Europe Radiotherapy Market

Market Size in USD Billion

CAGR :

%

USD

2.41 Billion

USD

4.89 Billion

2024

2032

USD

2.41 Billion

USD

4.89 Billion

2024

2032

| 2025 –2032 | |

| USD 2.41 Billion | |

| USD 4.89 Billion | |

| % | |

|

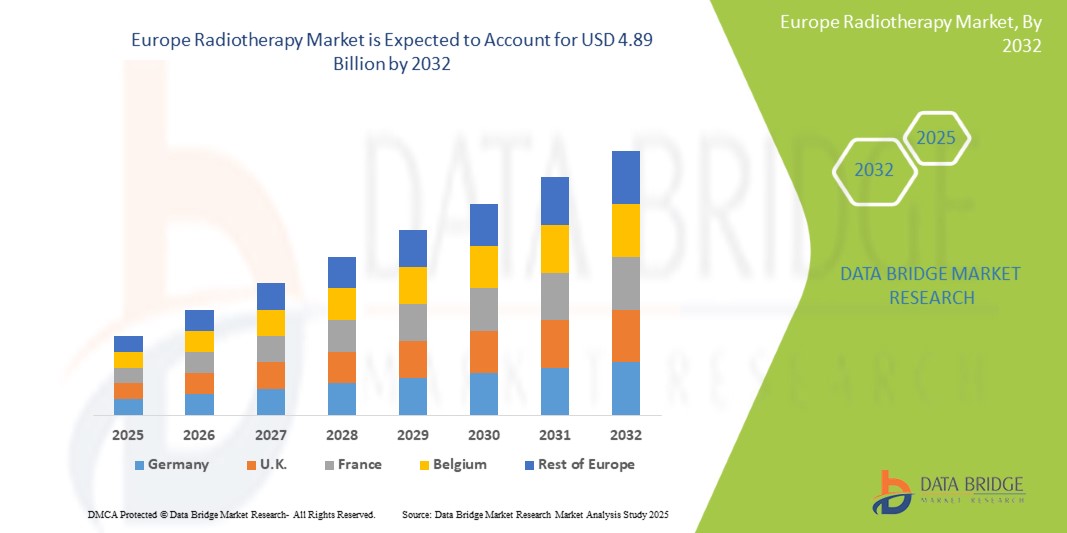

Europe Radiotherapy Market Size

- The Europe radiotherapy market size was valued at USD 2.41 billion in 2024 and is expected to reach USD 4.89 billion by 2032, at a CAGR of 9.7% during the forecast period

- The market growth is growing prevalence of cancer disease, novel technology in radiotherapy for cancer treatment and increasing adoption of radiotherapy devices and procedures

- Furthermore, the market is expected to increasing healthcare expenditure for cancer treatment, growing government initiatives toward cancer treatment and rising patients’ awareness towards cancer treatment

Europe Radiotherapy Market Analysis

- The Europe rise in cancer prevalence, increasing adoption of advanced radiotherapy techniques such as intensity-modulated radiotherapy (IMRT), stereotactic body radiotherapy (SBRT), and proton therapy, along with technological advancements in imaging and treatment planning systems, are key driving factors expected to propel the growth of the Europe radiotherapy market.

- Key factors such as rising demand for non-invasive and targeted cancer treatment solutions, growing investments in oncology-focused R&D, continuous innovation in radiotherapy equipment, and supportive government policies and funding for cancer care infrastructure are driving the growth of the Europe radiotherapy market.

- Germany dominated Europe radiotherapy market with the market share of 28.24% in 2024. and is expected to grow with the fastest CAGR of 10.5% in the forecast period of 2025 to 2032 due to growing prevalence of cancer disease, novel technology in radiotherapy for cancer treatment and increasing adoption of radiotherapy devices and procedures.

- The external beam radiotherapy segment dominated the market with a 62.47%market share in 2024, growing with the CAGR of 10.0% in the forecast period of 2025 to 2032. driven growing prevalence of cancer disease, novel technology in radiotherapy for cancer treatment and increasing adoption of radiotherapy devices and procedures.

Report Scope and Europe Radiotherapy Market Segmentation

|

Attributes |

Europe Radiotherapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Radiotherapy Market Trends

“Rising Demand for Advanced, Non-Invasive, And Precision-Based Cancer Treatment Solutions Across Healthcare Systems”

- Demand for advanced, non-invasive, and precision-based cancer treatment solutions is growing rapidly—driven by increasing cancer prevalence, rising patient awareness, and a shift toward personalized medicine across healthcare systems. Radiotherapy technologies address these demands by offering targeted, effective treatment options that minimize side effects and improve patient outcomes

- As healthcare providers aim to reduce treatment-related complications and enhance quality of care, there is a growing shift toward integrating advanced radiotherapy techniques such as image-guided radiotherapy (IGRT), intensity-modulated radiotherapy (IMRT), and proton therapy. This transition is crucial for meeting stringent regulatory standards, improving treatment efficacy, and supporting the Europe move toward value-based care

- Major industry players such as Siemens Healthineers, Elekta, Varian (a Siemens company), and Accuray are significantly increasing their R&D efforts to develop cutting-edge radiotherapy equipment and software that offer higher precision, automation, and integration with artificial intelligence, further driving innovation and market growth

- Advancements in imaging, treatment planning, and delivery technologies—such as adaptive radiotherapy, stereotactic radiosurgery (SRS), and proton beam therapy—are enhancing treatment accuracy, patient safety, and operational efficiency. These innovations are enabling broader adoption across hospitals and specialty centers and supporting the expansion of the Europe radiotherapy market

Europe Radiotherapy Market Dynamics

“Growing Prevalence of Cancer Disease”

- The rising Europe demand for advanced, precise, and patient-friendly cancer treatment solutions—driven by increasing cancer prevalence, growing patient awareness, and the shift toward personalized, less invasive therapies—is putting pressure on healthcare providers and manufacturers to innovate and upgrade radiotherapy technologies across hospitals, specialty clinics, and cancer centers. To meet this demand, companies are accelerating investments in next-generation radiotherapy equipment, software, and treatment planning systems to deliver higher accuracy, improved patient outcomes, and streamlined workflows at scale. These advancements are building smarter, more efficient oncology care ecosystems, much like how precision medicine is reshaping healthcare delivery

- For instance, in early 2025, researchers from leading oncology institutes highlighted the growing prominence of proton therapy and adaptive radiotherapy as transformative approaches in cancer treatment. Their studies emphasize the benefits of these cutting-edge technologies in minimizing radiation exposure to healthy tissues while enhancing tumor targeting, significantly improving patient quality of life. The report highlights the increasing importance of integrating advanced imaging and AI-driven treatment planning as vital components in the evolving landscape of cancer care, playing a critical role in enhancing radiotherapy efficacy as a personalized and integrative approach

- These investments are not only transforming radiotherapy capabilities but also enabling broader adoption of sophisticated treatment modalities across emerging markets and high-growth segments like pediatric oncology and rare cancers. Leading players such as Siemens, Elekta, Varian (Siemens), and Accuracy are investing heavily in innovative radiotherapy systems, AI-powered software, and patient-centric solutions to maintain competitive advantage and improve treatment performance across applications

- In addition, the ongoing commitment from governments, research institutions, and private industry toward improving cancer care infrastructure and advancing radiotherapy innovation is playing a pivotal role in shaping a more effective Europe oncology market. These initiatives are establishing advanced radiotherapy as a cornerstone of modern cancer treatment and a major growth driver in the transition toward safer, more precise, and patient-aligned therapies

Restraint/Challenge

“Lack of Skilled and Certified Professionals”

- The shortage of skilled and certified radiotherapy professionals remains one of the most significant restraints limiting the growth and broader adoption of advanced radiotherapy technologies worldwide. Radiotherapy treatment requires highly trained oncologists, medical physicists, dosimetrists, and radiation therapists to ensure precise treatment planning, safe delivery, and effective patient management—skills that are in short supply, especially in developing regions.

- Furthermore, the complexity of modern radiotherapy techniques—such as intensity-modulated radiotherapy (IMRT), stereotactic radiosurgery (SRS), and proton therapy—demands continuous professional training and certification to keep pace with technological advancements. The lack of standardized training programs and accreditation frameworks across many countries exacerbates the issue, often leading to suboptimal treatment outcomes and limiting the ability to fully leverage sophisticated radiotherapy equipment.

- For instance, in March 2025, a study by the International Atomic Energy Agency (IAEA) highlighted that many low- and middle-income countries face critical shortages of trained radiotherapy staff, which significantly delays the implementation of new treatment technologies and restricts patient access to quality care. The report emphasized the urgent need for international collaboration to develop scalable training programs and certification pathways tailored to resource-limited settings.

- Similarly, a 2024 survey conducted by the American Society for Radiation Oncology (ASTRO) revealed that despite growing investments in advanced radiotherapy systems across the United States, many centers struggle to recruit and retain qualified medical physicists and dosimetrists, directly impacting treatment efficiency and patient throughput.

- The shortage of skilled professionals coupled with the increasing complexity of radiotherapy techniques continues to act as a barrier to the widespread adoption and optimal utilization of radiotherapy services. While ongoing efforts in education, certification, and remote training are underway, addressing these workforce challenges remains critical to unlocking the full potential of the Europe radiotherapy market.

Europe Radiotherapy Market Scope

The market is segmented on the basis of product, application type, procedure type, usability, end user, and distribution channel

• By Product and Services

On the basis of product and services, the Europe radiotherapy market is segmented into services, products and software. In 2025, the services segment is expected to dominate the market with a market share of 55.95% growing with the highest CAGR of 9.9% in the forecast period of 2025 to 2032 driven by growing prevalence of cancer disease, novel technology in radiotherapy for cancer treatment and increasing adoption of radiotherapy devices and procedures.

- By Type

On the basis type, the Europe radiotherapy market is segmented into external-beam radiation therapy, internal radiation therapy, systemic radiotherapy/radiopharmaceuticals and others. In 2025, the External-Beam Radiation Therapy segment is expected to dominate the market with a market share of 65.11% growing with the highest CAGR of 9.9% in the forecast period of 2025 to 2032 driven by expected to increasing healthcare expenditure for cancer treatment, growing government initiatives toward cancer treatment and rising patients awareness towards cancer treatment.

- By Application

On the basis of application, the Europe radiotherapy market is segmented into breast cancer, lung cancer, prostate cancer, colorectal cancer, lymphoma, liver cancer, thyroid cancer, brain cancer, cervical cancer, spine cancer and others. In 2025, the breast cancer segment is expected to dominate the market with a market share of 21.94% growing with the highest CAGR of 10.9% in the forecast period of 2025 to 2032 driven by growing prevalence of cancer disease, novel technology in radiotherapy for cancer treatment and increasing adoption of radiotherapy devices and procedures.

- By End User

On the basis of end user, the Europe radiotherapy market is segmented into hospitals, radiation therapy centers, specialty clinics, academic & research institutes and others. In 2024, the hospitals segment dominated the market with a 63.55% market share and growing with the CAGR of 10.1% in the forecast period of 2025 to 2032 driven expected to increasing healthcare expenditure for cancer treatment, growing government initiatives toward cancer treatment and rising patients awareness towards cancer treatment

- By Distribution Channel

On the basis of distribution channel, the Europe radiotherapy market is segmented into direct tenders, third-party distributors and others. In 2024, the direct tenders segment dominated the market with a 81.41% market share and growing with the CAGR of 9.8.% in the forecast period of 2025 to 2032 driven by growing prevalence of cancer disease, novel technology in radiotherapy for cancer treatment and increasing adoption of radiotherapy devices and procedures.

Europe Radiotherapy Market Regional Analysis

- Germany in Europe radiotherapy market is expected to reach USD 1.47 Billion by 2032, from USD 0.68 Billion in 2024, growing at the CAGR of 10.5% in the forecast period of 2025 to 2032

- Germany allocates a significant portion of its GDP to healthcare, ensuring substantial funding for cutting-edge cancer treatment technologies, including advanced radiotherapy procedures. In contrast, emerging markets are increasing their healthcare spending due to growing cancer prevalence and rising awareness of modern treatment options. The availability of funding from both public and private sectors plays a crucial role in expanding access to radiotherapy services.

- In Europe, radiotherapy is widely available and integrated into standard oncology care. In contrast, emerging markets with developing healthcare infrastructure are experiencing rapid growth in access to radiotherapy services, driven by expanding hospital networks and increasing healthcare budgets. As healthcare systems become more centralized or privatized, increased investments in advanced radiotherapy equipment and software promote market growth and improve treatment accessibility.

France Radiotherapy Market Insight

The France radiotherapy market is expected to register the CAGR of 10.4% from 2025 to 2032, driven by expected to increasing healthcare expenditure for cancer treatment, growing government initiatives toward cancer treatment and rising patients’ awareness towards cancer treatment.

U.K Radiotherapy Market Insight

The U.K radiotherapy market is expected to register the CAGR of 10.1% from 2025 to 2032, driven by expected to increasing healthcare expenditure for cancer treatment, growing government initiatives toward cancer treatment and rising patients’ awareness towards cancer treatment.

Europe Radiotherapy Market Share

The Europe radiotherapy market is primarily led by well-established companies, including:

- Siemens Healthcare GmbH (Germany)

- Hitachi, Ltd. (Japan)

- General Electric Company (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Elekta (Sweden)

- ZEISS International (Germany)

- IBA Worldwide (Belgium)

- Canon Medical Systems Corporation (Japan)

- Accuray Incorporated (U.S.)

- Mevion Medical Systems (U.S.)

- Brainlab (Germany)

- BEBIG Medical (Germany)

- LinaTech, Inc. (China)

- United Imaging Healthcare Co., Ltd. (China)

- Eckert & Ziegler BEBIG (Germany)

- ViewRay Systems, Inc. (U.S.)

- Nordion (Canada) Inc. (Canada)

Latest Developments in Europe Radiotherapy Market

- In May 2024, Siemens Healthineers and Varian unveiled new advancements in radiation oncology at ESTRO 2024, including HyperSight imaging, ARIA CORE oncology management, and more accessible MRI for radiotherapy

- In September 2024, Ballad Health has entered a 10-year, USD 260 million collaboration with Varian, a Siemens Healthineers company, to transform cancer care in the Appalachian Highlands. This partnership will bring advanced oncology technology, including linear accelerators and digital management solutions, to six cancer centers, enhancing treatment precision and accessibility for rural communities

- In 2023, Hitachi expanded its Digital Systems & Services (DSS) segment through cloud, AI, and IoT solutions. This included further development of its Lumada platform and integration of EuropeLogic, an IT service company

- In May 2025, GE HealthCare is significantly expanding its radiation oncology portfolio at ESTRO 2025 with new AI-enabled solutions, including the MR Contour DL for efficient organ segmentation. They are also enhancing their Intelligent Radiation Therapy (iRT) software to integrate MR and AI-driven workflows, aiming for more precise and timely cancer treatment.

- In April 2024, GE HealthCare has finalized its acquisition of MIM Software, a Europe provider of medical imaging analysis and AI solutions. This strategic move bolsters GE HealthCare's portfolio, particularly in radiation oncology, by integrating MIM Software's advanced tools for image analysis, workflow automation, and AI-powered segmentation and contouring into its precision care strategy

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE EUROPE RADIOTHERAPY MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 MULTIVARIATE MODELLING

2.7 PRODUCT & SERVICES SEGMENT LIFELINE CURVE

2.8 MARKET END USER COVERAGE GRID

2.9 DBMR MARKET POSITION GRID

2.1 VENDOR SHARE ANALYSIS

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTLE ANALYSIS

4.2 PORTER'S FIVE FORCES MODEL

4.3 PRICING ANALYSIS

5 REGULATORY GUIDELINES FOR RADIOTHERAPY

5.1 U.S REGULATORY GUIDELINES FOR RADIOTHERAPY

5.2 EUROPE REGULATORY GUIDELINE FOR RADIOTHERAPY

5.3 INDIA REGULATORY GUIDELINE FOR RADIOTHERAPY

5.4 CLEARANCE OF THE UNIT BY AERB (TYPE APPROVED OR NOC-ISSUED EQUIPMENT)

5.5 CHINA REGULATORY GUIDELINE FOR RADIOTHERAPY

5.6 ELEMENTS OF RADIATION PROTECTION PROGRAM -

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 GROWING PREVALENCE OF CANCER DISEASE

6.1.2 NOVEL TECHNOLOGY IN RADIOTHERAPY FOR CANCER TREATMENT

6.1.3 INCREASING ADOPTION OF RADIOTHERAPY DEVICES AND PROCEDURES

6.1.4 RISING PREFERENCE FOR NON-SURGICAL PROCEDURES

6.2 RESTRAINTS

6.2.1 LACK OF SKILLED AND CERTIFIED PROFESSIONALS

6.2.2 HIGH COST OF TREATMENT AND RADIOTHERAPY PROCEDURE

6.3 OPPORTUNITIES

6.3.1 INCREASING HEALTHCARE EXPENDITURE FOR CANCER TREATMENT

6.3.2 GROWING GOVERNMENT INITIATIVES TOWARD CANCER TREATMENT

6.3.3 RISING PATIENTS AWARENESS TOWARDS CANCER TREATMENT

6.4 CHALLENGES

6.4.1 STRICT REGULATIONS AND STANDARDS FOR APPROVAL AND COMMERCIALIZATION OF RADIOTHERAPY PRODUCTS

6.4.2 RISK OF RADIATION EXPOSURE

7 EUROPE RADIOTHERAPY MARKET, BY PRODUCT & SERVICES

7.1 OVERVIEW

7.2 SERVICES

7.3 PRODUCT

7.4 SOFTWARE

8 EUROPE RADIOTHERAPY MARKET, BY TYPE

8.1 OVERVIEW

8.2 EXTERNAL-BEAM RADIATION THERAPY

8.3 INTERNAL RADIATION THERAPY

8.4 SYSTEMIC RADIOTHERAPY/ RADIOPHARMACEUTICALS

8.5 OTHERS

9 EUROPE RADIOTHERAPY MARKET, BY APPLICATION

9.1 OVERVIEW

9.2 BREAST CANCER

9.3 LUNG CANCER

9.4 PROSTATE CANCER

9.5 COLORECTAL CANCER

9.6 LYMPHOMA

9.7 LIVER CANCER

9.8 THYROID CANCER

9.9 BRAIN CANCER

9.1 CERVICAL CANCER

9.11 SPINE CANCER

9.12 OTHERS

10 EUROPE RADIOTHERAPY MARKET, BY END USER

10.1 OVERVIEW

10.2 HOSPITALS

10.3 RADIATION THERAPY CENTERS

10.4 SPECIALTY CLINICS

10.5 OTHERS

11 EUROPE RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL

11.1 OVERVIEW

11.2 DIRECT TENDERS

11.3 THIRD PARTY DISTRIBUTORS

11.4 OTHERS

12 EUROPE RADIOTHERAPY MARKET, BY REGION

12.1 EUROPE

12.1.1 GERMANY

12.1.2 FRANCE

12.1.3 U.K.

12.1.4 ITALY

12.1.5 SPAIN

12.1.6 RUSSIA

12.1.7 TURKEY

12.1.8 BELGIUM

12.1.9 NETHERLANDS

12.1.10 SWITZERLAND

12.1.11 SWEDEN

12.1.12 REST OF EUROPE

13 EUROPE RADIOTHERAPY MARKET: COMPANY LANDSCAPE

13.1 COMPANY SHARE ANALYSIS: EUROPE

14 SWOT ANALYSIS

15 EUROPE RADIOTHERAPY MARKET, COMPANY PROFILE

15.1 SIEMENS HEALTHCARE GMBH

15.1.1 COMPANY SNAPSHOT

15.1.2 REVENUE ANALYSIS

15.1.3 COMPANY SHARE ANALYSIS

15.1.4 PRODUCT PORTFOLIO

15.1.5 RECENT DEVELOPMENTS

15.2 HITACHI, LTD.

15.2.1 COMPANY SNAPSHOT

15.2.2 REVENUE ANALYSIS

15.2.3 COMPANY SHARE ANALYSIS

15.2.4 PRODUCT PORTFOLIO

15.2.5 RECENT DEVELOPMENTS

15.3 GENERAL ELECTRIC COMPANY

15.3.1 COMPANY SNAPSHOT

15.3.2 REVENUE ANALYSIS

15.3.3 COMPANY SHARE ANALYSIS

15.3.4 PRODUCT PORTFOLIO

15.3.5 RECENT DEVELOPMENTS

15.4 KONINKLIJKE PHILIPS N.V.

15.4.1 COMPANY SNAPSHOT

15.4.2 REVENUE ANALYSIS

15.4.3 COMPANY SHARE ANALYSIS

15.4.4 PRODUCT PORTFOLIO

15.4.5 RECENT DEVELOPMENTS

15.5 ELEKTA

15.5.1 COMPANY SNAPSHOT

15.5.2 REVENUE ANALYSIS

15.5.3 COMPANY SHARE ANALYSIS

15.5.4 PRODUCT PORTFOLIO

15.5.5 RECENT DEVELOPMENTS

15.6 ACCURACY INCORPORATED

15.6.1 COMPANY SNAPSHOT

15.6.2 REVENUE ANALYSIS

15.6.3 PRODUCT PORTFOLIO

15.6.4 RECENT DEVELOPMENTS

15.7 BEBIG MEDICAL.

15.7.1 COMPANY SNAPSHOT

15.7.2 PRODUCT PORTFOLIO

15.7.3 RECENT DEVELOPMENTS

15.8 BRAINLAB

15.8.1 COMPANY SNAPSHOT

15.8.2 PRODUCT PORTFOLIO

15.8.3 RECENT DEVELOPMENTS

15.9 CANON MEDICAL SYSTEMS CORPORATION

15.9.1 COMPANY SNAPSHOT

15.9.2 REVENUE ANALYSIS

15.9.3 PRODUCT PORTFOLIO

15.9.4 RECENT DEVELOPMENTS

15.1 ECKERT & ZIEGLER BEBIG

15.10.1 COMPANY SNAPSHOT

15.10.2 REVENUE ANALYSIS

15.10.3 PRODUCT PORTFOLIO

15.10.4 RECENT DEVELOPMENTS

15.11 IBA WORLDWIDE

15.11.1 COMPANY SNAPSHOT

15.11.2 REVENUE ANALYSIS

15.11.3 PRODUCT PORTFOLIO

15.11.4 RECENT DEVELOPMENTS

15.12 LINATECH INC

15.12.1 COMPANY SNAPSHOT

15.12.2 PRODUCT PORTFOLIO

15.12.3 RECENT DEVELOPMENT

15.13 MEVION MEDICAL SYSTEMS

15.13.1 COMPANY SNAPSHOT

15.13.2 PRODUCT PORTFOLIO

15.13.3 RECENT DEVELOPMENTS

15.14 NORDION (CANADA) INC. (A SUBSIDIARY OF SOTERA HEALTH)

15.14.1 COMPANY SNAPSHOT

15.14.2 PRODUCT PORTFOLIO

15.14.3 RECENT DEVELOPMENTS

15.15 P-CURE

15.15.1 COMPANY SNAPSHOT

15.15.2 PRODUCT PORTFOLIO

15.15.3 RECENT DEVELOPMENT

15.16 UNITED IMAGING HEALTHCARE CO., LTD

15.16.1 COMPANY SNAPSHOT

15.16.2 PRODUCT PORTFOLIO

15.16.3 RECENT DEVELOPMENT

15.17 VIEWRAY SYSTEMS, INC.

15.17.1 COMPANY SNAPSHOT

15.17.2 PRODUCT PORTFOLIO

15.17.3 RECENT DEVELOPMENT

15.18 ZEISS INTERNATIONAL

15.18.1 COMPANY SNAPSHOT

15.18.2 REVENUE ANALYSIS

15.18.3 COMPANY SHARE ANALYSIS

15.18.4 PRODUCT PORTFOLIO

15.18.5 RECENT DEVELOPMENTS

16 QUESTIONNAIRE

17 RELATED REPORTS

List of Table

TABLE 1 EUROPE RADIOTHERAPY MARKET: AVERAGE SELLING PRICE OF EQUIPMENT, SOFTWARE AND SERVICES

TABLE 2 EUROPE RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 3 EUROPE SERVICES IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 4 EUROPE PRODUCT IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 5 EUROPE PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 6 EUROPE EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 7 EUROPE PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 8 EUROPE INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 9 EUROPE SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 10 EUROPE SOFTWARE IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 11 EUROPE SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 12 EUROPE RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 13 EUROPE EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 14 EUROPE EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 15 EUROPE INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 16 EUROPE INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 17 EUROPE SYSTEMIC RADIOTHERAPY/ RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 18 EUROPE OTHERS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 19 EUROPE RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 20 EUROPE BREAST CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 21 EUROPE LUNG CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 22 EUROPE PROSTATE CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 23 EUROPE COLORECTAL CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 24 EUROPE LYMPHOMA IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 25 EUROPE LIVER CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 26 EUROPE THYROID CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 27 EUROPE BRAIN CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 28 EUROPE CERVICAL CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 29 EUROPE SPINE CANCER IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 30 EUROPE OTHERS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 31 EUROPE RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 32 EUROPE HOSPITALS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 33 EUROPE RADIATION THERAPY CENTERS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 34 EUROPE SPECIALTY CLINICS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 35 EUROPE OTHERS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 36 EUROPE RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 37 EUROPE DIRECT TENDERS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 38 EUROPE THIRD PARTY DISTRIBUTORS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 39 EUROPE OTHERS IN RADIOTHERAPY MARKET, BY REGION, 2018-2032 (USD THOUSAND)

TABLE 40 EUROPE RADIOTHERAPY MARKET, BY COUNTRY, 2018-2032 (USD THOUSAND)

TABLE 41 EUROPE RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 42 EUROPE PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 43 EUROPE EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 44 EUROPE PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 45 EUROPE INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 46 EUROPE SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 47 EUROPE SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 48 EUROPE RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 49 EUROPE EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 50 EUROPE INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 51 EUROPE RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 52 EUROPE RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 53 EUROPE RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 54 GERMANY RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 55 GERMANY PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 56 GERMANY EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 57 GERMANY PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 58 GERMANY INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 59 GERMANY SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 60 GERMANY SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 61 GERMANY RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 62 GERMANY EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 63 GERMANY INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 64 GERMANY RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 65 GERMANY RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 66 GERMANY RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 67 FRANCE RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 68 FRANCE PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 69 FRANCE EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 70 FRANCE PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 71 FRANCE INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 72 FRANCE SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 73 FRANCE SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 74 FRANCE RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 75 FRANCE EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 76 FRANCE INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 77 FRANCE RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 78 FRANCE RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 79 FRANCE RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 80 U.K. RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 81 U.K. PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 82 U.K. EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 83 U.K. PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 84 U.K. INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 85 U.K. SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 86 U.K. SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 87 U.K. RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 88 U.K. EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 89 U.K. INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 90 U.K. RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 91 U.K. RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 92 U.K. RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 93 ITALY RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 94 ITALY PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 95 ITALY EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 96 ITALY PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 97 ITALY INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 98 ITALY SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 99 ITALY SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 100 ITALY RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 101 ITALY EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 102 ITALY INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 103 ITALY RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 104 ITALY RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 105 ITALY RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 106 SPAIN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 107 SPAIN PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 108 SPAIN EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 109 SPAIN PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 110 SPAIN INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 111 SPAIN SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 112 SPAIN SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 113 SPAIN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 114 SPAIN EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 115 SPAIN INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 116 SPAIN RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 117 SPAIN RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 118 SPAIN RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 119 RUSSIA RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 120 RUSSIA PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 121 RUSSIA EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 122 RUSSIA PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 123 RUSSIA INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 124 RUSSIA SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 125 RUSSIA SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 126 RUSSIA RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 127 RUSSIA EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 128 RUSSIA INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 129 RUSSIA RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 130 RUSSIA RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 131 RUSSIA RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 132 TURKEY RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 133 TURKEY PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 134 TURKEY EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 135 TURKEY PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 136 TURKEY INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 137 TURKEY SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 138 TURKEY SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 139 TURKEY RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 140 TURKEY EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 141 TURKEY INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 142 TURKEY RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 143 TURKEY RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 144 TURKEY RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 145 BELGIUM RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 146 BELGIUM PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 147 BELGIUM EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 148 BELGIUM PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 149 BELGIUM INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 150 BELGIUM SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 151 BELGIUM SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 152 BELGIUM RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 153 BELGIUM EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 154 BELGIUM INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 155 BELGIUM RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 156 BELGIUM RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 157 BELGIUM RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 158 NETHERLANDS RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 159 NETHERLANDS PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 160 NETHERLANDS EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 161 NETHERLANDS PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 162 NETHERLANDS INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 163 NETHERLANDS SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 164 NETHERLANDS SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 165 NETHERLANDS RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 166 NETHERLANDS EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 167 NETHERLANDS INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 168 NETHERLANDS RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 169 NETHERLANDS RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 170 NETHERLANDS RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 171 SWITZERLAND RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 172 SWITZERLAND PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 173 SWITZERLAND EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 174 SWITZERLAND PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 175 SWITZERLAND INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 176 SWITZERLAND SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 177 SWITZERLAND SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 178 SWITZERLAND RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 179 SWITZERLAND EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 180 SWITZERLAND INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 181 SWITZERLAND RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 182 SWITZERLAND RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 183 SWITZERLAND RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 184 SWEDEN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 185 SWEDEN PRODUCT IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 186 SWEDEN EXTERNAL BEAM RADIOTHERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 187 SWEDEN PROTON THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 188 SWEDEN INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 189 SWEDEN SYSTEMIC RADIOTHERAPY/RADIOPHARMACEUTICALS IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 190 SWEDEN SOFTWARE IN RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

TABLE 191 SWEDEN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 192 SWEDEN EXTERNAL-BEAM RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 193 SWEDEN INTERNAL RADIATION THERAPY IN RADIOTHERAPY MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 194 SWEDEN RADIOTHERAPY MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 195 SWEDEN RADIOTHERAPY MARKET, BY END USER, 2018-2032 (USD THOUSAND)

TABLE 196 SWEDEN RADIOTHERAPY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 197 REST OF EUROPE RADIOTHERAPY MARKET, BY PRODUCT & SERVICES, 2018-2032 (USD THOUSAND)

List of Figure

FIGURE 1 EUROPE RADIOTHERAPY MARKET: SEGMENTATION

FIGURE 2 EUROPE RADIOTHERAPY MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE RADIOTHERAPY MARKET: DROC ANALYSIS

FIGURE 4 EUROPE RADIOTHERAPY MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE RADIOTHERAPY MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE RADIOTHERAPY MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE RADIOTHERAPY MARKET: MULTIVARIATE MODELLING

FIGURE 8 EUROPE RADIOTHERAPY MARKET: PRODUCT & SERVICES LIFELINE CURVE

FIGURE 9 EUROPE RADIOTHERAPY MARKET: MARKET END USER COVERAGE GRID

FIGURE 10 EUROPE RADIOTHERAPY MARKET: DBMR MARKET POSITION GRID

FIGURE 11 EUROPE RADIOTHERAPY MARKET: VENDOR SHARE ANALYSIS

FIGURE 12 EUROPE RADIOTHERAPY MARKET: SEGMENTATION

FIGURE 13 EUROPE RADIOTHERAPY MARKET: EXECUTIVE SUMMARY

FIGURE 14 EUROPE RADIOTHERAPY MARKET: STRATEGIC DECISIONS

FIGURE 15 NOVEL TECHNOLOGY IN RADIOTHERAPY FOR CANCER TREATMENT IS EXPECTED TO DRIVE THE GROWTH OF THE EUROPE RADIOTHERAPY MARKET FROM 2025 TO 2032

FIGURE 16 THE SERVICES SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE RADIOTHERAPY MARKET IN 2025 & 2032

FIGURE 17 DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES OF EUROPE RADIOTHERAPY MARKET

FIGURE 18 EUROPE RADIOTHERAPY MARKET: BY PRODUCT & SERVICES, 2024

FIGURE 19 EUROPE RADIOTHERAPY MARKET: BY PRODUCT & SERVICES, 2025-2032 (USD THOUSAND)

FIGURE 20 EUROPE RADIOTHERAPY MARKET: BY PRODUCT & SERVICES, CAGR (2025-2032)

FIGURE 21 EUROPE RADIOTHERAPY MARKET: BY PRODUCT & SERVICES, LIFELINE CURVE

FIGURE 22 EUROPE RADIOTHERAPY MARKET: BY TYPE, 2024

FIGURE 23 EUROPE RADIOTHERAPY MARKET: BY TYPE, 2025-2032 (USD THOUSAND)

FIGURE 24 EUROPE RADIOTHERAPY MARKET: BY TYPE, CAGR (2025-2032)

FIGURE 25 EUROPE RADIOTHERAPY MARKET: BY TYPE, LIFELINE CURVE

FIGURE 26 EUROPE RADIOTHERAPY MARKET: BY APPLICATION, 2024

FIGURE 27 EUROPE RADIOTHERAPY MARKET: BY APPLICATION, 2025-2032 (USD THOUSAND)

FIGURE 28 EUROPE RADIOTHERAPY MARKET: BY APPLICATION, CAGR (2025-2032)

FIGURE 29 EUROPE RADIOTHERAPY MARKET: BY APPLICATION, LIFELINE CURVE

FIGURE 30 EUROPE RADIOTHERAPY MARKET: BY END USER, 2024

FIGURE 31 EUROPE RADIOTHERAPY MARKET: BY END USER, 2025-2032 (USD THOUSAND)

FIGURE 32 EUROPE RADIOTHERAPY MARKET: BY END USER, CAGR (2025-2032)

FIGURE 33 EUROPE RADIOTHERAPY MARKET: BY END USER LIFELINE CURVE

FIGURE 34 EUROPE RADIOTHERAPY MARKET: BY DISTRIBUTION CHANNEL, 2024

FIGURE 35 EUROPE RADIOTHERAPY MARKET: BY DISTRIBUTION CHANNEL, 2025-2032 (USD THOUSAND)

FIGURE 36 EUROPE RADIOTHERAPY MARKET: BY DISTRIBUTION CHANNEL, CAGR (2025-2032)

FIGURE 37 EUROPE RADIOTHERAPY MARKET: BY DISTRIBUTION CHANNEL, LIFELINE CURVE

FIGURE 38 EUROPE RADIOTHERAPY MARKET: SNAPSHOT (2024)

FIGURE 39 EUROPE RADIOTHERAPY MARKET: COMPANY SHARE 2024 (%)

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.