Global Diabetes Care Devices Market

Market Size in USD Billion

CAGR :

%

USD

34.28 Billion

USD

66.82 Billion

2024

2032

USD

34.28 Billion

USD

66.82 Billion

2024

2032

| 2025 –2032 | |

| USD 34.28 Billion | |

| USD 66.82 Billion | |

| % | |

|

Diabetes Care Devices Market Size

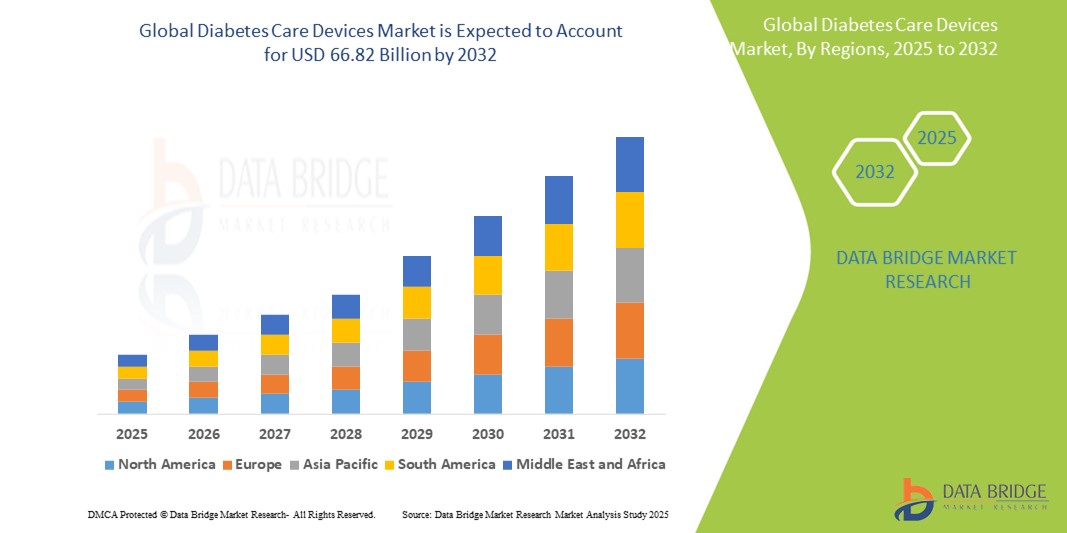

- The global diabetes care devices market size was valued at USD 34.28 billion in 2024 and is expected to reach USD 66.82 billion by 2032, at a CAGR of 8.70 % during the forecast period

- This growth is driven by factors such as the increasing prevalence of diabetes, rising health awareness, technological advancements in diabetes management devices, and the growing demand for home-based care solutions

Diabetes Care Devices Market Analysis

- Diabetes care devices are essential tools used for monitoring and managing diabetes, providing accurate blood glucose measurements, insulin delivery, and continuous monitoring for better disease management

- The demand for these devices is primarily driven by the increasing prevalence of diabetes, growing health awareness, and advancements in technology for more efficient and convenient diabetes management

- North America is expected to dominate the diabetes care devices market with a market share of 39.1%, due to advanced healthcare infrastructure, high adoption of innovative medical technologies, and the presence of major market players

- Asia-Pacific is expected to be the fastest growing region in the diabetes care devices market with a market share of 21.9%, during the forecast period due to rapid improvements in healthcare infrastructure, rising awareness about diabetes management, and an increase in the number of diabetes cases

- insulin delivery devices segment is expected to dominate the market with a market share of 56.3% due to the increasing prevalence of diabetes, particularly type 1 and type 2. The growing adoption of insulin pumps, pens, and syringes for efficient and precise insulin administration, along with technological advancements in these devices, contributes to their widespread use.

Report Scope and Diabetes Care Devices Market Segmentation

|

Attributes |

Diabetes Care Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Diabetes Care Devices Market Trends

“Technological Advancements in Diabetes Management Devices & Continuous Glucose Monitoring”

- One prominent trend in the evolution of diabetes care devices is the increasing integration of advanced technology in continuous glucose monitoring (CGM) systems and insulin delivery devices

- These innovations enhance diabetes management by providing real-time, accurate glucose level readings and enabling more precise insulin delivery, improving control over blood sugar levels

- For instance, modern CGM systems feature sensors that provide continuous, non-invasive glucose readings, enabling patients to make timely adjustments to their diet and insulin therapy. Insulin pumps are becoming more sophisticated with features such as automated insulin delivery based on real-time glucose readings

- These advancements are revolutionizing diabetes care by offering greater convenience, reducing the need for frequent fingerstick tests, and helping patients maintain better glycemic control, ultimately improving their quality of life and health outcomes

Diabetes Care Devices Market Dynamics

Driver

“Increasing Prevalence of Diabetes and Growing Healthcare Access”

- The rising global prevalence of diabetes, driven by factors such as an aging population, unhealthy lifestyles, and increasing obesity rates, is significantly contributing to the increased demand for diabetes care devices

- As the number of individuals diagnosed with type 1 and type 2 diabetes continues to grow, the need for effective diabetes management tools, including blood glucose monitors, insulin delivery systems, and continuous glucose monitors (CGMs), is rising

- With improved healthcare access and growing awareness about diabetes management, more patients are seeking advanced devices to monitor their glucose levels and administer insulin more effectively

For instance,

- According to the International Diabetes Federation (IDF), the global prevalence of diabetes is expected to reach 10.9% of the adult population by 2045, which translates to nearly 700 million adults living with diabetes globally

- This growing demand for diabetes care devices is fueled by the need for better control of blood sugar levels, reducing complications, and enhancing patient quality of life, ultimately driving the market for advanced diabetes care solutions

Opportunity

“Integration of Artificial Intelligence and Data Analytics for Improved Diabetes Management”

- AI-powered diabetes care devices, particularly in continuous glucose monitoring (CGM) systems and insulin delivery devices, have the potential to revolutionize diabetes management by enhancing real-time data analysis and providing more personalized treatment plans for patients

- AI algorithms can analyze glucose trends, predict future glucose levels, and automatically adjust insulin delivery, helping patients maintain optimal blood sugar levels with minimal manual intervention

- In addition, AI-powered systems can assist in patient education and behavior tracking, offering insights into dietary habits, exercise, and medication adherence, further improving overall diabetes management

For instance,

- According to a report published by the American Diabetes Association in 2023, AI algorithms integrated with CGM systems can predict glucose fluctuations and alert patients to take corrective actions in advance, potentially reducing the risk of complications

- The integration of AI in diabetes care devices can lead to improved patient outcomes, enhanced quality of life, and better overall disease management by providing more accurate and timely information

Restraint/Challenge

“High Costs of Diabetes Care Devices Limiting Market Growth”

- The high cost of advanced diabetes care devices, such as continuous glucose monitors (CGMs) and insulin pumps, poses a significant challenge for widespread adoption, particularly in low-income and developing regions

- These devices, which are essential for effective diabetes management, can be prohibitively expensive, often ranging from hundreds to thousands of dollars per unit, along with ongoing costs for sensors and maintenance

- This financial barrier can prevent smaller clinics, healthcare providers, and patients from accessing or affording the latest diabetes management technologies, leading to reliance on traditional methods such as fingerstick glucose testing and standard insulin injections

For instance,

- According to a 2023 report by the International Diabetes Federation (IDF), the cost of CGM systems and insulin pumps remains a major hurdle in several low- and middle-income countries, where healthcare spending is limited

- Consequently, these cost constraints can contribute to disparities in diabetes care, limiting access to advanced technologies and hindering the market’s growth potential, especially in regions where diabetes prevalence is increasing rapidly

Diabetes Care Devices Market Scope

The market is segmented on the basis of product type, device type, delivery type and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Product Type |

|

|

By Device Type |

|

|

By Delivery Type |

|

|

By Distribution Channel |

|

In 2025, the insulin delivery devices is projected to dominate the market with a largest share in product type segment

The insulin delivery devices segment is expected to dominate the diabetes care devices market with the largest share of 56.3% in 2025 due to the increasing prevalence of diabetes, particularly type 1 and type 2. The growing adoption of insulin pumps, pens, and syringes for efficient and precise insulin administration, along with technological advancements in these devices, contributes to their widespread use. In addition, the convenience and improved patient compliance offered by modern insulin delivery systems are key factors driving growth in this segment.

The self-monitoring is expected to account for the largest share during the forecast period in device type market

In 2025, the self-monitoring segment is expected to dominate the market with the largest market share of 57.03% due to the increasing demand for regular glucose level monitoring, which is essential for diabetes management. Advancements in blood glucose meters and continuous glucose monitoring (CGM) devices offer greater accuracy, convenience, and ease of use for patients. The rise in awareness about the importance of self-monitoring for better control of diabetes and improved health outcomes further drives the segment's growth.

Diabetes Care Devices Market Regional Analysis

“North America Holds the Largest Share in the Diabetes Care Devices Market”

- North America dominates the diabetes care devices market with a market share of estimated 39.1%, driven, by advanced healthcare infrastructure, high adoption of innovative medical technologies, and the presence of major market players

- U.S. holds a market share of 90%, due to the increasing prevalence of diabetes, the widespread use of continuous glucose monitoring (CGM) systems, and insulin delivery devices, as well as advancements in diabetes management technologies

- The availability of robust healthcare insurance plans, government initiatives promoting diabetes awareness, and ongoing investments in research & development by leading medical device companies further strengthen the market

- In addition, the growing number of diabetes diagnoses and an aging population are contributing to the demand for efficient and accurate diabetes management solutions, driving growth in the region

“Asia-Pacific is Projected to Register the Highest CAGR in the Diabetes Care Devices Market”

- Asia-Pacific is expected to witness the highest growth rate in the diabetes care devices market with a market share of 21.9%, driven by rapid improvements in healthcare infrastructure, rising awareness about diabetes management, and an increase in the number of diabetes cases

- Countries such as China, India, and Japan are emerging as key markets due to the growing prevalence of diabetes, an aging population, and increasing healthcare access

- China is experiencing a rise in diabetes diagnoses, with a large number of patients transitioning from traditional methods to advanced devices such as CGM systems and insulin pumps

- India is projected to register the highest CAGR, driven by expanding healthcare infrastructure, increasing diabetes prevalence, and a rising demand for more effective and patient-friendly diabetes care solutions

Diabetes Care Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Abbott (U.S.)

- Dexcom, Inc. (U.S.)

- Medtronic (Ireland)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novo Nordisk A/S (Denmark)

- Johnson & Johnson Services, Inc. (U.S.)

- Tandem Diabetes Care, Inc. (U.S.)

- BD (U.S.)

- Insulet Corporation (U.S.)

- Lilly (U.S.)

- Sanofi (France)

- Hovione (Portugal)

- OMRON Healthcare (Japan)

- Senseonics (U.S.)

- Ascensia Diabetes Care Holdings AG (Switzerland)

- Zebra Medical Vision (Israel)

- Diabetes Care Group (Italy)

- BlueLoop (U.S.)

- Medline Industries, LP. (U.S.)

Latest Developments in Global Diabetes Care Devices Market

- In January 2025, Senseonics has received FDA approval for its Eversense 365, an implantable CGM system that lasts up to a year, doubling the lifespan of its predecessor.This device provides real-time glucose readings every five minutes

- In October 2024, Companies such as Novo Nordisk and Eli Lilly have introduced smart insulin pens, such as the NovoPen 6 and Lilly’s Tempo Pen. These devices offer Bluetooth connectivity and companion apps, allowing for automated insulin delivery based on real-time glucose levels. Some models are now integrated with CGMs, enhancing personalized diabetes management

- In July 2023, CharmHealth and Bioverge jointly invested in My Diabetes Tutor, a startup focused on improving the lives of individuals with diabetes

- In May 2023, Medtronic agreed to acquire EOFlow, a manufacturer of insulin devices. The integration of EOFlow with Medtronic's Meal Detection Technology algorithm and advanced continuous glucose monitor (CGM) is expected to enhance the company's ability to serve a broader range of people with diabetes

- In April 2023, Undbio announced its plan to invest USD 100 million in constructing a US-based insulin manufacturing plant. The South Korean company intends to build a new facility in West Virginia to manufacture insulin and distribute its products within the country

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.