Raw Material

On the basis of raw material, the geomembranes market is segmented into High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), Polyvinyl Chloride (PVC), Ethylene Propylene Diene Monomer (EPDM), Polypropylene (PP), and Others. The HDPE segment dominated the market with the largest revenue share of 44.7% in 2024, driven by its exceptional chemical resistance, tensile strength, and long service life. HDPE geomembranes are widely used in water management, mining, and waste containment projects due to their durability and cost-effectiveness. Growing government initiatives for environmental protection, along with stringent regulations for landfill liners and water reservoirs, have further boosted demand. HDPE’s compatibility with multiple welding techniques and adaptability to harsh environmental conditions make it a preferred choice among contractors and engineering firms. Additionally, increasing awareness about sustainable construction practices supports the adoption of HDPE geomembranes across developed and emerging regions.

The EPDM segment is expected to witness the fastest CAGR of 20.5% from 2025 to 2032. EPDM offers excellent flexibility, UV resistance, and temperature tolerance, making it ideal for pond liners, reservoir covers, and green infrastructure projects. Its growing adoption in environmentally sensitive applications, coupled with rising infrastructure investments in Asia-Pacific and Latin America, is driving market growth. EPDM’s ease of installation, long-term reliability, and ability to meet strict environmental compliance standards make it increasingly attractive for municipalities and private developers. Rising demand for renewable energy projects and water conservation solutions further contributes to its rapid uptake.

- By Manufacturing Process

On the basis of manufacturing process, the geomembranes market is segmented into Blown Film, Calendering, and Others. The Blown Film segment dominated the market with a revenue share of 46.3% in 2024, owing to its superior uniformity, thickness consistency, and mechanical properties. Blown film geomembranes are widely used in large-scale landfill, mining, and water containment applications, as they offer excellent strength-to-weight ratios. The process allows for production of large sheets suitable for continuous lining, reducing seams and improving performance. Growing environmental regulations and infrastructure development projects in North America and Europe drive adoption. The versatility of blown film in accommodating HDPE, LDPE, and PP materials further strengthens its position as the preferred manufacturing method.

The Calendering segment is expected to witness the fastest CAGR of 19.8% from 2025 to 2032. Calendered geomembranes provide superior surface smoothness and uniform thickness, making them suitable for specialized applications such as chemical containment, tunnel lining, and waterproofing in critical industrial projects. The rising adoption of calendered geomembranes in emerging economies, due to increasing industrialization and mining projects, is fueling growth. Technological improvements in calendering machinery, enabling precise thickness control and large-scale production, further contribute to the segment’s rapid expansion.

- By Application

On the basis of application, the geomembranes market is segmented into Waste Management, Mining, Water Management, Tunnel Lining, and Others. The Waste Management segment dominated the market with a revenue share of 42.1% in 2024, driven by the increasing construction of sanitary landfills and regulatory mandates for environmental protection. Geomembranes are extensively used for lining municipal and industrial landfills to prevent leachate leakage and contamination of soil and groundwater. The growing focus on sustainable waste management practices and rising urbanization further support adoption. Integration of geomembranes in waste-to-energy and recycling projects is also contributing to market growth.

The Water Management segment is expected to witness the fastest CAGR of 21.4% from 2025 to 2032. Rising demand for irrigation systems, reservoirs, and dams, especially in water-scarce regions of Asia-Pacific and Middle East, is fueling growth. Geomembranes offer superior impermeability, chemical resistance, and flexibility, making them ideal for lining canals, ponds, and wastewater treatment facilities. Government initiatives promoting efficient water resource management, along with climate change mitigation efforts, further accelerate market adoption. Technological advancements in geomembrane materials, such as reinforced and composite liners, support increased deployment in large-scale water management projects.

Geomembranes Market Regional Analysis

- North America dominated the geomembranes market with the largest revenue share of 44.5% in 2024, driven by advanced infrastructure development, strong industrial base, and the presence of key industry players

- The market witnessed substantial adoption of geomembranes in construction, mining, waste management, and environmental protection projects, supported by regulatory initiatives and large-scale industrial activities

- High-quality manufacturing capabilities and early adoption of advanced geomembrane solutions also contribute to the region’s market leadership

U.S. Geomembranes Market Insight

The U.S. geomembranes market captured the largest revenue share within North America in 2024, fueled by the widespread adoption of geomembranes in infrastructure projects, industrial facilities, water reservoirs, and landfill lining applications. Government initiatives promoting environmental safety and sustainable water management further accelerated the market growth. Additionally, partnerships between manufacturers and large-scale projects are expanding the deployment of high-performance geomembranes across multiple sectors.

Europe Geomembranes Market Insight

The Europe geomembranes market is projected to grow at a substantial CAGR throughout the forecast period, primarily driven by stringent environmental regulations, rising investments in waste containment, and increasing adoption in water and wastewater management projects. Countries such as France, Italy, and Spain are seeing strong demand in both public infrastructure and industrial applications. The region’s emphasis on sustainability and eco-friendly construction materials further supports geomembrane adoption.

U.K. Geomembranes Market Insight

The U.K. geomembranes market is expected to grow steadily during the forecast period, fueled by increasing infrastructure projects, urban development initiatives, and government regulations promoting environmental protection. The rising need for containment solutions in landfills, water treatment facilities, and industrial applications continues to drive market expansion.

Germany Geomembranes Market Insight

The Germany geomembranes market is expected to expand at a considerable CAGR during the forecast period, supported by strong industrial activities, advanced infrastructure, and an emphasis on sustainable development. Adoption is particularly high in wastewater management, industrial containment, and mining projects, where high-quality geomembranes offer long-term durability and environmental protection.

Asia-Pacific Geomembranes Market Insight

The Asia-Pacific geomembranes market is expected to grow at the fastest CAGR of 24% during the forecast period of 2025 to 2032, driven by rapid urbanization, growing industrial activities, and rising investments in water management, environmental protection, and infrastructure projects in countries such as China, India, and Japan. The region’s increasing focus on sustainable construction and large-scale industrial development is expanding the use of geomembranes.

Japan Geomembranes Market Insight

The Japan geomembranes market is gaining momentum due to the country’s industrial growth, urban expansion, and government-backed infrastructure initiatives. Increased focus on environmental protection, water conservation, and sustainable construction practices is driving demand for geomembranes across residential, commercial, and industrial projects.

China Geomembranes Market Insight

The China geomembranes market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, expanding industrial base, and rising investments in water management and environmental protection projects. Large-scale infrastructure projects, smart city initiatives, and growing environmental awareness are driving the adoption of geomembranes in municipal, industrial, and commercial applications.

Geomembranes Market Share

The Geomembranes industry is primarily led by well-established companies, including:

- GSE Holdings, Inc. (U.S.)

- Solmax International Inc. (Canada)

- AGRU America, Inc. (U.S)

- NAUE GmbH & Co. KG (Germany)

- Raven Industries, Inc. (U.S.)

- Juta a.s. (Czech Republic)

- Tensar International Corporation (U.K.)

- Propex Operating Company, LLC (U.S.)

- Seaman Corporation (U.S.)

- Cosella-Dörken (Germany)

- Fosroc International Limited (U.K.)

- Teknor Apex Company (U.S.)

- Layfield Group (Canada)

- Solmax Asia Pacific Pte Ltd (Singapore)

- Bostik SA (France)

- Tesa (Spain)

Latest Developments in Global Geomembranes Market

- In May 2024, Solmax Americas inaugurated a new geomembrane manufacturing line at its Houston facility, significantly enhancing its production capacity to cater to the growing demand for high-quality geomembranes across the Americas. This expansion reflects the company’s commitment to supporting large-scale infrastructure, mining, and water management projects while ensuring timely supply of reliable geomembrane solutions

- In March 2025, Plastatech Engineering Ltd. introduced a 40 mil non-reinforced UV-resistant geomembrane, engineered for superior durability and excellent lay-flat characteristics. This product is specifically designed for above-ground applications, offering enhanced resistance to environmental factors such as sunlight and temperature fluctuations, making it suitable for a wide range of industrial, municipal, and environmental projects

- In June 2025, the Flexible Geomembrane Institute (formerly the Fabricated Geomembrane Institute) underwent a rebranding to reflect its expanded mission, emphasizing factory fabrication and modular construction. This strategic shift aims to address the evolving needs of the geomembrane industry by providing updated guidance, technical expertise, and industry standards that support efficient design, installation, and quality assurance for modern geomembrane applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Geomembranes Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Geomembranes Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Geomembranes Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.